According to a new survey by The American Institute of Stress (AIS), the biggest source of emotional stress for 50% of Americans is financial (money worries, cost of living, unemployment, mortgage, and debt).

These pressures can push people to alternative borrowing options like Uprova, leading them to search for Uprova reviews.

So, if you’re weighing Uprova as an option, this review breaks down what borrowers actually experience to give you context and perspective before you commit.

What Is Uprova?

Uprova Credit LLC is owned by the Habematolel Pomo of Upper Lake, a federally recognized Native American sovereign based in California.

Since the company operates under tribal law, it isn’t required to follow state lending rules.

This legal setup allows Uprova to bypass interest rate caps and other consumer protections that apply to most non-tribal lenders.

Uprova Loan Details: Rates, Terms, Requirements, Availability

| Detail | Information |

|---|---|

| Loan amounts | $300 – $5,000 |

| APR range | 34.5% – 35.99% |

| Terms | 6 to 36 months, depending on loan type |

| Funding speed | Often same-day or next business day if approved early |

| Availability | Not available in all states due to tribal regulations |

| Minimum credit score | No strict minimum; Uprova accepts bad credit borrowers |

What Loans Does Uprova Offer?

Uprova offers personal installment loans that can be used for things like medical bills, urgent repairs, or paying off high-interest debt.

You get a lump sum upfront, then repay it over time in fixed payments. If you pay on time, Uprova reports your activity to the credit bureaus, which may help improve your credit over time.

Who Qualifies for Uprova?

Uprova loans are available to U.S. residents who live in eligible states, are at least 18 years old, have a verifiable source of income, and maintain an active checking account.

This lender does not require a minimum credit score, making it accessible to borrowers with bad credit.

What Fees Does Uprova Charge?

Uprova advertises rates that fall between 34.5% and 35.99% APR, depending on the loan. This range includes most of the cost to borrow, since the company doesn’t usually break out separate origination fees.

Late fees depend on the loan terms you agree to. They’re not fixed across all loans, so the final details will be spelled out in the contract.

The same goes for your payment schedule and total repayment cost.

There’s no penalty for paying the loan off early, and doing that could lower the amount of interest you end up paying.

How to Apply for a Uprova Loan

The application starts at the Uprova website and takes only a few minutes. You’ll be asked for basic information, and checking your rate won’t affect your credit score.

Once submitted, Uprova uses its internal system to make a quick decision based on your application. If approved, you’ll see your offer and repayment terms right away.

Funding is usually fast. In some cases, customers receive funds within 30 minutes using the Instant Funding option, depending on bank processing.

However, standard bank transfers may take longer, especially if submitted after business hours. Prepaid cards also aren’t eligible, and same-day funding through ACH might include extra fees, depending on your bank.

Benefits of Using Uprova

Uprova markets itself as a faster and more accessible option for borrowers who need money quickly but can’t qualify through traditional lenders.

These are the features that stand out for borrowers who value speed and flexibility, according to Uprova reviews.

Fast Funding

Once approved, many borrowers receive their funds the same day or by the next business day. Depending on the time of approval and the funding method selected, instant transfers are also available through select banks.

Bad Credit Accepted

Uprova does not require a minimum FICO score, which opens the door for applicants who may have been denied elsewhere. Approval is based on income and banking history rather than strict credit thresholds.

Flexibility

Compared to payday loans, Uprova’s installment structure gives borrowers more time to repay. Payments are scheduled over a fixed term rather than being due in full by the next paycheck.

Online Application

The whole process happens online. You won’t need to print anything or send paperwork, and once you apply, you usually get a decision pretty quickly.

It saves time, especially if you need funds without delays or back-and-forth calls.

Risks and Limitations

While Uprova promotes fast access and flexible credit checks, borrowers should weigh the following downsides carefully.

Very High APRs

Although Uprova advertises rates around 35%, Uprova reviews frequently mention effective APRs in the 300% to 800% range once repayment terms are factored in.

At that cost, even small loan amounts can become difficult to repay on time.

Tribal Sovereignty

Because Uprova operates under tribal law, its loans are not bound by state-level rate limits or consumer protections.

If issues arise, such as billing disputes or unauthorized charges, borrowers may find that normal legal channels don’t apply.

Aggressive Collection Reports

Some users have reported repeated automatic withdrawals and trouble stopping ACH payments after asking Uprova to cancel them. They described these collections as multiple debits after attempting to close the account.

Not Available Nationwide

Since availability is limited to approved locations, this can create confusion if borrowers apply without realizing their state is excluded.

It’s worth noting that the Washington State Department of Financial Institutions has warned that Uprova is not licensed to lend in Washington.

Auto-Funding Without Approval

There are also reports of applicants receiving funds even though they believed they hadn’t completed or accepted the offer. This risk can lock you into repayment terms you didn’t knowingly agree to.

Uprova Reviews

Uprova reviews vary on these review sites, forums, and third-party databases:

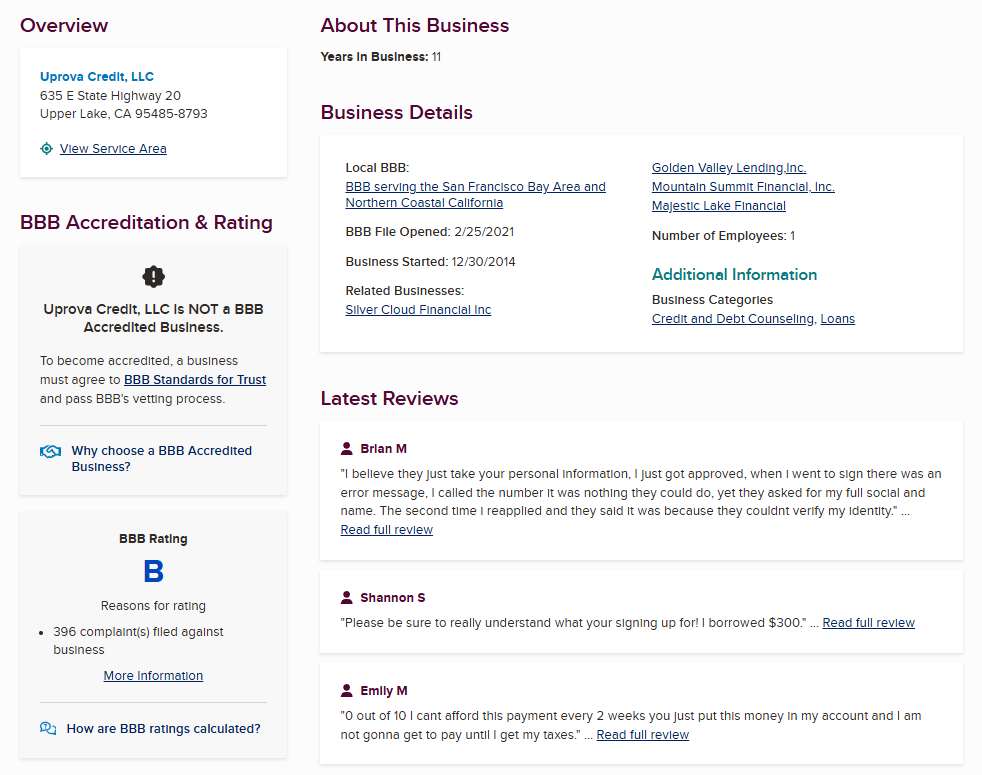

Better Business Bureau (BBB) Reviews

Uprova is not accredited by the BBB but currently holds a B rating. Based on 63 reviews, the average customer rating is 1.17 stars.

Additionally, 396 complaints were filed in the last three years, and 164 were closed in the past 12 months.

The most common negative reviews relate to high interest rates, confusing repayment terms, and unexpected charges.

Most borrowers report effective APRs of 360–600%, far exceeding what Uprova advertises during the application process.

Customers describe making dozens of payments while their principal balance barely decreases over time.

Borrowers also report that no hardship options are available and that they have difficulty stopping automatic withdrawals from their bank accounts.

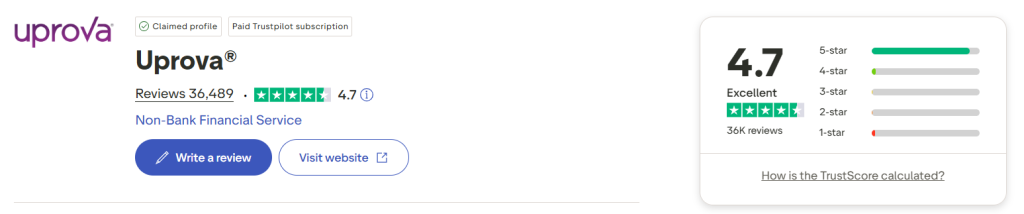

Trustpilot Reviews

On Trustpilot, Uprova has a very different reputation. With over 36,000 reviews, it holds a 4.7 rating.

Most positive reviews praise the fast funding speed, easy online application, and access for bad credit borrowers.

However, even satisfied customers frequently acknowledge the excessively high interest rates.

Reddit Reviews

Uprova reviews: Is it legit or scam?

by

u/PomegranateDense9615 in

financeonloans

Most describe Uprova as a last-resort option, useful only in emergencies. Even the positive experiences are usually paired with strong cautions to read every line of the contract and to pay off the balance quickly.

Additional insights from independent platforms like LoanForum reinforce this mixed view.

While some praise the fast application and near-instant deposits, others report extremely high APRs, sometimes above 600%.

Others raised technical problems, such as login failures and slow customer service responses. They also mentioned issues with debit card verification.

When to Use Uprova

Uprova isn’t built for long-term financial planning or low-cost borrowing. It’s a short-term option, and the situations where it might make sense are limited.

Here are two cases where some borrowers have found it useful.

You Have No Other Options

If you’ve been denied by banks or credit unions and need to cover an emergency – like car repairs, rent, or medical bills – Uprova may approve you.

The lender doesn’t rely heavily on credit scores, which gives borrowers with bad credit a possible fallback when other lenders say no.

You Need Cash Fast

Speed is one of the few areas where Uprova consistently delivers. In some cases, funds are deposited within 30 minutes after approval, depending on the time of day and your bank.

If timing matters more than cost, this fast turnaround can be helpful.

When to Avoid Uprova

Below are some situations where you may not want to try out Uprova.

You Qualify Elsewhere

If you can get approved through a credit union, bank, or online lender, you’ll likely pay much less interest.

Some banks also offer payday alternative loans with capped rates and better repayment terms. These options may take longer, but they cost less over time.

You Can’t Afford High Interest

Uprova loans typically have APRs of more than 300%, even if the advertised APR is lower.

This type of cost can turn a loan into an expensive burden, especially if you have limited income or your finances are already stretched thin.

If you’re not sure you can do that, the loan could end up being more of a headache than a solution.

Is Uprova Legit?

Yes, Uprova is a legally recognized lender owned and operated by the Habematolel Pomo of Upper Lake, California.

Uprova’s lending practices operate under tribal laws, which don’t make it a scam but do make it risky. The company uses legal protections that allow it to charge rates that most traditional lenders can’t.

How Uprova Compares to Other Lenders

| Lender | Loan Amount | APR / Cost | Turnaround Time |

|---|---|---|---|

| Uprova | $300 – $5,000 | 34.5% – 35.99% APR (advertised); actual rates may be higher | Same-day or next business day |

| Brigit | $50 – $250 | $8.99 – $14.99/month; no interest | 1–3 business days; instant with Premium |

| CreditNinja | $300 – $5,000 | Varies by state and borrower profile | 1–2 business days |

| OppLoans | $500 – $5,000 | 160% – 195% APR | Same business day |

| EarnIn | Up to $1,000 | Free or $3.99+ per instant transfer | 1–2 business days; minutes with Lightning Speed |

| Varo | $20 – $500 | Flat fee of $1.60 – $40; no membership fee | Instant (once qualified) |

| Cleo | $20 – $250 | $5.99/month; $3.99 for instant transfer | 3–4 days; instant for a fee |

| Current | $50 – $750 | Free; small fee for instant delivery | Up to 3 days; within an hour for a fee |

| Possible Finance | $50 – $500 | 150% – 200% APR | As fast as 1 business day |