Total household debt climbed by $191 billion to $18.8 trillion in Q4 2025, according to the latest Quarterly Report on Household Debt and Credit. Balances are rising across credit cards, medical bills, and personal loans, and more Americans are turning to debt relief companies for a way forward.

Freedom Debt Relief is among the more widely recognized debt settlement companies in the country. Before enrolling, here’s what the program costs, how it works, and what it does to your credit.

What Is Freedom Debt Relief?

Freedom Debt Relief is a debt settlement company, not a lender. Founded in 2002 and headquartered in San Mateo, California, FDR operates as an LLC and has been in business for over 23 years.

To date, the company has served more than one million clients and resolved over $20 billion in enrolled debt, making it one of the largest debt relief program providers in the country.

Freedom Debt Relief at a Glance

| Company type | Debt settlement company |

| Free quote or consultation | Available at no cost |

| Services | Debt settlement, credit counseling, debt consolidation, bankruptcy evaluation |

| Min. required debt | $7,500 in unsecured debt |

| Average turnaround | 24 to 48 months |

| Settlement fee | Up to 20% of total enrolled debt |

| Fee range | 15% to 25% of enrolled debt |

| Additional fees | $9.95 monthly maintenance fee |

| Eligible debt types | Credit cards, personal loans, medical bills, collections, private student loans, select business debts |

| Accreditations | American Association for Debt Resolution |

| Negotiation approach | Direct or third-party, varies by state |

How Freedom Debt Relief Works

- The process begins with a free consultation. You share your total debt and basic financial details, and FDR reviews your situation before moving forward.

- After enrollment, you open an FDIC-insured dedicated account and deposit a fixed amount each month.

- FDR recommends pausing payments to creditors during this period, which is standard in the debt settlement process.

- Once enough funds accumulate, FDR’s negotiation team reaches out to creditors with reduced settlement amount offers, targeting each account for less than the original debt.

- Every time a creditor accepts an offer, it shows up in your online dashboard. You review and approve the settlement agreement before any payment goes through.

- FDR collects its service fees only after you approve a settlement.

- When all enrolled debt is resolved, your settled accounts close at the negotiated amounts, and you exit the program.

Freedom Debt Relief Fees and Costs

FDR charges a service fee rate of 15% to 20% of enrolled debt, but only after a settlement agreement is finalized. No fees are collected before a creditor settles.

In addition to the settlement fee, there’s a one-time $9.99 setup fee and a $9.95 monthly account management fee.

Key Features That Differentiate Freedom Debt Relief

FDR has three program features that most debt settlement companies don’t offer.

Refund Guarantee

FDR refunds the difference if total service fees collected exceed the original debt enrolled, up to 100%. Enroll $30,000 and pay more than that in combined costs, and you get money back.

Legal Support Network

Some creditors pursue lawsuits once monthly payments stop. FDR’s legal partners network gives enrolled clients access to legal support at no added cost, covering a gap that most debt settlement services leave to the borrower.

Acceleration Loan Options

Through Achieve, FDR’s parent company, eligible clients can access personal loans to fund negotiated settlements faster. Qualifications vary, but it lets clients exit the debt settlement program sooner.

Freedom Debt Relief Requirements

To qualify for the Freedom Debt Relief program, you need at least $7,500 in unsecured debt and a documented financial hardship, such as job loss, reduced income, divorce, a death in the family, or medical issues. You also need to live in a state where FDR operates.

Pros and Cons of Freedom Debt Relief

FDR offers some advantages that other settlement companies don’t, but there are limitations to know before enrolling.

Pros

- FDR has a large, experienced negotiation team that handles the settlement process on your behalf.

- Proprietary technology helps determine which accounts to prioritize, which can speed up first settlement offers.

- Refund policy covers cases where total service fees exceed the original debt enrolled.

- Online dashboard gives clients full visibility into their account status and approved settlements.

Cons

- Enrolling in the debt settlement program will negatively affect your credit report while the program is active.

- FDR cannot settle tax debts, federal student loans, or secured debts such as mortgages and auto loans.

Freedom Debt Relief Reviews and Reputation

Here’s what clients, review platforms, and online forums say about Freedom Debt Relief.

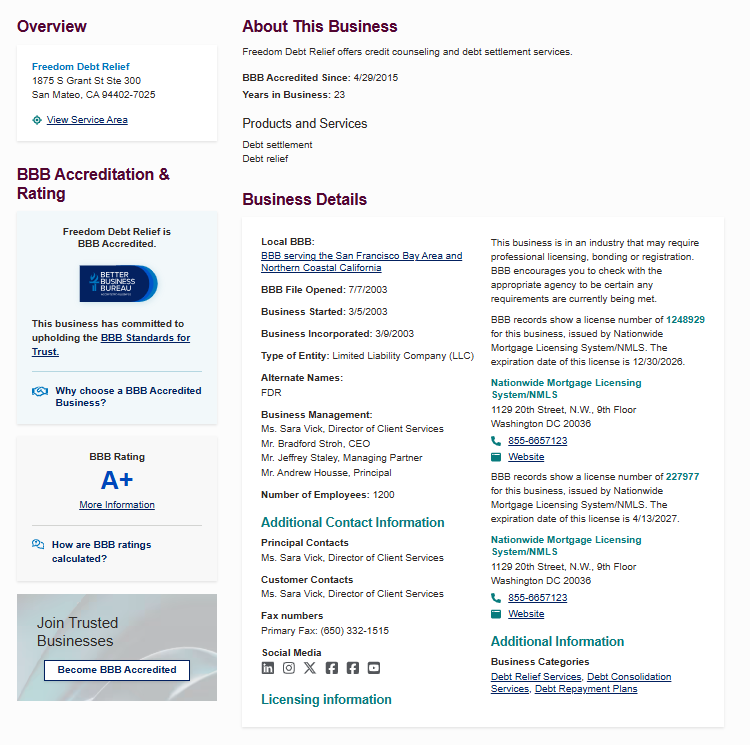

Better Business Bureau (BBB) Reviews

FDR holds an A+ BBB rating and has maintained accreditation since 2015. Across 1,582 customer satisfaction reviews, the company averages 4.41 stars.

Positive feedback highlights fast first settlement offers and responsive support throughout the settlement process.

Negative reviews cite fee transparency issues and slower-than-expected progress on total debt balances. BBB records show 288 complaints over three years, with billing and service issues topping the list.

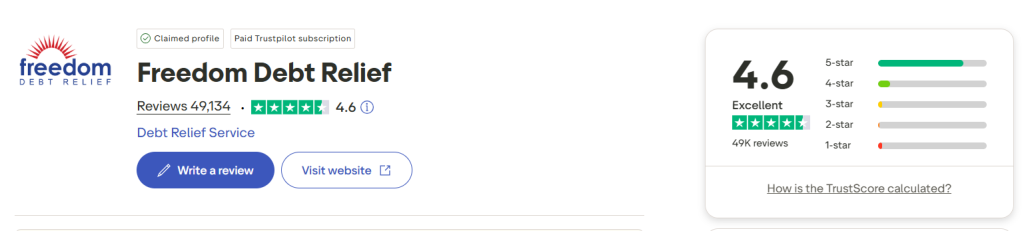

Trustpilot Reviews

FDR holds a 4.6 Trustpilot rating across over 49,000 reviews. Positive feedback highlights professional staff and smooth communication throughout the debt settlement process.

Many clients report receiving a first settlement offer faster than they expected after enrolling. Recurring complaints mention debt collectors continuing to reach out while the Freedom Debt Relief program is active.

Some reviewers also noted the program timeline ran longer than what was presented at enrollment.

Reddit Reviews

Most Reddit users confirm FDR is a legitimate company that handles unsecured debt through negotiated settlements. Several shared firsthand accounts of settling balances for roughly 40% to 55% of their original debt.

Is freedom debt relief legit? I’m exploring options…

by

u/Conscient- in

shoppingaddiction

Consistent deposits into a dedicated account were cited as the main factor in completing the program. Users are warned that missed payments damage their credit report, and debt collectors may still call during the process.

Any forgiven debt can be considered taxable income, which caught some enrollees off guard at the end.

Freedom Debt Relief vs. Competitors

| Possible Savings | Min. Balance | Settlement Fee | Monthly Account Fee | State Availability | Refund Guarantee | Consolidation Loan Option | |

|---|---|---|---|---|---|---|---|

| Freedom Debt Relief | Up to 50% | $7,500 | 15% – 25% | $9.95 | More states, incl. via legal partners | Yes | No |

| National Debt Relief | Up to 50% | $10,000 | 15% – 25% | None listed | 45 states | No | No |

| Accredited Debt Relief | Up to 50% | $10,000 | 25% | None | 30 states + D.C. | No | Yes, via Beyond Finance |

Alternatives to Freedom Debt Relief

FDR works for specific situations, but it’s not the only path out of debt.

Debt Management Plans

Nonprofit credit counseling agencies offer debt management plans that let you repay the full debt on a structured schedule.

Monthly fees run $25 to $50, and programs take 3 to 5 years. The credit impact is minimal, which makes it worth considering for borrowers still making minimum payments.

Personal Loan Consolidation

A consolidation loan combines multiple balances into one fixed monthly payment at a lower interest rate. You need a 600+ credit score to qualify, and repayment spans 2 to 7 years.

DIY Debt Settlement

Borrowers with few accounts can negotiate a reduced settlement amount with creditors directly and avoid service fees entirely. The credit impact mirrors professional settlement, but results depend on the creditor.

Bankruptcy Options

Chapter 7 eliminates most unsecured debts in 3 to 6 months. The credit impact lasts 10 years, and filing costs apply. For borrowers with no viable repayment path, speaking with a bankruptcy attorney before enrolling in any debt relief program is a reasonable first step.

Read More: Can Debt Consolidation Affect Your Credit Score?

Who Should Use Freedom Debt Relief?

Before reaching out to FDR, it’s worth checking whether your situation lines up with the program.

Who It’s Best For

- Borrowers already falling behind on monthly payments with $7,500 or more in unsecured debt

- People dealing with credit card debt, medical debt, or other unsecured debts who can commit to consistent deposits into a dedicated account

- Residents in states where FDR operates

- Borrowers facing potential creditor lawsuits who need access to legal partners at no added cost

Who Should Avoid It

- Borrowers with secured debts, federal student loans, or tax debt, as FDR does not cover these

- Those with a 600+ credit score and manageable balances who may qualify for a consolidation loan with less credit impact

- Residents in states where FDR does not operate

- Anyone still able to make minimum payments without significant strain, who should consider nonprofit credit counseling or a debt management plan first

Is Freedom Debt Relief Legit and Safe?

FDR is a legitimate company with over 23 years in business, an A+ BBB rating, and $20 billion in enrolled debt resolved. Per FTC rules, no service fees are collected until a settlement agreement is reached, and clients retain control of their dedicated account throughout.

The credit impact from missed payments and the tax liability on forgiven debt are standard risks across all debt settlement services.