According to a national survey by Pew Research Center conducted April 20-26, 2026 among 5,103 U.S. adults, inflation sits at 66% of the public calling it a very big problem, up from 63% last year.

Unemployment anxiety has also climbed 11 points since early 2025, and health care affordability is increasingly out of reach for many households.

For households already dealing with inflation and a reduced financial cushion, borrowing is less a choice and more a calculation.

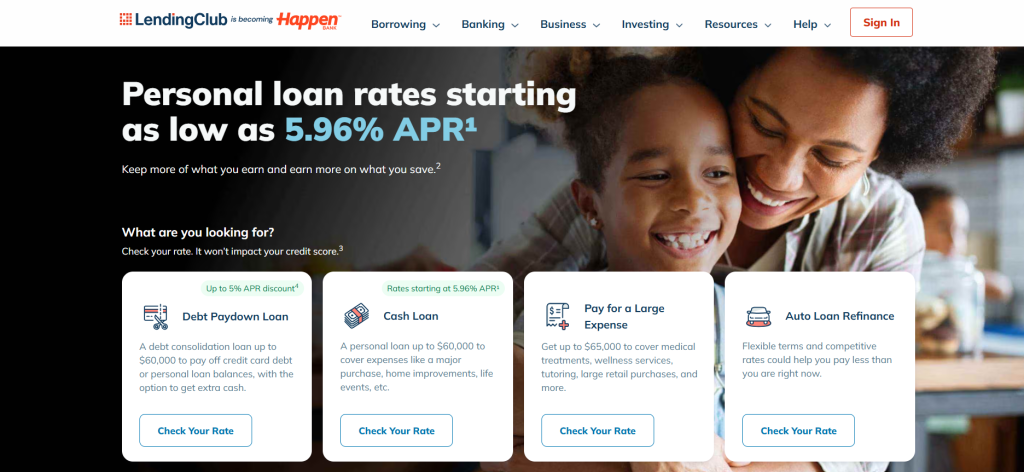

In your search for a potential lender, you may encounter LendingClub. So, this LendingClub review will break down what it offers and if it’s worth the cost.

What Is LendingClub?

LendingClub, founded in the United States in 2007, was one of the country’s first peer-to-peer (P2P) lending platforms. It directly links borrowers and individual investors, and replaces traditional banks in undertaking the function of capital intermediary.

LendingClub has transformed into a full-service, FDIC-insured digital bank operating as LendingClub Bank, N.A., which provides personal loans, checking accounts, and savings account services.

The company will officially change its name to Happen Bank, transitioning into a diversified digital-first bank that integrates deposit and loan services.

LendingClub at a Glance

| LendingClub Personal Loans | |

|---|---|

| Loan Amounts | $1,000 – $60,000 |

| Term Lengths | 24 to 84 months |

| APR Range | 5.96% – 35.99% |

| Origination Fee | 0% – 8% |

| Rate Check | Soft credit pull |

| Hard Inquiry | Only upon loan issuance |

Loan Amounts and Terms

LendingClub offers personal loans with flexible amounts and repayment schedules to accommodate different borrowing needs.

Loan Amounts

LendingClub’s personal loan limits range from $1,000 to $60,000. Its low entry threshold enables borrowers to borrow only what they need, preventing them from taking on unnecessary debt.

Repayment Terms

Personal loans offered on this platform have terms ranging from 24 to 84 months.

LendingClub Rates and Fees

- APR range: 5.96% to 35.99%, set at the time of application. Borrowers with excellent credit qualify for the lower end, though loan amount and term length also factor into the final rate.

- Origination fee: 0% to 8%, deducted from the loan proceeds before disbursement. Borrowers can review the exact fee on the loan offer page and in the Truth in Lending Disclosure before accepting.

- Prepayment: No penalty for paying off a loan early.

- Late fee: A 15-day grace period applies before any penalty takes effect on a missed loan payment.

LendingClub Eligibility Requirements

The company targets fair- to good-credit borrowers, though applicants with higher scores and stable income have better approval odds. Here is what the application process requires:

- Credit score: 600 and above

- Credit history: Minimum of 3 years and 2 open accounts

- Debt-to-income ratio: Cannot exceed 40%

- Income: No set minimum, but applicants must show proof of employment or income

- Citizenship: U.S. citizens with a valid Social Security number and proof of residency

- Other: Valid bank account, government-issued photo ID, and an active email address

- State availability: Available in all 50 states and Washington, D.C.

How to Apply

Applying for LendingClub personal loans starts on their website and takes a few minutes.

Pre-Qualify

Fill out basic details, including your name, address, loan amount, and purpose. LendingClub uses a soft credit pull here, so your credit score stays unaffected. Once submitted, you’ll see multiple loan offers, each listing the amount, term, APR, and estimated monthly payment.

Select Your Offer

Go through the offers and pick one. Pay attention to both the APR and origination fee before deciding.

Submit Full Application

Complete the full application and provide supporting documents, including bank account information. LendingClub performs a hard credit check at this point.

Sign Loan Agreement

Read through all terms before signing, particularly the origination fee, which gets deducted from the loan proceeds before disbursement.

Receive Funds

Investors in LendingClub’s marketplace fund the approved loan. From start to finish, the process takes around seven business days.

The Direct-Pay Debt Consolidation Feature

LendingClub’s Direct Pay option routes loan funds to creditors, bypassing the step where borrowers manage payments themselves.

Any leftover balance after creditors are paid gets deposited into the borrower’s bank account.

How the Direct-Pay Process Works

The application process follows the same steps as a standard cash loan. The only difference is that borrowers add their creditors during the application.

After approval, LendingClub sends payments to those creditors within a few days to a couple of weeks, depending on how each creditor accepts payments.

Borrowers should keep up with their regular payments during that period to avoid late fees. If an overpayment happens before the transfer is finalized, the creditor issues a refund.

Once the payment is confirmed, received, and applied, borrowers can reach out to their creditors to close the paid accounts.

Direct Pay loans cannot cover mortgages, auto loans, student loans, business loans, or existing LendingClub personal loans.

Why It Stands Out vs Competitors

Direct Pay loans use fixed rates, so the monthly payment stays consistent throughout the loan term, unlike credit cards, where rates can change.

The APR may also come in lower than a credit card rate, depending on the borrower’s credit profile and loan terms.

For borrowers looking to consolidate debt across multiple accounts, having LendingClub handle the payments removes the risk of receiving funds and leaving balances unpaid.

Other LendingClub Services

LendingClub Bank offers more than personal loans. Its product lineup spans personal banking, business financing, and investing.

Personal Banking

LendingClub’s personal banking products include the LevelUp checking account, the LevelUp savings account, and certificates of deposit.

No minimum opening deposit is required for either account, and there are no monthly maintenance fees.

All deposit products are FDIC-insured up to $250,000 per depositor, per ownership category.

LevelUp Checking

- Earns cash back on qualified purchases at grocery stores, gas stations, and pharmacies based on each merchant’s category code.

- A debit card must be active to earn rewards.

- New account holders can earn account bonuses of up to $350: $200 for setting up direct deposit of at least $2,000 and $150 for completing at least ten debit card transactions, both by June 30, 2026.

LevelUp Savings

- Applies the LevelUp rate to the full balance when the account receives at least $250 in deposits per evaluation period, which equals one statement cycle.

- The first evaluation period begins at the third statement cycle after account opening.

- Interest payments, account credits, and bank reversals are not considered deposits for rate evaluation.

- The LevelUp rate prior to the first evaluation period is variable and subject to change at the bank’s sole discretion.

Business Financing Solutions

LendingClub provides point-of-sale financing for businesses in Health and Wellness, Home Improvement, and Retail Services. These options let businesses offer payment plans to their customers at the point of sale.

Business Loans

For business owners, LendingClub offers Small Business Loans and SBA Loans to fund operations, expansion, or other business expenses.

Investing

Through its Institutional Investing program, LendingClub gives institutional investors access to interest earnings generated through its lending marketplace.

Pros and Cons of LendingClub

Before applying, here is where LendingClub stands out and where it falls short.

Pros

- Simple application process: The application process starts with three questions on the homepage and takes only a few minutes. Personal loan customers who get approved can expect funds within a few business days.

- No prepayment penalty: Borrowers can pay off LendingClub personal loans early with no additional charges.

- Educational resources: LendingClub dedicates sections of its website to credit score education, helping borrowers make more informed decisions about loan payments and borrowing.

- Peer-to-peer lending: Connecting borrowers with individual investors instead of traditional banks gives borrowers access to capital outside the conventional banking system.

Cons

- Origination fee: LendingClub deducts 0% to 8% from loan proceeds before funds are sent. P2P investors collect most of the interest payments, so this fee keeps the platform running. Several competing lenders skip it entirely.

- Late payment fee: A $15 or 5% penalty applies to late or failed fixed monthly payments. The 15-day grace period gives borrowers a short window before the charge takes effect.

- Irregular income: Self-employed borrowers with inconsistent annual income tend to face more friction during the application process than salaried applicants.

- Paper check fee: Borrowers who forgo direct deposit or automated payments from their bank account pay a $7 processing fee per paper check.

LendingClub Reviews

Across review platforms, this LendingClub review section captures both the praise and the recurring pain points borrowers report.

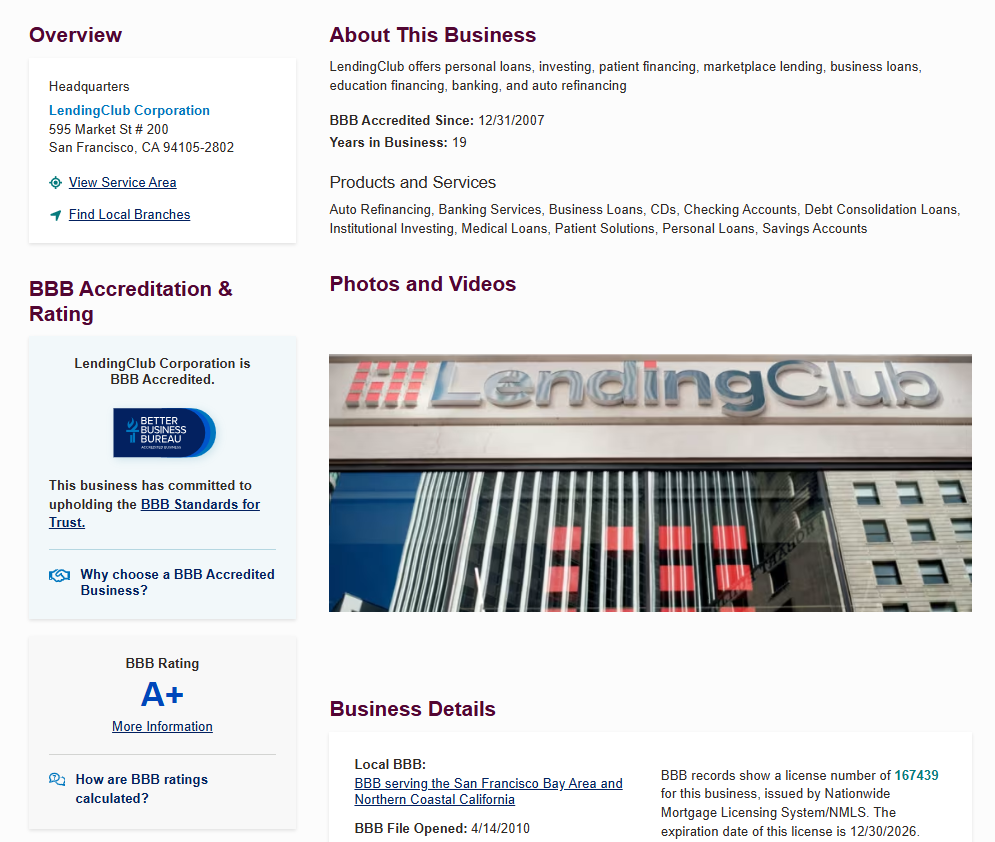

Better Business Bureau (BBB) Reviews

LendingClub holds a BBB A+ rating and has been accredited since 2008 as an online bank.

The customer service team receives mixed feedback, with 624 BBB reviews averaging 3.99 stars.

Over 1,066 complaints were filed in three years, with billing issues topping the list.

Common complaints involve payment processing errors, duplicate charges, and unresolved disputes over account balances.

LendingClub responds to most complaints, though many customers report dissatisfaction with the resolutions provided.

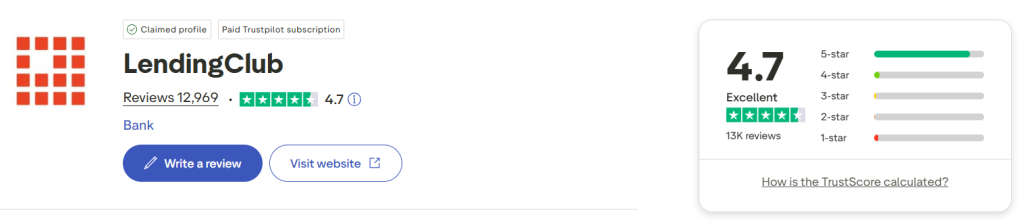

Trustpilot Reviews

LendingClub holds a 4.7 Trustpilot rating based on over 12,000 reviews from verified borrowers nationwide.

The customer service team is consistently praised for being responsive, friendly, and helpful to borrowers.

Customers highlight the fast process, with debts paid to creditors directly within a few days.

Some reviewers reported issues with payments not reflecting on account balances as expected or on time.

A few borrowers felt the advertised rates did not match the processing timelines they actually experienced.

Reddit Reviews

Anybody use The Lending Club?

by

u/cheesusismygod in

povertyfinance

On Reddit, most users recognize that Lending Club operates in compliance with relevant regulations, while some users warn others to guard against impersonation scams.

All borrowers who used Credit Karma’s recommendation service agreed that the debt consolidation loan process was fast and straightforward.

Numerous users have praised that the fee rates of this financial service are far lower than those of high-interest credit cards and those charged by other banks.

User complaints fall into two categories: wire transfer delays and non-compliant debt collection levied against users who have made their payments on time.

LendingClub vs Alternatives

| APR Range | Loan Amounts | Min. Credit Score | Credit Score Category | Origination Fee | Late Fee | Repayment Terms | Discounts | |

|---|---|---|---|---|---|---|---|---|

| LendingClub | 5.96% – 35.99% | $1,000 – $60,000 | 600+ | Fair, good | 0% – 8% | None within 15-day grace period | 24 – 84 months | None listed |

| LightStream | 6.49% – 24.89% | $5,000 – $100,000 | 660+ | Excellent, good | 0% | None | 24 – 144 months | 0.50% rate reduction for autopay |

| Upgrade | 7.74% – 35.99% | $1,000 – $50,000 | 580+ | Fair, bad | 1.85% – 9.99% | $10 | 24 – 84 months | None listed |

Who Should and Shouldn’t Use LendingClub

LendingClub is for you if:

- Credit score 600–720: LendingClub is most competitive in this range, where many traditional banks offer fewer options

- Borrowers looking to consolidate debt across multiple accounts with payments sent to creditors directly

- Anyone needing between $1,000 and $5,000, a loan size most competing lenders skip

- Applicants with a co-borrower who want to improve approval odds or secure a lower rate

- Borrowers who want to check a loan offer through a soft credit pull before committing

LendingClub may not be for you if:

- Credit score 720 or above: SoFi or LightStream offer lower rates with reduced or no origination fees

- Borrowing above $60,000: SoFi and LightStream both go up to $100,000

- DTI above 40%: LendingClub’s maximum DTI requirement makes approval unlikely, regardless of credit score

- Credit history under three years: the minimum history requirement blocks approval for thin files

- Borrowers focused on avoiding fees: the origination fee of up to 8% is a cost that better-credit lenders do not charge

- Borrowers who prefer in-person service: LendingClub has no physical branches and operates entirely as a digital bank