According to Cotality’s Homeowner Equity Report (HER) for Q4 2025, borrower equity declined by $78.8 billion, or 0.5% year over year. On average, homeowners lost about $8,500 in equity between Q4 2024 and Q4 2025, bringing accumulated home equity to around $295,000 per borrower.

Despite the decline, equity remains a valuable financial resource. It can cover unexpected expenses, fund home improvements, and bridge income gaps.

Splitero is one way to access it. The question is whether it is a safe and legit home equity investment (HEI) provider.

What Is Splitero?

Splitero, based in San Diego, California, is a financial technology company that provides homeowners with a lump sum of cash in exchange for a share of their home’s future value.

Splitero Home Equity Investment Amounts, Terms, Requirements, Availability

| Category | Details |

| Investment amounts | $50,000–$500,000 or up to 25% of home value, based on equity and location |

| Minimum home equity | 30% equity must be retained (maximum 70% CLTV) |

| Term length | Matches existing mortgage term (10–30 years); extension may be available |

| Repayment structure | No monthly payments; repay via sale, refinance, or cash buyout; capped at 17.99% annual rate (safety cap) |

| Availability | Available in AZ, CA, CO, FL, NV, NJ, OH, OR, PA, SC, TN, UT, VA, and WA |

What Product Does Splitero Offer?

Splitero offers a single product: the home equity investment (HEI). It lets homeowners access their equity without a loan or monthly payments.

Instead of interest, Splitero’s funds managed by institutional investors, including Blue Owl Capital, take a share of your home’s future appreciation.

How Does Splitero Work?

Splitero provides a lump sum of cash in exchange for a share of the home’s future value, allowing you to unlock funds without creating new debt or making monthly payments.

Eligibility and Property Requirements

To qualify, your property must be owner-occupied and can be a single-family home, condo, or a 2 to 4-unit residence valued between $200,000 and $5 million. Homes may be held by an individual, trust, or LLC (with approval).

There are no income or employment requirements, and the minimum credit score to apply is 500. Applicants submit ID, basic mortgage documents, and lien information.

Splitero may record its lien in a first or junior position depending on your existing loan, and it conducts a hard credit inquiry valid for 120 days.

Ineligible properties include non-owner-occupied units, manufactured or modular homes, commercial or agricultural buildings, and unique structures like container homes or log cabins.

Funding Amounts

Eligible homeowners may receive between $50,000 and $500,000, up to 25% of their home’s value, depending on location and market value.

Since Splitero’s HEI is not a loan, there’s no interest or additional monthly payments. The company earns a return only when the property sells, is refinanced, or when you repurchase the investment.

Application Process

The process is designed to be fast and digital:

- Pre-qualify: Enter your property address to get an estimate of how much you could receive.

- Apply: Submit details about ownership, income, and financial goals.

- Appraisal & Offer: Splitero orders a third-party valuation and sends your offer.

- Funding: Once you sign, the funds are typically disbursed within two to four weeks.

You can repurchase your investment at any time through selling, refinancing, or paying it off directly.

Read More: Home Equity Line of Credit: What It Is and How It Works

How Much Does a Splitero HEI Cost?

Splitero charges a 4.99% origination fee, deducted from your funds, plus third-party fees (appraisal, title, escrow, and recording) that average about $1,000.

The company’s return is capped at 17.99% annually on its share of your home’s future value. You’ll never owe interest or additional monthly payments, and there are no penalties for early repurchase.

How Does Splitero Calculate the Savings Compared to Credit Cards and Other HEI Providers?

Splitero estimates that homeowners could save $32,085 over five years compared to carrying the same balance on a credit card charging 26.89% APR, which reflects the national average for fair credit borrowers in August 2024.

Compared with other home equity partner programs, projected savings can reach $19,590 over a 10-year period, assuming a $1 million starting home value and a $100,000 investment.

This comparison is based on a 3% annual appreciation rate.

However, final savings will vary by applicant due to differences in minimum credit score, occupancy status, valuation, and pricing factors.

Note: Splitero’s comparison of the calculation with that of credit cards reflects WalletHub’s 2024 data. WalletHub has now updated its APR average for fair credit borrowers to 26.79% for April 2026.

Benefits of Getting a Splitero Home Equity Investment

Since Splitero provides access to home equity funds without the structure of traditional loans, you can have the following benefits:

- No monthly payments: You repay only when you sell, refinance, or through cash settlement.

- Fast lump-sum access: Receive up to 25% of your home’s value without income requirements or long bank approvals.

- Flexible buyout: You can repurchase anytime with no penalty.

- Low credit threshold: The minimum credit score of 500 allows more families and employees with limited credit to qualify.

- Full ownership retained: The owner keeps the title; Splitero simply records a lien.

- Unchanged mortgage: No impact on your rate or term, letting you continue living in your home.

Risks and Limitations of Splitero Home Equity Investment

Splitero may not be feasible for many homeowners.

From repayment structure to state availability, some restrictions may affect long-term decisions or eligibility.

- Single repayment: The balance must be paid in full at sale, refinance, or cash settlement; there’s no installment option.

- No early discount: Paying early doesn’t reduce what you owe on the agreed appreciation.

- Fees: Origination and third-party fees reduce your net payout.

- State availability: Currently limited to 14 states, though Splitero plans to expand.

- Appraisal concerns: Some customers mention valuation differences during buyouts; review the terms carefully.

Splitero Reviews

Public feedback on Splitero reflects a mix of positive experiences and critiques.

While some users report satisfaction with the entire process, others raise concerns about transparency and cost.

Here are the company reviews from the following third-party platforms.

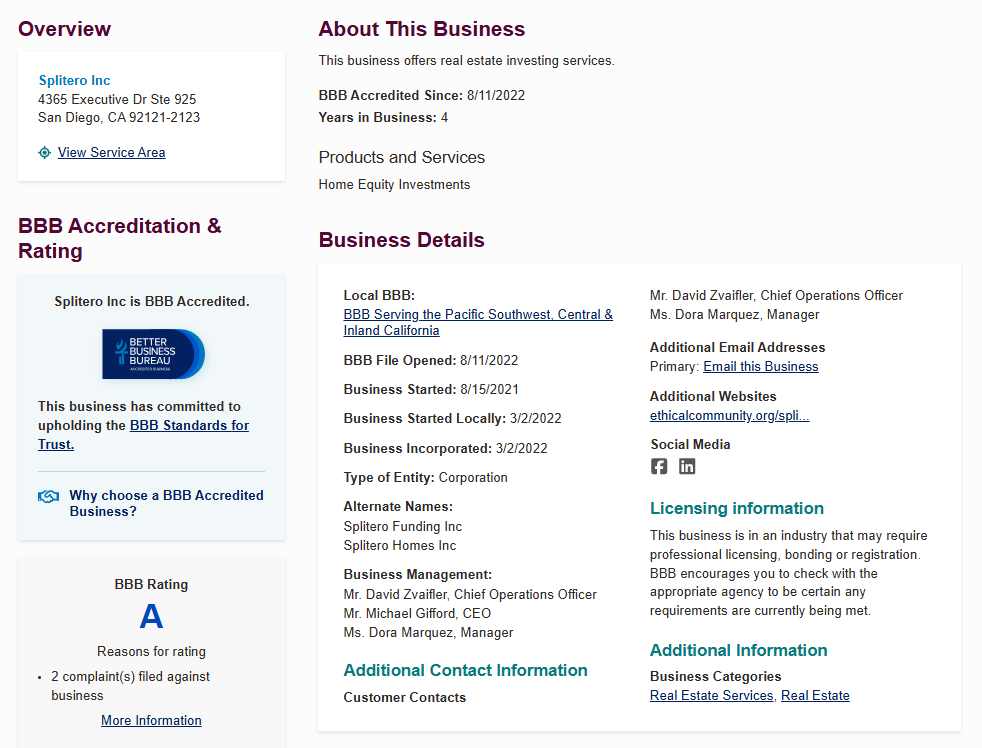

Better Business Bureau (BBB) Reviews

Splitero has been BBB-accredited since August 2022 and currently holds an A rating with an average of 4.07 stars from 28 reviews.

Most positive reviewers highlight a fast, professional process with no surprises and responsive support staff.

Negative reviews cite misleading pre-qualifications, late property denials after months, and hard credit pulls causing damage.

BBB complaints involve unsolicited marketing mail sent to opted-out homeowners.

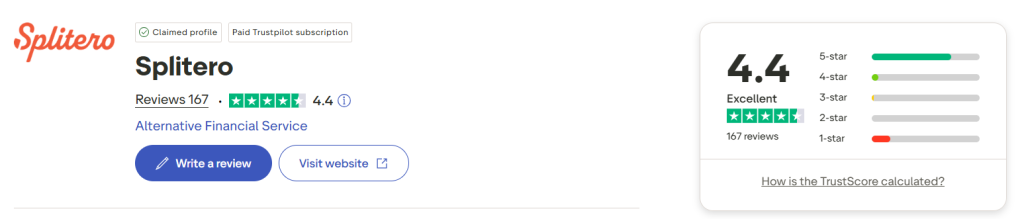

Trustpilot Reviews

As of April 2026, Splitero has a 4.4 TrustScore on Trustpilot from more than 100 reviews.

Most positive reviewers praise the professional staff, smooth application process, and fast funding within weeks.

Negative reviews highlight communication issues, repeated document requests, and concerns about high repayment costs.

Reddit Reviews

is a home equity investment (hei) from point.com better than a home equity line of credit (heloc)? what are the disadvantages of a hei?

by

u/ConfidentCategory771 in

Mortgages

No Reddit posts directly discuss Splitero, but a few comments across two threads mention it briefly. One commenter found Splitero fair and straightforward after researching home equity investment options available.

Home Equity investment – bad idea?

by

u/subietrek in

RealEstate

Splitero’s $50,000 minimum was also flagged as too high for a commenter who needed a smaller amount.

When to Use Splitero

Splitero may be ideal for homeowners who:

- Want cash without a loan or additional monthly payments.

- Need to pay off debt or consolidate high-interest balances.

- Wish to fund home improvements or pursue financial goals like retirement.

- Prefer better options to access their equity without income requirements.

- Are house-rich but cash-poor and want to continue living in their homes.

When to Avoid Splitero

Avoid Splitero if you:

- Need funds for only a short term, since HEIs work best over several years.

- Prefer predictable monthly payments from a traditional loan.

- Expect your home’s future value to rise significantly and don’t want to share it.

- Live outside the eligible states or require under $50,000.

Is Splitero Legit?

Available third-party data supports Splitero’s credibility. The company holds an A rating with the BBB and has been accredited since 2022.

Blue Owl, an institutional investor, has also committed $350 million to Splitero. However, customer experiences may still vary.

How Splitero Compares to Other Options

| Feature | Splitero | HELOC | Home Equity Loan | Credit Cards |

|---|---|---|---|---|

| Type | Home equity investment | Revolving credit line | Lump-sum loan | Unsecured revolving credit |

| Monthly Payments | No | Yes (variable) | Yes (fixed) | Yes (variable, often high) |

| Repayment | Sale, refinance, or cash settlement | Monthly | Monthly | Minimum monthly |

| Rate / Return Cap | 17.99% annual compounded | Variable APR | Fixed APR | 20%–27% APR |

| Min. Credit Score | 500+ | 620+ | 620+ | Typically 580–670+ |

| Income Required | No | Yes | Yes | Yes |

| Equity Required | 30% retained | 15–20% | 15–20% | N/A |

| Availability | 14 states | Nationwide | Nationwide | Nationwide |

Splitero vs. Other HEI Providers

| Company | Funding | Term Length | Min. Credit Score |

|---|---|---|---|

| Splitero | $50K–$500K | Up to 30 years | 500 |

| Hometap | $15K–$600K | 10 years | 585 |

| Unlock | $15K–$500K | 10 years | 500 |

| Point | $30K–$500K | 30 years | 500 |

You May Also Like:

Subletting vs Subleasing: Understanding the Key Differences

Are Utilities Included in Rent? Costs, Benefits, and Tenant Rights

Assessed Value: Meaning, How to Calculate, Importance & More

Short Sale vs Foreclosure: Timeline, Pros & Cons, and Key Differences

Pros and Cons of Airbnb for Landlords and Renters