“The impact of low interest rates is broad and deep. Many Americans rely on interest income from their savings to help cover their cost of living.” – John Delaney

The prime rate in the U.S. sits at 6.75%. This benchmark directly influences the interest rates banks and lenders charge on consumers.

But most don’t quite understand how interest rates work on personal loans, savings accounts, credit cards, and other financial products.

That’s why understanding how these figures work can save you money or help you earn more on your savings.

What Are Interest Rates?

Interest rates represent the cost of borrowing money or the return you earn on interest when you save.

How Interest Rates Work

Fixed interest rates lock one rate in for the life of your loan, keeping payments consistent. You know what you’ll owe every month, so budgeting is easy.

Variable interest rates are based on market conditions, so your payments can rise or fall. You could be offered a lower cost to start, but rates can rise if the Federal Reserve changes policy.

On savings accounts, interest means your earnings can increase when rates rise.

Why Do Interest Rates Exist?

Interest rates serve three functions: compensating lenders for risk, rewarding savers, and helping regulate the economy.

Lenders Need to Make Money and Stay Protected

Every financial institution faces non-repayment risk, so charging interest offsets that potential loss. The rate provides profit margins that keep lending operations sustainable and allow continued loan offerings.

Interest Encourages People to Save or Invest

When you put money into a bank or credit union, they pay interest income. This incentive makes saving more appealing than spending.

Interest Rates Help Keep the Economy Steady

“Interest rates are used to achieve overall economic stability.” – Ben Bernanke

Rising interest rates drive up borrowing costs, slowing consumer spending and loan demand.

Lower interest rates make mortgage loans and business financing affordable, encouraging borrowing and spending. The Federal Reserve uses the federal funds rate to influence cycles and support economic growth.

Read More: What Does a Loan Processor Do? A Complete Guide on Requirements, Skills, Salary, & More

Who Determines Interest Rates?

- Central banks set baseline rates, while individual lenders adjust them based on risk, loan costs, and market conditions.

- The fed funds rate is set by the Federal Reserve and acts as a basis for all other interest rates.

- When the central bank raises or lowers the benchmark, credit card rates, mortgage rates, and auto loan rates may jump.

- While the Fed doesn’t set specific loan term rates, its policies influence what consumers pay their lenders.

- Interest also becomes the baseline for banks and credit unions.

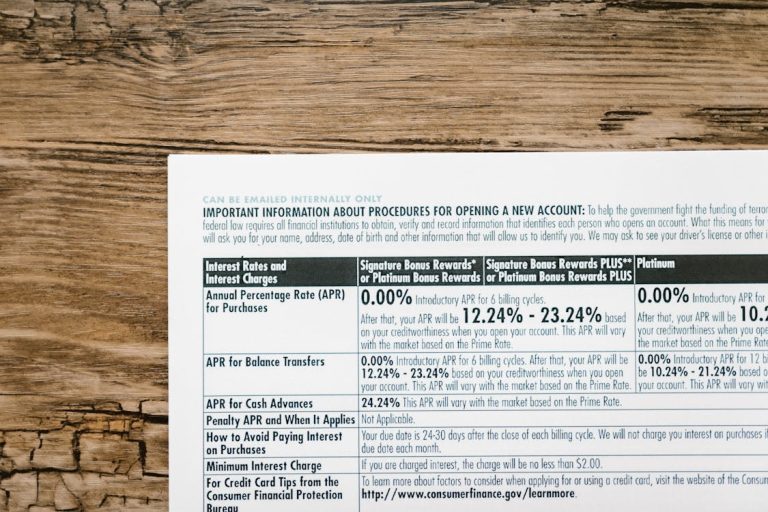

- If you have a good credit rating, your annual percentage rate (APR) will be lower, whilst bad credit makes it much higher.

- Lenders look at borrowing costs, operational prices, and default risk to arrive at the final rates offered to borrowers.

When Are Interest Rates Applied?

- Interest is charged when you borrow, carry a balance, repay a loan, or earn interest from savings.

- Interest starts adding up as soon as you collect loan money, though some lenders have short grace periods.

- Carrying credit card debt past the due date means the interest owed compounds on your unpaid balance each cycle.

- Compound interest grows faster with daily calculations compared to monthly or annual schedules on the same balance.

- Interest-bearing accounts pay you for deposits, letting your savings generate interest earned over time automatically.

Where Are Interest Rates Used?

Below are the banking services where interest rates apply:

When You Borrow Money

- Personal Loans – interest dependent on credit and income; can be used to cover home repairs or emergencies

- Mortgages – Home loans with small rate differences can result in big cost differences

- Student Loans – Accumulated interest may multiply while attending school

- Auto Loans – Interest adds thousands to vehicle cost beyond sticker price

- Credit Cards – Interest is charged daily on balances

- Payday Loans – Short-term loans with very high interest rates

When You Save or Invest

- High-Yield Savings Accounts – Higher interest rates than the average savings account

- Certificates of Deposit (CDs) – Fixed interest rate for a specified term

- Bonds – Most bonds have fixed interest rates

- Stocks – High rates lower stock prices by increasing borrowing costs

You May Also Like: Origination Fee: What They Are, How They Work, and more

How Interest Rates Work: How Are Interest Rates Calculated?

Here are some tips for calculating your interest rates:

Use the Interest Formula

Simple interest uses this formula: Principal × Rate × Time to estimate costs. Borrow $2,000 at 6% for two years, and you pay interest totaling $240.

Multiply the principal balance by 0.06, then by 2 to get that amount. Your total repayment becomes $2,240, with $240 going strictly toward interest costs

Check Your Loan or Credit Terms

Review your mortgage loan or unsecured loan paperwork to confirm the rate and schedule. A $10,000 car loan at 4% over five years compounds monthly, affecting totals.

The APR gives you the yearly cost, but compounding frequency changes outcomes. Adjustable-rate mortgages can shift rates mid-term, altering your mortgage payments and final costs.

Use Online Calculators

Online tools estimate interest owed based on the amount, rate, and repayment timeframe entered. Some calculators compare loans side by side or show savings from extra payments.

Others demonstrate how compound interest grows compared to simple calculations over identical terms. These tools help you avoid paying interest unnecessarily by visualizing different repayment strategies.

What Affects the Interest Rate You Receive?

Lenders adjust rates based on credit score, income, loan size, and debt-to-income ratio.

Credit Score

A good credit score above 670 signals a reliable repayment history to lenders reviewing applications. Higher scores typically qualify you for lower interest rates because you present less default risk

Income and Employment

Steady employment and consistent income demonstrate your ability to make regular interest payments. Lenders offer better rates when your job history shows stability and sufficient earnings flow.

Loan Amount and Term

Larger loans and extended repayment periods increase lender risk over the loan period significantly. Market interest rates rise on these products because income or expenses can shift dramatically.

Debt-to-Income Ratio (DTI)

Your DTI shows what percentage of your monthly income already goes toward existing borrowing costs. High ratios (above 36%) suggest limited capacity for new debt, prompting lenders to raise interest rates.

Why Do Interest Rates Change Over Time?

- Rates shift based on inflation, central bank policy decisions, and competitive market responses.

- When inflation rises, the Federal Reserve increases the target interest rate to reduce spending and stabilize prices

- Central banks adjust benchmark rates based on employment data, price growth forecasts, and overall economic trends

- Lenders monitor competitors and revise their own rates to attract borrowers or manage borrowing costs strategically

- Bond prices fall when rates rise because new bonds offer better returns than existing ones held

Managing Money When Rates Change

Adjust your personal finance strategy based on whether rates are rising or falling.

What to Do When Interest Rates Fall

- Consider investing money instead of keeping everything in low-yield savings accounts

- Diversify your portfolio to balance risk across different asset types

- Refinance your mortgage loan to lock in lower interest rates now

- Look at bonds or dividend stocks that benefit from low-rate environments

- Keep some safe investments like Treasury securities for stability

What to Do When Interest Rates Rise

- Cut unnecessary spending to free up cash for debt payments

- Pay off your highest-rate credit card debt first

- Consolidate multiple balances into one lower-rate loan if possible

- Borrow only what you actually need, not the maximum offered

- Skip purchases that require financing unless absolutely necessary

- Build an emergency fund to avoid paying interest on unexpected expenses

- Find extra income to pay down debt faster

Strategies to Avoid Interest Charge

- Build your good credit score by paying bills on time and reducing balances

- Borrow only when you actually need to, not for wants

- Save up for big expenses instead of financing everything

- Put more money down to lower your principal balance and interest owed

- Pick shorter loan periods to pay less interest total

- Pay credit cards in full monthly to avoid paying interest

- Never take cash advances since interest starts immediately