Borrowers make the minimum payment. The balance barely moves. Next month, they do it again.

Many borrowers carry $10,000 to $50,000 or more in credit card debt, medical bills, or personal loans. That cycle does not break on its own. The interest grows faster than most payments can cover. The calls from creditors do not stop while they look for a fix.

PDS Debt reviews describe a debt settlement company run by Puridy Financial, Inc. It negotiates with creditors to lower what borrowers owe. It also folds their balances into one monthly payment. But is it worth enrolling? What does it cost, and who does it help most?

This review pulls from Better Business Bureau (BBB) records, Trustpilot scores, real customer complaints, and public fee data. The aim is to help U.S. borrowers make a clear, informed call.

TL;DR PDS Debt at a glance

- Legitimate? Yes. PDS Debt is BBB-certified with an A+ rating. It is also certified by the International Association of Professional Debt Arbitrators (IAPDA). It has no Federal Trade Commission (FTC) or Consumer Financial Protection Bureau (CFPB) actions as of March 2026.

- Fees. 15 to 25 percent of enrolled debt, paid only after a settlement is reached.

- BBB rating. A+ and 4.93 out of 5 stars from 369 reviews.

- Best for. U.S. borrowers who hold $10,000 to $50,000-plus of unsecured debt and want structured, guided relief.

- Program length. Normally 24 to 48 months.

- Not for. People who want fast results, who hold secured debts, or who cannot accept a short credit score dip.

What is PDS Debt

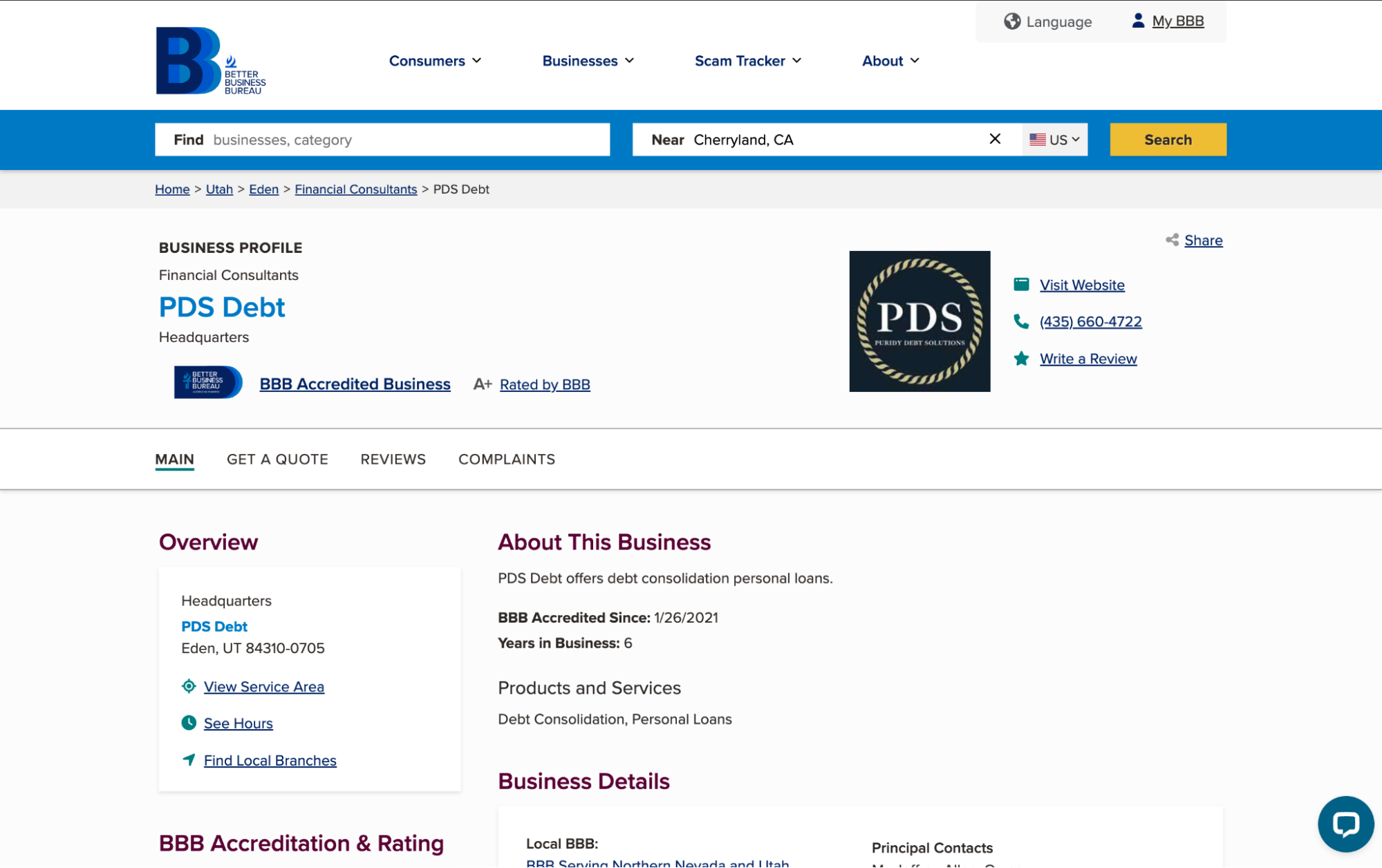

PDS Debt is a debt settlement company owned by Puridy Financial, Inc. Its website lists the address as 13520 Evening Creek Dr. N, San Diego, California 92128. Its BBB profile and third-party sources, such as LendEDU, list the registered address as Eden, Utah. The reason for this gap is not public. Borrowers should verify it with a representative before signing up.

PDS Debt has been BBB-accredited since January 2021 and holds an A+ rating through 2026. The company is also certified by the IAPDA, a recognized credential for debt negotiation pros.

PDS Debt works only with unsecured debt. That includes credit cards, medical bills, personal loans, and accounts in collections. It does not handle secured debt like mortgages or car loans. The company has also gained notice through podcast sponsorships, mainly in true crime and lifestyle shows.

One threshold matters. PDS Debt works best for borrowers with at least $10,000 in unsecured debt. For balances under $10,000, a do-it-yourself plan may serve better. Many experts suggest the debt snowball strategy to build momentum by clearing smaller balances first.

How PDS Debt works

The Consumer Financial Protection Bureau describes debt settlement firms as groups that negotiate with creditors to accept less than the full amount owed. Here is how the PDS Debt process works.

- Step one. Start with a free phone call or online form. No commitment is needed.

- Step two. A specialist checks eligibility. If a borrower does not qualify, they may be referred to a partner company. Borrowers should ask before agreeing to anything.

- Step three. Stop paying creditors directly. Put a set monthly sum into a personal, FDIC-insured savings account.

- Step four. Once the funds build up, PDS Debt contacts each creditor to negotiate.

- Step five. Settled accounts are closed. The full program usually runs 24 to 48 months.

PDS Debt charges no fee until a debt is settled. That is one clear sign of a fair service model.

PDS Debt services and programs

Debt settlement

Debt settlement is the main offering. The team negotiates enrolled unsecured balances down to less than the original amount owed. Results vary and are never guaranteed. Fees run 15 to 25 percent of enrolled debt and apply only after a settlement is reached, so there are no upfront costs. Monthly savings account fees are not public, so ask about them during the first consultation.

Debt consolidation support

PDS Debt sometimes uses consolidation language, but this is not a new loan. Enrolled debts merge into one monthly deposit in a dedicated savings account, which later funds settlements. The “0 percent interest” line in some ads points to the payment structure, not a loan product. This matters for anyone comparing PDS Debt to a balance transfer or a personal consolidation loan.

Financial education and counseling

PDS Debt advisors give budgeting guidance during the program. This fits the idea that personal finance is largely about protection. Clients manage debt risks now so they can build wealth later. Clients also get an online portal with visual progress tracking. Reviews on BBB and Trustpilot praise this feature, and it helps during a 24 to 48-month commitment.

PDS Debt fees and pricing

There are no upfront enrollment fees. That helps borrowers who are already stretched thin.

The main cost is a settlement fee of 15 to 25 percent of the total enrolled debt. It applies only after a debt is settled. Say a borrower enrolls $10,000 in credit card debt and PDS Debt settles it for $5,000. A 20 percent fee equals $2,000 based on the original enrolled amount. The total cost, the settled amount plus the fee, should still land below the original balance for the program to make sense.

Savings account maintenance fees are not public. Ask about them during the consultation.

There is also a tax issue many people miss. Per IRS guidance on canceled debt, forgiven debt usually counts as income and is taxed. Say a lender cancels $5,000 of a borrower’s debt. The borrower will likely get a 1099-C form and owe taxes on that sum. A tax advisor can confirm the details before enrollment.

For comparison, National Debt Relief charges up to 25 percent of enrolled debt. Freedom Debt Relief charges 15 to 25 percent. Accredited Debt Relief also charges 15 to 25 percent. PDS Debt pricing sits in line with industry norms. It is neither a bargain outlier nor a premium one.

PDS Debt reviews and customer complaints

To judge the real impact, look past marketing claims. Check the feedback from borrowers across independent review sites and regulatory databases.

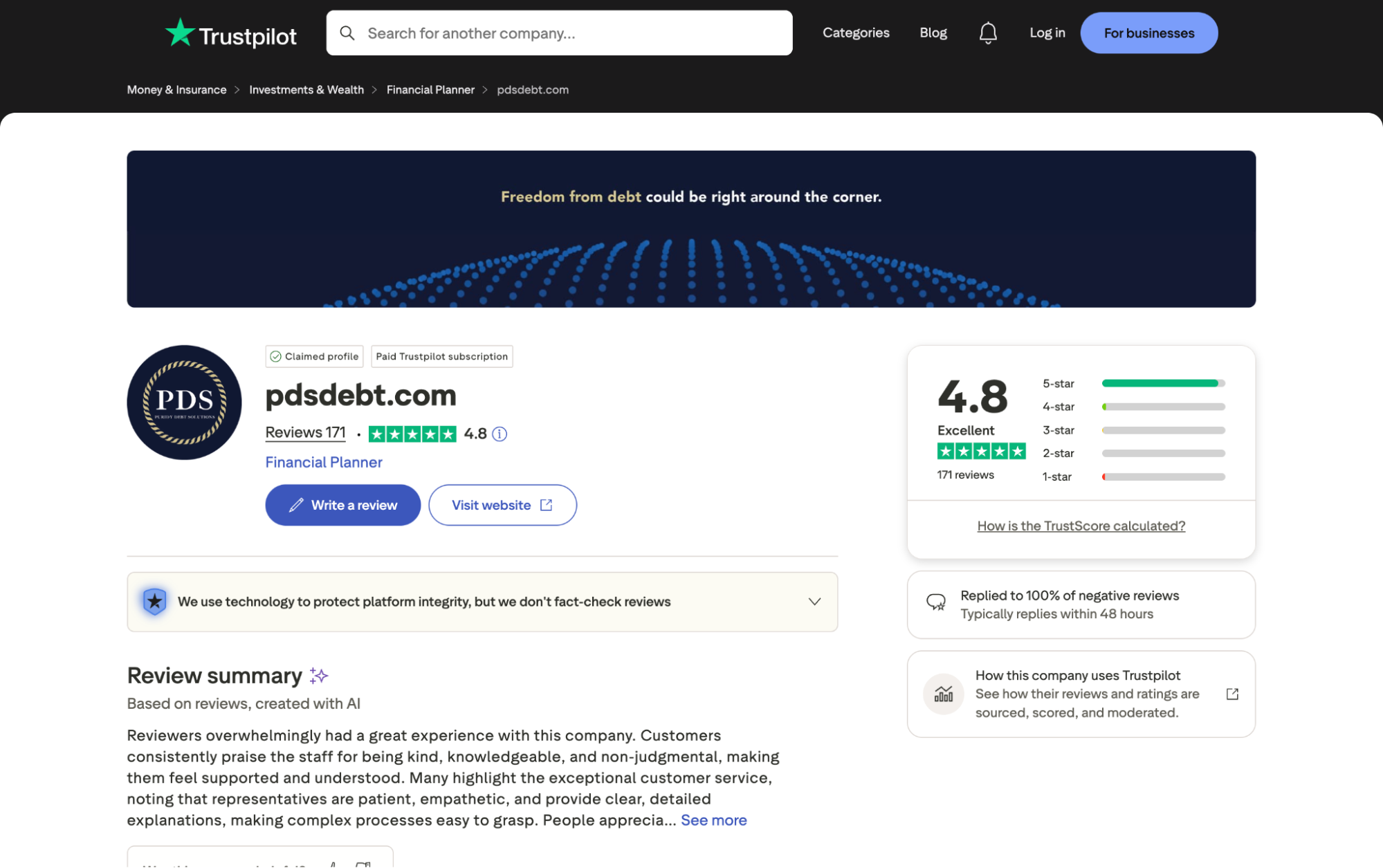

Trustpilot reviews

PDS Debt holds a Trustpilot rating of 4.8 out of 5 stars from 171 reviews as of early 2026. That score is high for a debt settlement firm, a field where delays and money worries drive many complaints.

Reviewers often praise advisors who stay non-judgmental, explain options in plain terms, and give calm consultations. Customers name individual advisors often. That points to steady, personal service rather than a generic call center.

BBB reviews

PDS Debt has held an A+ BBB accreditation since 2021. It averages 4.93 out of 5 stars from 369 reviews as of 2026.

One real BBB example stands out. A couple enrolled in November 2024 and had three of seven accounts settled by August 2025, about nine months in, with their credit score starting to recover. That is a realistic look at what the program can do.

One complaint deserves attention. A BBB reviewer said they were moved to a third-party company without clear notice. If a partner referral comes up, ask for the company name, the fees, and the credentials before consenting.

No FTC or CFPB enforcement actions have been filed against PDS Debt or Puridy Financial as of March 2026.

Reddit reviews

Is PDS Debt legit?

byu/TCmotivation indebtfree

Reddit threads, mainly in r/personalfinance and r/debtfree, run more cautious than BBB or Trustpilot. That is normal for the platform. Common posts question credit score impact, program length, and the affiliate referral concern also seen on BBB.

Most of these posts come from people still researching, not those who finished the program. The verified review sites give a fuller picture of real outcomes.

Common PDS Debt complaints worth knowing

- Credit score drop. Stopping creditor payments pushes accounts past due, which hurts credit scores. This happens with every debt settlement program, not just PDS Debt. The dip is real but temporary. Once the debt clears, borrowers can start to rebuild.

- Long timeline. A 24 to 48-month plan is a serious commitment. People who expect fast results often feel frustrated. Clear expectations help before enrolling.

- Affiliate referrals. Borrowers who do not qualify may go to a partner company without a full explanation. Always ask who that company is and what their terms are first.

- Tax surprise. Forgiven debt can count as taxable income under IRS rules. This is not a PDS Debt policy, but many borrowers learn it too late. Talk to a tax pro first.

PDS Debt outcomes and success rate

The performance-based fee model is a strong sign of a results-driven service. The company earns a fee only when a debt is settled, so its incentive ties directly to client outcomes.

BBB data backs this up. The couple who signed up in November 2024 had three of seven accounts settled in under nine months. That is an achievable pace for a multi-account program. Cases do not always move that fast, but it shows real progress within the first year.

Industry timelines run 24 to 48 months. Savings vary and are never guaranteed. Whether a creditor agrees to settle depends on account age, creditor policies, and total enrolled balance. The CFPB urges borrowers to understand the risks, including credit score impact and tax effects, before they enroll in any debt settlement program.

PDS Debt pros and cons

A lower balance brings long-term value, but it carries a short-term hit to credit and taxes.

Pros

- No upfront fees. Payment comes only after results.

- A+ BBB rating and IAPDA certification. These credentials add industry-standard trust.

- Free, no-commitment consultation. Borrowers can explore options at no cost.

- Online portal for progress tracking. Clients can watch settlement status in real time.

- Helpful advisors. Staff earn praise as professional and supportive.

- Simpler payments. One monthly deposit replaces many creditor payments.

Cons

- Credit score declines during enrollment. The hit is temporary but expected.

- Settlement fees. Costs run 15 to 25 percent of enrolled debt.

- Long commitment. The program runs 24 to 48 months, so it is not fast.

- Affiliate transfers. Some customers moved to partner firms without clear notice.

- Eligibility limits. Mortgages and car loans do not qualify.

- Tax effects. Forgiven debt may count as taxable income under IRS rules.

The gap between the San Diego address on the website and the Eden, Utah address on BBB has not been explained.

Who PDS Debt is best for

The best path depends on the total balance, the type of debt carried, and how much credit impact a borrower can accept.

Best for

- U.S. borrowers with $10,000 to $50,000-plus in unsecured debt who can no longer keep up with minimum payments

- People who want a performance-based fee model with no upfront costs

- Borrowers ready for a 24 to 48-month commitment in exchange for a structured path out of debt

- People who value regular advisor check-ins, clear progress tracking, and a supportive experience

Not recommended for

- Anyone who needs a fast or short-term fix

- Borrowers whose main debt is secured, such as a mortgage, car loan, or home equity line

- People who cannot accept a short drop in their credit score

- Anyone who has not yet looked at nonprofit debt management plans or personal consolidation loans as lower-impact options

How to apply for PDS Debt relief

- Visit pdsdebt.com or call to start the free debt assessment. It takes a few minutes with no commitment.

- Enter your total unsecured debt amount and basic contact details.

- A debt specialist reviews your eligibility and explains options in plain language.

- If approved, you get a custom plan with the monthly deposit amount, estimated timeline, and fee structure.

- Sign the service agreement. A personal, FDIC-insured savings account is set up.

- Begin monthly deposits while PDS Debt watches accounts for settlement chances.

- Track progress in real time through the online client portal.

Note. If PDS Debt refers you to a partner company, ask for that company name, fee structure, and accreditation before you agree to the transfer. Do not assume their terms match what you discussed with PDS Debt.

PDS Debt vs top debt settlement alternatives

PDS Debt is a highly rated provider. Still, a look at the largest firms shows clear gaps in minimum requirements, program guarantees, and the level of personal service borrowers can expect.

PDS Debt vs National Debt Relief

National Debt Relief has run since 2009 and has resolved over $15 billion in enrolled debt, a deeper track record by volume. Its minimum enrolled debt is $7,500, and it shares average savings data upfront. PDS Debt stands out with more one-on-one advisor support and higher overall satisfaction in reviews. That makes it a better pick for people who want a personal experience.

PDS Debt vs Freedom Debt Relief

Freedom Debt Relief needs a $7,500 minimum in enrolled debt and offers a program cost guarantee for added predictability. Both charge 15 to 25 percent of enrolled debt. PDS Debt scores higher on Trustpilot per-review ratings, which hints at a better day-to-day experience.

PDS Debt vs Accredited Debt Relief

Accredited Debt Relief needs at least $10,000 in enrolled debt and shares more specific savings projections upfront. Both use a performance-based fee model. PDS Debt suits borrowers who want a personal, advisor-led experience over a data-forward one.