Many Americans rely on credit to keep up with expenses, and the Federal Reserve reported a 2.2% seasonally adjusted annual rate increase in consumer credit for February 2026.

As borrowing grows, many people are turning to short-term financing, such as personal loans and lines of credit, for quick access to funds when budgets fall short.

This interest has sparked more searches for CreditFresh reviews, especially from borrowers trying to understand how this line of credit works and whether it’s a practical option for short-term needs.

What Is CreditFresh?

CreditFresh launched in 2019 and operates online from its base in Newark, Delaware. It works with FDIC-insured banks like CBW Bank and First Electronic Bank to offer personal lines of credit.

As of November 2025, CreditFresh is available in 33 states, though availability can change.

How Does a CreditFresh Line of Credit Work?

A CreditFresh line of credit gives you access to a reusable credit limit between $500 and $5,000. You can prequalify without a credit check to see your estimated limit.

If approved, you can draw funds online in any amount within your limit. Requests made before 3:30 p.m. Eastern on business days may be processed the same day.

Payments usually follow your income schedule, either biweekly or monthly, making it easier to stay on track.

CreditFresh Loan Details: Terms, Limits, Fees, Availability

| Detail | Information |

| Loan Type | Personal Line of Credit |

| Credit Limit | $500 to $5,000; Up to $15,000 for FreshLine |

| Application Method | Online only |

| Approval Time | Same day possible (if verified early) |

| Funding Speed | Same business day if requested by 3:30 p.m. ET |

| Repayment Schedule | Biweekly or monthly (based on income) |

| Minimum Payment Includes | Billing cycle charge + required principal |

| Fees | No origination or prepayment fees |

| Billing Cycle Charge | Based on average daily principal balance |

| Reports to Bureaus | Yes |

| Credit Check | Soft pull for prequalification |

| Availability | Select U.S. states |

| Customer Support | Phone and email |

Where to Use a CreditFresh Line of Credit

CreditFresh is most suitable for the following expenses:

- Emergency costs: Covers urgent needs like car repairs, medical bills, or fixing something critical at home.

- School expenses: Can help pay for textbooks, fees, or tuition.

- Unplanned project costs: Useful for events or projects where costs change, like home repairs or caregiving.

- Paying off debt: May help simplify repayment if you use it to cover high-interest debt.

- Bills or large purchases: Helps with shortfalls when paying rent, utilities, or buying items that don’t fit your paycheck.

Who’s Eligible for a CreditFresh Line of Credit?

To qualify for a CreditFresh line of credit, you need to be of legal age in your state, have a steady income, an active bank account, and a valid phone number and email. You must also be a U.S. citizen or permanent resident.

CreditFresh doesn’t offer products to active-duty military members or their dependents due to Military Lending Act (MLA) rules. Applications are reviewed individually, and there’s no option to apply with a co-applicant.

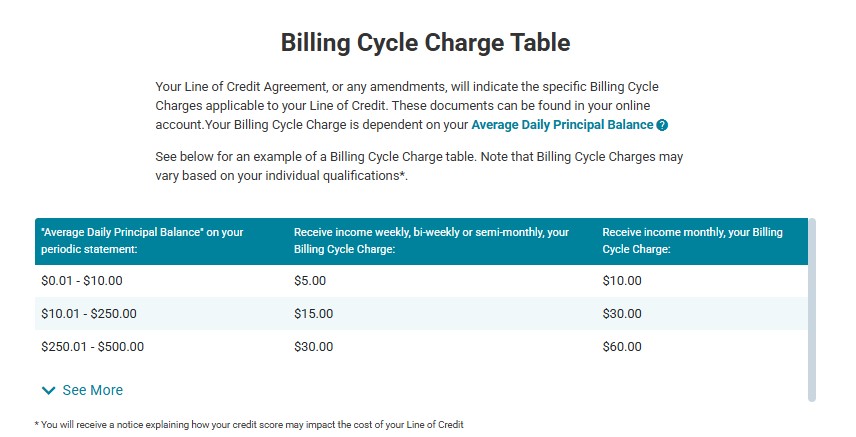

What Are CreditFresh’s Costs and Fees? (With Computation Example)

CreditFresh doesn’t use a standard APR. However, each billing cycle includes a billing fee and a required principal payment, both based on your average daily balance. These two charges make up your minimum payment.

Example 1: Monthly Income Frequency

In this setup, payments occur about once every 30 days. If you borrow $1,500, here’s how the first three months would look:

| Billing cycle | 1 | 2 | 3 |

| Balance | $1,500 | $1,470 | $1,440.60 |

| Principal payment | $30 | $29.40 | $28.81 |

| Billing cycle charge | $184 | $184 | $184 |

| Min. payment | $214 | $213.40 | $212.81 |

| New balance | $1,470 | $1,440.60 | $1,411.79 |

After three months, you would have paid $552 but still owe over $1,400. This is due to the billing cycle cost, which stays high even as the balance decreases.

Example 2: Non-Monthly Income Frequency

With payments scheduled about every 14 days, the cycle charge is lower but applies more frequently. Here’s a breakdown using a $1,500 draw:

| Billing cycle | Balance | Min. payment | New balance |

| 1 | $1,500 | $100 | $1,485 |

| 2 | $1,485 | $99.85 | $1,470.15 |

| 3 | $1,470 | $99.70 | $1,455.45 |

| 4 | $1,455.45 | $99.55 | $1,440.90 |

| 5 | $1,440.90 | $99.41 | $1,426.49 |

| 6 | $1,426.49 | $99.26 | $1,412.23 |

Each payment includes a required principal amount and an $85 billing cycle fee. There are no extra charges, but the total cost can still be higher than a typical personal loan.

For example, a $1,500 loan at 12% APR would drop to about $1,288 after three months, with lower monthly payments and a cheaper long-term cost.

How to Repay Your CreditFresh Line of Credit

CreditFresh sends your statement at least 14 days before the due date. It includes your minimum payment and the exact date it’s due.

You can set up automatic payments by submitting an authorization form. If approved, payments are pulled directly from your bank account on the scheduled date.

If you prefer manual payments, you can log in and use a debit or prepaid card through the secure online portal. There’s no need to contact support.

As long as you have a balance, you must make at least the minimum payment each billing cycle.

How to Apply for a CreditFresh Line of Credit

CreditFresh accepts applications online only. You’ll need a checking account, and in some cases, you may be asked to upload documents for verification.

- Step 1: Apply online

- Fill out a short form with your basic details. Most people finish this in a few minutes.

- Step 2: Verify and get approved

- After submitting, you’ll be asked to request a credit limit and confirm your identity and bank account. You can verify your account instantly using DecisionLogic or by phone if needed. If that’s not possible, upload documents like a pay stub, utility bill, or ID.

- Step 3: Request funds

- Once approved, log in and request a draw. If you do it before 3:30 p.m. Eastern on a business day, the money may arrive the same day.

Benefits of Using a CreditFresh Line of Credit

According to user reviews on platforms like Reddit, here are the advantages of using CreditFresh:

- Fast access to funds: Submit a draw by 3:30 p.m. ET on a business day, and funds may arrive the same day.

- No hidden fees: Only pay the clearly stated billing cycle charge; no extra fees or prepayment penalties.

- Pay only for what you use: Charges apply only to borrowed amounts; no borrowing means no billing cost.

- On-time payments may help: Timely payments can lead to lower charges and possible credit limit increases.

- Build credit history: CreditFresh reports payments, which may help improve your credit with consistent use.

- Prequalify without a hard pull: Checking eligibility won’t affect your credit score.

Risks of CreditFresh Lines of Credit

Depending on your situation, below are the limitations, according to users, that could affect the platform and the loan’s usefulness:

- No standard APR: CreditFresh doesn’t use a fixed interest rate. The billing cycle charge depends on your balance, not a set percentage.

- Costs add up fast: Fees apply each billing cycle, even on small draws. The overall cost can be high.

- Vague requirements: There’s no clear minimum credit score or income info on the CreditFresh website.

- Not nationwide: The personal line of credit is only available in select states. New Mexico isn’t one of them.

- Lower limits: The credit limit tops out at $5,000. Other lenders may offer much more.

CreditFresh Reviews

Customer feedback on CreditFresh varies widely.

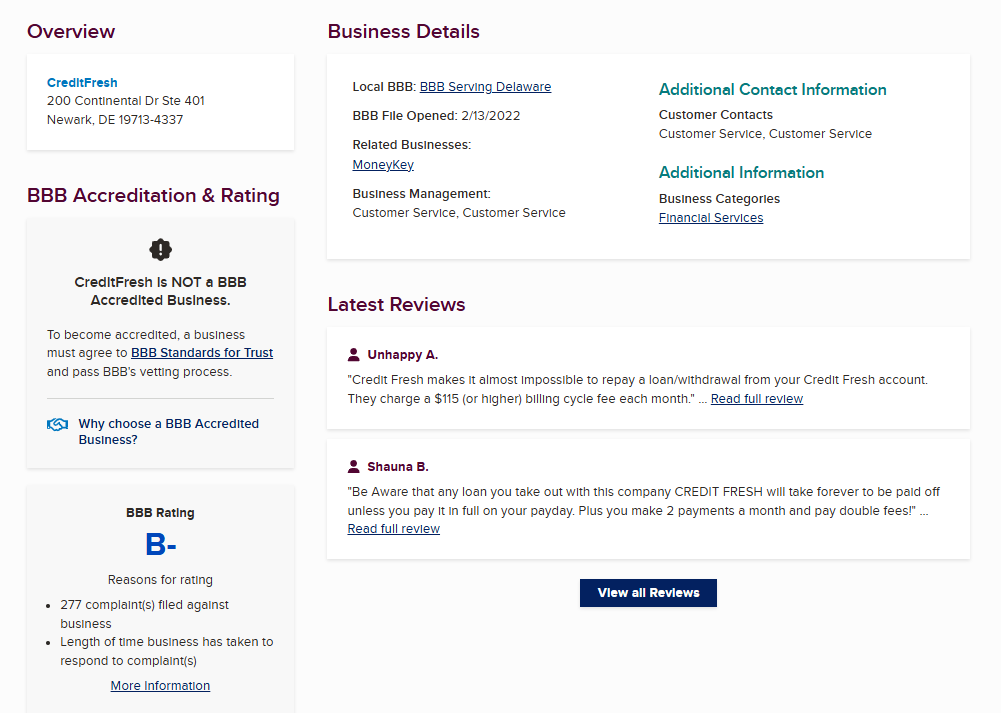

Better Business Bureau (BBB) Reviews

CreditFresh isn’t accredited by the BBB and holds a B- rating.

Over the past three years, more than 200 complaints have been filed. Many focused on billing issues, high fees, and how little each payment reduces the balance.

The two public reviews on the BBB site average 1.5 stars, with both reviewers warning that the fee structure makes the loan extremely difficult to pay off.

One notes that most of each payment goes toward billing cycle fees rather than the principal, while the other cautions that without paying the full balance immediately, repayment can drag on indefinitely.

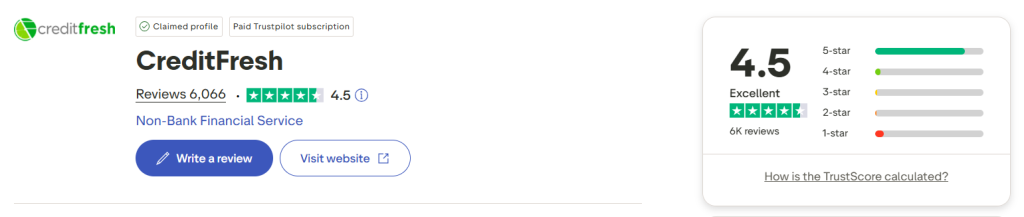

Trustpilot Reviews

CreditFresh holds a 4.5-star rating on Trustpilot. Many reviewers like the fast approval, easy access to funds, and simple account management through the dashboard.

Some, though, point out the high fees and slow balance reduction. A few say most of their payment goes toward charges, not the actual amount borrowed.

While the feedback leans positive overall, users stress the importance of reading the terms carefully before committing.

Reddit Reviews

Most Reddit users speak negatively about CreditFresh. Many say it’s expensive and hard to pay off, with payments mostly going toward fees instead of the balance. Some shared they paid for months and saw barely any change in what they owed.

What are the reviews like for CreditFresh? Any major concerns or praises?

byu/Haripriya_DM1234 infinanceonloans

A few noted being charged hundreds in billing fees while barely touching the principal. Others mentioned the account didn’t show up on their credit report right away, or flagged aggressive collections and unclear terms.

Still, some said it helped when they had no other option. They liked the fast access to funds and having a credit line ready for emergencies, but only because they paid it off fast.

Is CreditFresh Right for You?

CreditFresh may be a suitable option in certain situations, but not all borrowers will benefit from its structure.

When It May Make Sense

Here’s when to use CreditFresh:

- Other lenders said no: If you’ve been denied elsewhere, CreditFresh may still approve you based on consistent income and credit history.

- You need fast money: The online application is simple, and same-day funding is possible for urgent expenses.

- Short-term gap: If your budget is tight for a few weeks, this line of credit can help cover a net for any unexpected costs.

When to Avoid CreditFresh

Here’s when to avoid CreditFresh:

- You qualify elsewhere: A traditional personal loan or low-rate credit card may cost less in interest and fees.

- You need time to repay: This isn’t a long-term financial solution. Balances can grow fast if unpaid.

- Fees worry you: The billing cycle charge can feel like high fees. If you’re fee-sensitive, this may not be the right fit.

CreditFresh vs. Other Lenders

| Product | Loan Amount | Turnaround Time | Requirements |

|---|---|---|---|

| CreditFresh Personal Line of Credit | $500–$5,000 (up to $15,000 for FreshLine) | Same business day if requested by 3:30 p.m. ET | Online application only; same-day approval possible if verified early |

| OppLoans Installment Loans | $500–$5,000 | As soon as the same business day | Must be 18+, receive pay via direct deposit, earn at least $1,500/month, and live in an eligible state |

| CreditNinja Installment Loan | $300–$5,000 | 1–2 business days | Checking account must be at least 60 days old, steady income via direct deposit, eligible state, and meet your state’s age of majority |

| EarnIn | Up to $150/day, max $1,000 between paydays | 1–2 business days; minutes with Lightning Speed | Must be 18+, a US resident with a valid SSN, at least 60 days of banking history, consistent direct deposit income, and a positive balance |

| Current | $50–$750 | Up to 3 days; within an hour for a fee | Must deposit at least $500 in monthly payroll into a Current account |

| Chime MyPay® | Up to $500 | Within 24 hours; instant for a fee of $2–$5 | Requires a Chime checking account, direct deposits of at least $200, and residency in a supported state |

| Varo Cash Advance | $20–$500 | Instant once approved | Requires an active Varo Bank account in good standing and at least $800 in qualifying direct deposits, though exact limits depend on deposit history and account activity |

| Cleo | $20–$250 | 3–4 days; instant for a fee | Not stated |