Credit card interest does not pause while you plan. Indeed, many Americans carry high balances and feel stuck. Meanwhile, minimum payments barely move the principal, so the debt compounds year after year.

For some borrowers, bankruptcy can feel too extreme. Debt settlement, on the other hand, can feel too risky. Therefore, a debt management plan often sits between those two paths.

Trinity Debt Management has offered that middle path since 1994. Specifically, it is a nonprofit credit counseling agency based in Cincinnati, Ohio. Because it works directly with creditors, the agency can lower interest rates. In addition, it folds several payments into one monthly bill.

This Trinity Debt Management review explains what the program does. Moreover, it covers fees, the application process, and real customer feedback. Finally, it flags what to verify before you enroll, and how Trinity compares to other nonprofit options.

Quick Trinity Debt Management Facts (TL;DR)

- A nonprofit and faith-based credit counseling agency based in Cincinnati, Ohio.

- Active since 1994, so more than 30 years of operating history.

- Offers debt management plans (DMPs) for unsecured debts.

- Holds FCAA accreditation and ISO 9001:2015 certification.

- Does not hold BBB, AFCC, or IAPDA accreditation.

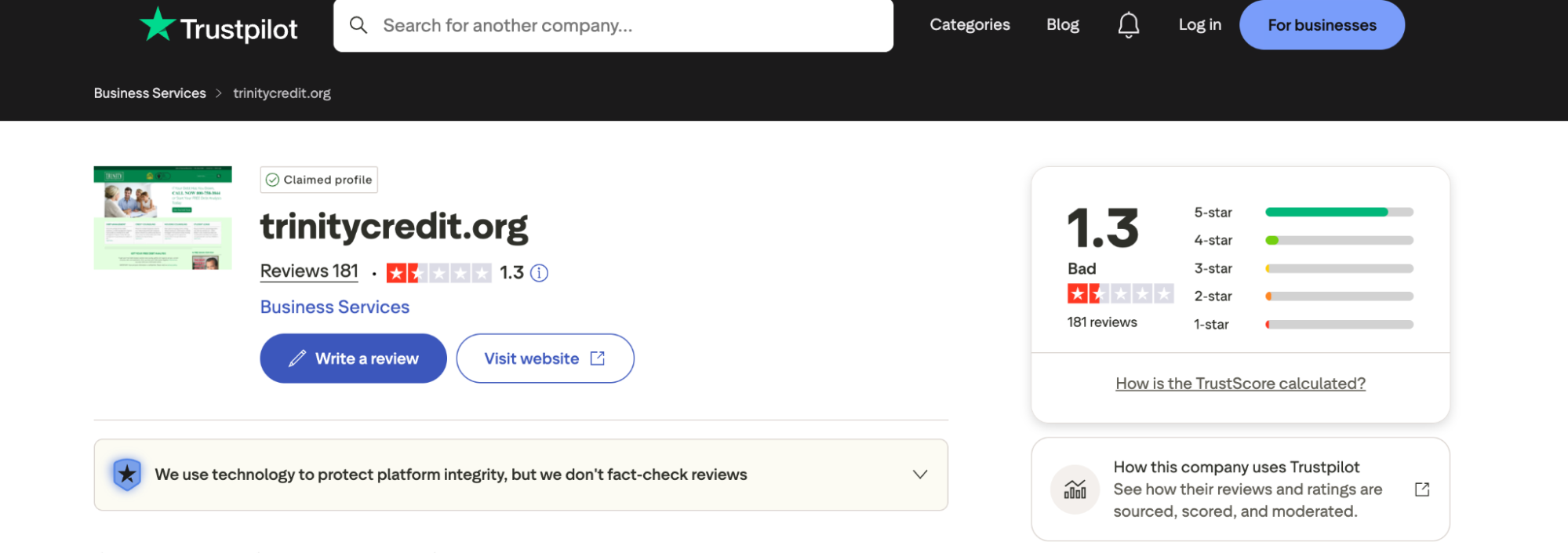

- Trustpilot rating sits at 1.3 out of 5 across 181 reviews at time of writing.

- The BBB does not currently list a star rating for Trinity.

- The initial consultation is free.

- Setup fees tend to fall under $50, and monthly fees fall between $20 and $50.

- Most plans run three to five years.

- Service is not offered in Kansas, Montana, Nevada, New York, or Rhode Island.

See which debt payoff method fits your situation in Explore your options, the best ways to pay off credit card debt.

Trinity Debt Management Company Overview

Trinity Debt Management operates under the legal name Trinity Credit Counseling, Inc., and it is headquartered in Cincinnati, Ohio. Notably, the agency has run nonstop since 1994. As a result, it ranks among the longer-standing nonprofit credit counseling agencies in the country.

Although Trinity positions itself as a Christian-centered organization, it still serves clients of every faith and background.

In terms of credentials, the agency holds accreditation from the Financial Counseling Association of America (FCAA). Additionally, it carries an ISO 9001:2015 quality management certification. Its counselors, meanwhile, are certified by the Partnership for Financial Education. Trinity is also a member of the Credit Builders Alliance.

Because it is a registered 501(c)(3) nonprofit, Trinity faces nonprofit oversight. Consequently, that status limits the financial pressure to upsell clients, which is common in for-profit debt relief companies.

Trinity Debt Management Accreditation and Legitimacy

First, the reassuring part: Trinity is a legitimate nonprofit agency, and its 501(c)(3) status is confirmed.

That said, Trinity does not hold accreditation from the Better Business Bureau (BBB). Likewise, it does not hold accreditation from the American Fair Credit Council (AFCC) or the International Association of Professional Debt Arbitrators (IAPDA).

Its National Foundation for Credit Counseling (NFCC) membership status also shows up in some third-party lists. However, other sources do not list it at all.

Ultimately, the absence of BBB accreditation and the conflicting NFCC information are transparency gaps. By comparison, several competing nonprofit agencies hold more of these credentials.

Trinity Debt Management Key Services and Programs

Trinity offers a small set of services that all support consumer debt repayment. Primarily, its core service is the debt management plan, which almost every Trinity client uses.

In addition, the agency offers a few support services.

- Free credit counseling sessions.

- Budget reviews and household money planning.

- Basic education on bankruptcy options.

- Basic education on student loan repayment paths.

- A free financial literacy guide for long-term money habits.

However, Trinity does not offer debt settlement, direct loans, or tax resolution. Furthermore, it does not provide the depth of housing counseling that some larger nonprofits offer.

How the Trinity Debt Management Plan Works

To be clear, a DMP is not debt settlement, and it is not bankruptcy. Instead, it is a structured repayment program for unsecured debt.

First, Trinity asks each creditor to lower your interest rate. As a result, many creditors drop rates to a range of 6 percent to 10 percent. By contrast, standard credit card rates often sit between 18 percent and 25 percent.

Next, you make one consolidated monthly payment to Trinity. Then the agency sends each payment to your creditors on a set schedule.

In most cases, enrolled credit cards are closed once the plan starts. Consequently, that helps prevent new debt while you repay the old balances. Moreover, you can leave the plan early with no penalty.

Debts Trinity can help with.

- Credit cards.

- Medical bills.

- Unsecured personal loans.

- Department store cards.

Debts Trinity cannot help with.

- Payday loans.

- Auto loans.

- Mortgages.

- Tax debt.

- Federal student loans.

- Business debt.

Trinity Debt Management Application Process and Eligibility

Generally, Trinity follows five core steps.

- Free consultation. First, call Trinity to schedule the session. Beforehand, gather proof of income, a list of all debts, and recent creditor statements. Note that office hours run weekdays from 10 a.m. to 6 p.m. Eastern. Because there are no weekend or evening hours, the schedule may be a limit for borrowers with standard work hours.

- Debt analysis. Next, a certified counselor reviews your income, expenses, and balances. Then they confirm whether a DMP is the right fit. Although Trinity does not require a minimum credit score, you do need steady income.

- Creditor negotiations. After that, Trinity contacts each creditor and asks for lower rates. However, not all creditors agree. Therefore, ask which of your specific creditors Trinity already has agreements with before you enroll.

- Plan enrollment. Once creditors agree, you start one consolidated monthly payment. Meanwhile, enrolled credit card accounts close to new charges.

- Ongoing repayment and monitoring. Finally, the plan runs three to five years. For convenience, Trinity offers an online portal for payment tracking. Still, you should log into each creditor account every month to confirm payments posted on time.

Learn how debt management plans stack up against other strategies in Debt management methods, successful strategies for getting out of debt.

Trinity Debt Management Pricing and Fees

To begin, the first consultation is free, so there is no charge until you enroll.

After enrollment, however, two fees apply.

- A one-time setup fee.

- A monthly maintenance fee.

Unfortunately, Trinity does not publish its fee schedule online. Instead, exact amounts depend on your state and your case. According to outside reporting, the setup fee falls under $50 in most cases. Similarly, monthly fees tend to fall in the $20 to $50 range. Still, these are estimates only, so call Trinity to confirm specific figures before you commit.

How Trinity’s Fees Compare to Other Nonprofits

Overall, Trinity’s estimated range matches the rest of the nonprofit DMP industry. The main gap, however, is transparency, because most other nonprofits post fees on their website.

For context, here is how three common alternatives publish their fees.

- American Consumer Credit Counseling (ACCC) charges a one-time $39 enrollment fee and an average $25 monthly fee.

- Cambridge Credit Counseling averages $40 upfront and $30 per month.

- GreenPath Financial Wellness averages $35 upfront and $28 per month.

Notably, all three of those agencies publish a clear fee schedule. By contrast, Trinity is the only one in that group that requires a phone call to confirm pricing. As a result, that lack of upfront transparency adds friction for borrowers comparing options side by side.

Therefore, before you commit, ask Trinity, in writing, for the items below.

- Your exact setup fee for your state.

- Your exact monthly fee for your state.

- Any hardship reduction options.

- How late or returned payments are handled.

Trinity Debt Management Customer Reviews and Complaints

In short, Trinity reviews are split. While its own site shares warm testimonials, independent third-party platforms tell a harder story. Accordingly, here is a breakdown by platform.

Trustpilot Reviews

Currently, Trinity has a 1.3 out of 5 rating on Trustpilot across 181 reviews at time of writing. For a nonprofit in this category, that is a low score.

On the positive side, reviewers describe the items below.

- Caring, step-by-step counselors.

- Real interest rate reductions.

- A clear, single monthly payment.

Conversely, negative reviewers describe these items.

- Missed payments to creditors.

- Unexpected jumps in the monthly payment amount.

- Inconsistent answers from staff about account status.

In one striking case, a reviewer reported paying $30,000 into the program. Even so, they said their credit score still dropped because Trinity missed creditor payments.

Better Business Bureau (BBB) Reviews

As noted earlier, Trinity is not BBB-accredited, and the BBB does not currently list a star rating for it. Generally, BBB accreditation requires meeting standards for transparency, complaint resolution, and honest advertising. Although the absence does not signal misconduct on its own, it does mean borrowers have one less third-party oversight layer to lean on. By comparison, GreenPath Financial Wellness carries an A+ BBB rating.

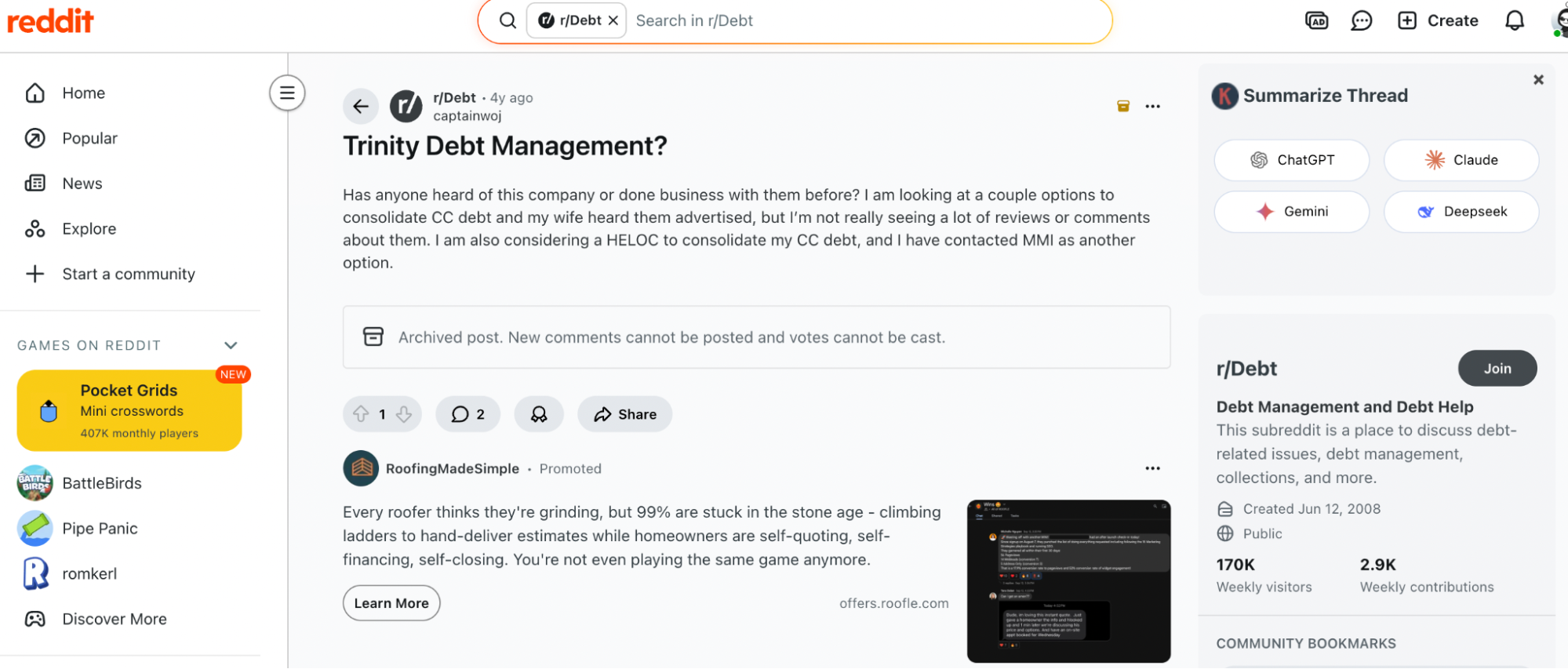

Reddit Reviews

Admittedly, Reddit threads about Trinity are limited, since the agency does not get the volume of mentions that bigger DMP providers get.

Still, when Trinity does come up in personal finance subreddits, users tend to flag these themes.

- Missed or late payments to creditors.

- Slow or unclear responses from customer service.

- Mixed feelings after the first counseling call.

Meanwhile, a few Reddit users share positive notes about the initial consultation. Most, however, caution that DMP execution can feel uneven.

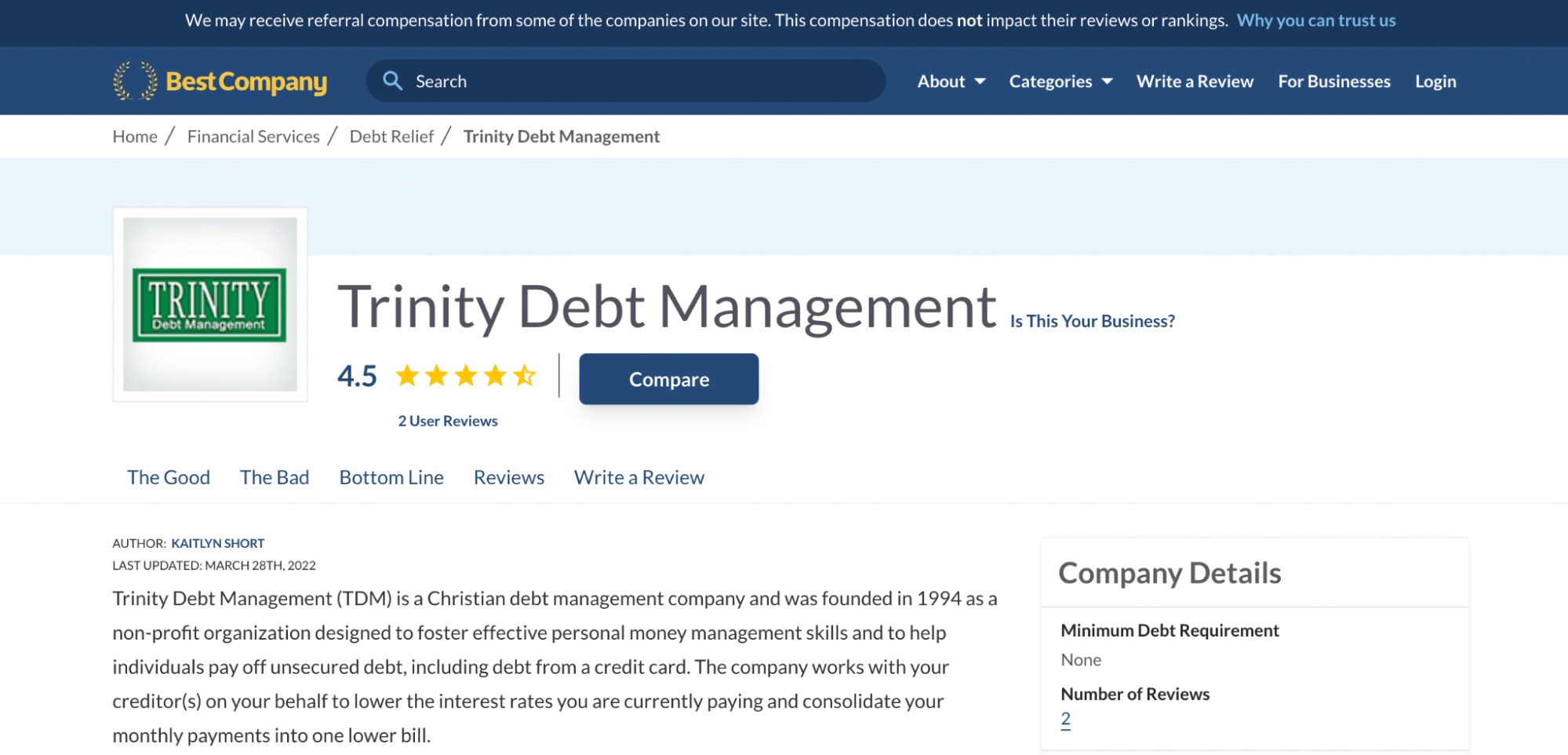

BestCompany and ConsumerAffairs Reviews

Similarly, BestCompany and ConsumerAffairs show the same split pattern as Trustpilot. For example, some clients praise the faith-based culture and helpful one-on-one calls. Others, by contrast, report late payments, surprise increases in monthly cost, and slow customer service. In addition, both platforms noted that Trinity did not respond to their requests for more information.

Reader safety note. Above all, do not rely on the Trinity client portal alone. Instead, log into each creditor account each month and confirm Trinity posted your payment on time. Also, save proof of every call and email with Trinity.

How a Trinity Debt Management Plan Affects Your Credit Score

Over time, a DMP can help your credit. In the short term, however, the picture is more mixed.

Here is what can happen at the start.

- Enrolled credit cards close, which lowers your available credit.

- As a result, your credit utilization rate may rise on paper for a few months.

- In addition, some creditors report each account as enrolled in a DMP.

Importantly, that DMP note is not the same as a bankruptcy filing, nor is it the same as a debt settlement note. Even so, some future lenders still view it less favorably during a credit check.

By contrast, here is what can improve over time.

- Because payment history makes up 35 percent of a FICO score, every on-time DMP payment builds that factor.

- Likewise, amount owed makes up 30 percent of a FICO score, and balances drop steadily through the program.

For instance, Trinity reports that some clients see credit gains of up to 200 points across a full program. Meanwhile, NFCC industry data shows DMP enrollees often gain about 106 points across the first three years.

Ultimately, all of those gains depend on one thing: Trinity must post every payment on time. Unfortunately, documented complaints show this has not always happened. Therefore, independent monthly verification is not optional; rather, it is the safety net for your credit.

Trinity Debt Management Outcomes and Success Rate

Unfortunately, Trinity does not publish a verified client completion rate. Likewise, it does not publish average client savings across its full client base. Clearly, that is a real transparency gap.

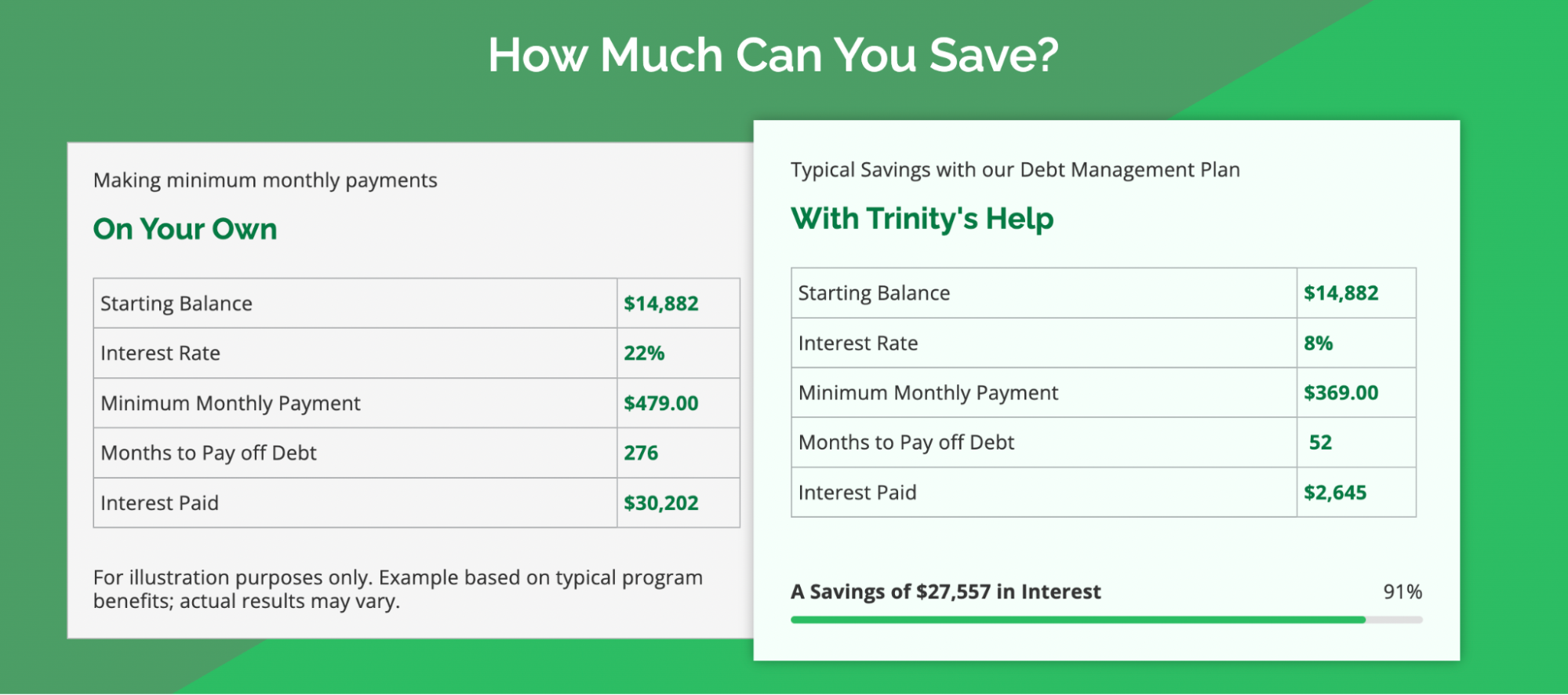

Nonetheless, Trinity does share illustrated examples on its site. In one example, a client carries $14,882 in debt at 22 percent interest. Under a standard plan, that would cost $30,202 in total interest over time. However, under Trinity’s DMP, the rate drops to 8 percent, the monthly payment falls to $369, and the total interest paid falls to $2,645. Of course, Trinity notes those figures are illustrations and that real results vary.

To fill the gap, industry benchmarks help.

- For example, Money Management International clients saved more than $48,000 in total interest on average in 2024.

- Additionally, NFCC data shows DMP enrollees often complete plans within three to five years.

Typically, most Trinity clients carry $5,000 or more in unsecured debt. Still, the savings only matter if Trinity makes every payment on time, so track each creditor account every month.

Trinity Debt Management Pros and Cons

To decide whether Trinity fits your needs, weigh the strengths and weaknesses below.

Pros

- Nonprofit 501(c)(3) status, with limited upselling pressure.

- More than 30 years of nonstop operating history.

- Free initial consultation and debt analysis.

- FCAA accreditation and ISO 9001:2015 certification.

- Online client portal for payment tracking.

- No penalty for early payoff.

- Member of the Credit Builders Alliance.

- Free financial literacy guide and budgeting resources.

- Christian-centered counseling culture that many clients value.

Cons

- Low Trustpilot rating of 1.3 out of 5 at time of writing.

- No BBB, AFCC, or IAPDA accreditation.

- Fee schedule is not published online.

- Recurring complaints about missed or delayed creditor payments.

- Office hours run only weekdays from 10 a.m. to 6 p.m. Eastern.

- Service is not offered in Kansas, Montana, Nevada, New York, or Rhode Island.

- No principal forgiveness, so borrowers repay the full balance.

- Smaller service menu than larger nonprofit competitors.

- More basic digital tools than agencies like GreenPath or MMI.

- Conflicting public information on NFCC membership status creates a verification burden for borrowers.

Who Trinity Debt Management Is Best For and Not Recommended For

Ultimately, the right choice depends on your financial profile and priorities.

Best For

- Borrowers with $10,000 or more in credit card or medical debt.

- People with steady income who can commit to three to five years of monthly payments.

- People who want a full repayment plan without bankruptcy or settlement.

- People who value a faith-aligned counseling environment.

Not a Good Fit For

- People already deep into delinquency who need fast creditor intervention.

- People who need faster principal reduction than a DMP provides.

- Borrowers in Kansas, Montana, Nevada, New York, or Rhode Island.

- People who require full fee transparency before any phone call.

- People whose debts are mainly payday loans, secured loans, or tax debt.

Trinity Debt Management Alternatives

In summary, Trinity’s strengths are its operating history and counseling culture. Its gaps, however, are accreditation breadth, fee transparency, and geographic coverage. Accordingly, the alternatives below offer more verifiable credentials.

GreenPath Financial Wellness

- NFCC-accredited and A+ BBB rating.

- Available in all 50 states.

- Average setup fee around $35 and average monthly fee around $28.

- Fee schedule posted publicly.

ACCC (American Consumer Credit Counseling)

- NFCC-accredited.

- One-time $39 enrollment fee and average $25 monthly fee.

- Fees fully disclosed before enrollment.

Cambridge Credit Counseling

- NFCC-accredited.

- Average $40 setup fee and $30 monthly fee.

- Fee schedule publicly posted.

Therefore, if NFCC accreditation, BBB standing, and fee transparency are top priorities, GreenPath and ACCC offer more verifiable oversight. By contrast, Trinity’s case rests on longevity and counseling style. Indeed, neither is better in every dimension; instead, the right choice depends on what matters most to the borrower.