Buy now, pay later is increasingly used at retail checkouts as an alternative to credit cards, with services like Klarna experiencing solid growth.

According to Statista, the market is expected to expand by nearly 9% annually through 2028. JD Power’s 2026 study also emphasizes this rapid growth, driven by the increased BNPL use offered by fintech providers.

And while the best credit cards still offer rewards and purchase protection, more consumers are choosing installment payments.

So, if you’re considering using Klarna, this review will explain what to expect before you sign up.

What Is Klarna?

Klarna is a Swedish fintech company. It was established in 2005 and is based in Stockholm.

Klarna’s app currently works with more than 600,000 merchants and is running in 26 countries, including the United States.

You can pay with it (debit card, Apple Pay, or Visa card), and it is available through the Apple App Store and Google Play Store.

Klarna BNPL Details: Terms, Fees, Requirements, Availability

| Category | Details |

|---|---|

| Service type | Buy Now, Pay Later platform (not a credit card or lender) |

| Payment plans | Pay in 4, Pay, Pay over time, Pay in full today, Pay in 30 days |

| APR range | 0.00% to 35.99% |

| Late fees | Up to $7 (U.S.) or local equivalent per missed payment |

| Credit check | Soft check for Pay in 4; hard inquiry for long-term financing |

| Availability | U.S., U.K., EU, Canada, Australia |

| App features | Order tracking, budgeting tools, virtual shopping cards |

What Products Does Klarna Offer?

Through the Klarna card or app, users have four ways to pay:

- Pay in 4: Split the purchase into four equal interest-free payments, made every two weeks.

- Pay over time: Installment payments with 6-24-month options.

- Pay in full today: A debit mode option where you can pay in full immediately.

- Pay in 30 days: Get the item now and pay the full amount within 30 days of the purchase date.

Who Qualifies for Klarna?

Anyone at least 18 with a valid bank account or debit card and a verifiable address can use Klarna’s service.

Before deciding whether to approve your application, Klarna will assess your purchase amount, your history with Klarna, and internal data.

There is no minimum credit score or required threshold at all, though Klarna said it may perform a soft credit check.

If you have poor credit or a record of missed payments, you may be less likely to qualify for large purchases or longer-term monthly payments.

What Fees Does Klarna Charge?

- No annual fees: Opening or using a Klarna account doesn’t cost anything annually.

- Pay in 4: A late fee may apply for each missed payment, depending on your terms.

- Pay over time: Interest and late fees may apply. Klarna performs a soft credit check, and APR can range from 0.00% to 35.99%.

- Pay in 30: No late fees, but you must check your terms.

- Failed payments: If your bank account or payment method fails, Klarna may charge a returned payment fee.

- Service fees: Most service fees are covered by merchants, not shoppers.

How to Use Klarna

- Download and set up: Get the Klarna app or Chrome extension, create a Klarna account, and link a payment method like a debit card or Apple Pay.

- Shop online: Select a Klarna payment plan at checkout when shopping with participating Klarna online stores.

- Shop in-store: Use the app to create a digital card, then add it to your mobile wallet or scan a QR code at checkout, depending on the store.

Benefits of Klarna

Klarna gives users different ways to manage how they pay, especially for online purchases and everyday checkouts.

- Flexible payment options: Split purchases into interest-free installments or choose long-term financing.

- Wide retailer access: Use Klarna with major retailers online and in-store.

- Helpful mobile app: Track payment details, get reminders, and manage due dates via the Klarna app on iOS and Android.

Risks & Limitations of Klarna

The Klarna app can be convenient, but it also comes with drawbacks that buyers should pay attention to before choosing a Klarna payment plan.

- Spending can add up: Easy approvals can lead to growing balances over time.

- Late fees and credit risk: Missed payments may trigger fees or hurt your credit report.

- Fewer protections: Klarna lacks the dispute safeguards that credit cards provide.

Klarna Reviews

Klarna reviews show mixed experiences:

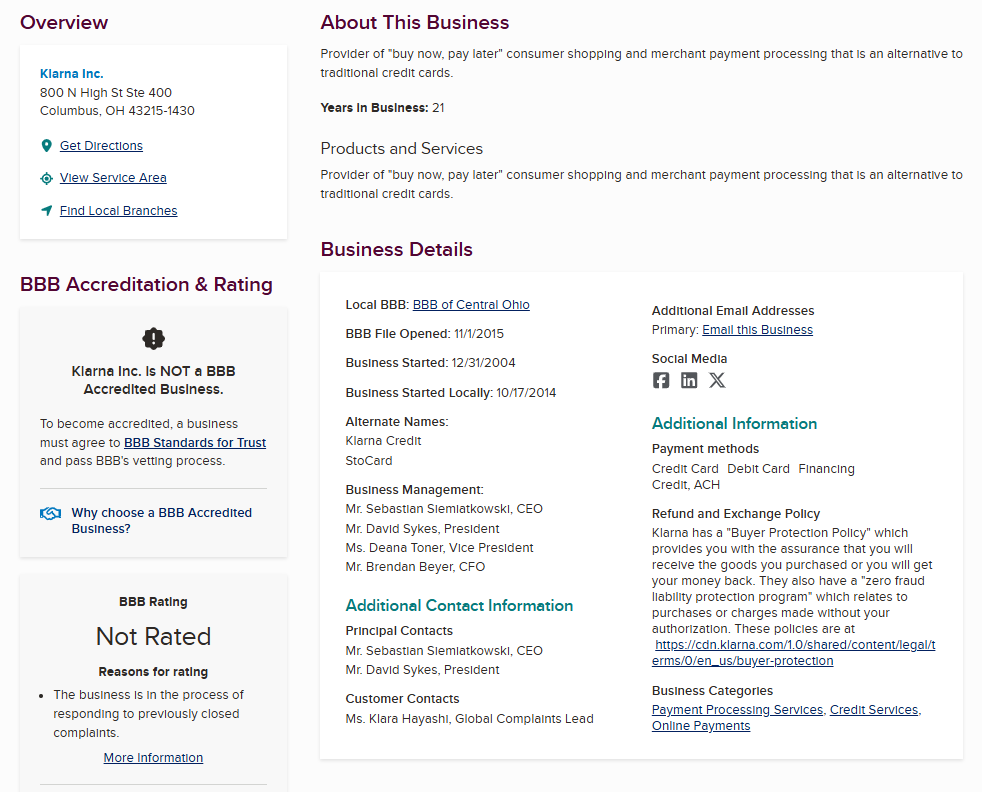

Better Business Bureau (BBB) Reviews

Klarna is not accredited by the BBB and doesn’t have a rating. In the last three years, users submitted more than 2,700 complaints, most of them about billing, refunds, and problems with merchants.

Some customers said they had paid for items that never arrived or had experienced delays in resolving disputes. In some cases, Klarna either forgave the balance or told the customer to contact the store directly. The complaints remain unresolved.

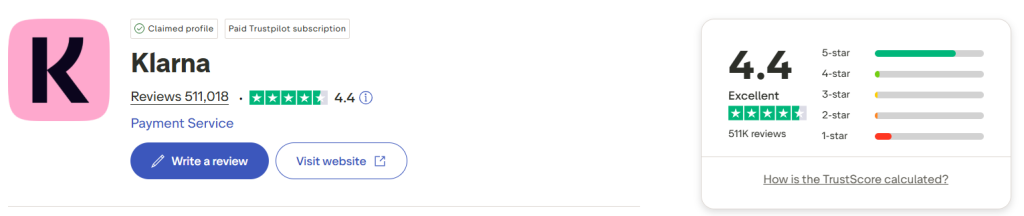

Trustpilot Reviews

Most reviews state Klarna makes it easier to handle purchases, especially with smaller split payments. The Klarna app is widely considered to be easy to understand.

A few users complain about overcharging, confusing credit checks, and slow refunds or returns. Some say fees come before items ship, or support takes longer than they’d like.

Most find Klarna easy to use, based on over 500,000 reviews and an average rating of 4.4 stars, but this ultimately depends on how you utilize each Klarna payment plan.

Reddit Reviews

Some Reddit users say Klarna helps with short-term purchases when paid off on time, especially thanks to the interest-free options and simple app. Others mention issues like late fees, refund delays, and trouble reaching support.

In certain countries, Klarna activity appears on your credit report, which has affected mortgage approvals for those with heavy BNPL use.

A few also describe falling into emotional spending and juggling too many payment plans at once.

Used occasionally, it offers flexibility, but frequent use can raise concerns.

When to Use Klarna

Klarna can work well in specific situations, especially when timing and spending are predictable.

- You pay on time and want flexibility: Klarna’s Pay in 4 and Pay in 30 options can help break up costs without using a credit card or taking out personal loans.

- Need a bridge for occasional purchases: Useful for larger purchases or one-time expenses from major retailers when you want shorter-term breathing room.

When to Avoid Klarna

Klarna isn’t always the right choice, especially if you already manage tight budgets or rely on credit-building tools.

- Struggle with debt or impulse spending: Klarna can add to the problem if you miss payments or overspend without planning.

- Want to build credit: A missed payment may show up on your credit report and hurt your score, since Klarna reports to credit bureaus.

- Prefer traditional protections: A visa card or credit card usually offers stronger fraud support and easier dispute handling.

Is Klarna Safe?

Klarna is considered safe for most users. It uses industry-standard protections, including strong encryption, two-step login where you receive verification codes, and continuous fraud detection.

How Klarna Compares to Other BNPL Platforms

| Provider | Key Features / Highlights |

|---|---|

| Klarna | Widely accepted at major retailers including Amazon, Walmart, Target, eBay, and Sephora. Soft credit checks for short-term plans. No fees or interest unless repayment goes past 30 days. Beginner-friendly spending limits. |

| Sezzle | Offers interest-free payments and an in-app digital card for in-store purchases at retailers like T.J. Maxx, Ulta, and Lowe’s. Soft credit checks for Pay in 4 and Pay in 2. Hard checks only for monthly financing. |

| Affirm | Provides higher financing limits up to $30,000, ideal for big purchases. |

| Afterpay | Beginner-friendly and widely accepted at stores like Belk and Lululemon. Optional Afterpay Plus upgrade expands use. Spending limits increase over time. |