The average credit card balance in the U.S. grew to $1.23 trillion in 2025. Student loan balances also climbed as of February 2026, now totaling $1.833 trillion.

Meanwhile, total household debt jumped in the fourth quarter of 2025, hitting $18.8 trillion.

People are still borrowing, but many are also hitting a wall with repayment. For many, the repayment wall could lead to searches like Accredited Debt Relief reviews.

So, this review focuses on what the experience looks like beyond the quote and how well Accredited Debt Relief aligns with expectations.

What Is Accredited Debt Relief?

Accredited Debt Relief started in 2011 and is based in San Diego. It’s part of Beyond Finance, LLC.

The company works with people dealing with unsecured debt who may not get approved for a traditional consolidation loan or need help working out lower payments with creditors.

Accredited Debt Relief Details: Fees, Terms, Requirements, Availability

| Category | Details |

|---|---|

| Service offered | Debt consolidation as listed on site |

| Min enrolled debt | About $1k-$100k |

| Program length | 24-48 months |

| APR | 4.9% to 35.99% |

| Fees | Success-based, about 25% of enrolled debt, varies by state |

| Eligible debts | Most unsecured debts: credit cards, medical, personal loans, private student loans |

| Availability | Not offered in all states |

| Credit impact | Short-term credit drop due to paused payments – risk of collections or lawsuits |

What Products Does Accredited Debt Relief Offer?

Accredited Debt Relief offers debt consolidation services through its affiliate network.

While the company itself does not issue debt consolidation loans, it connects clients with lenders that do.

Who Qualifies for Accredited Debt Relief?

You’ll need at least $1,000 in unsecured debt to qualify, with the program capping at around $100,000. It also depends on where you live.

Most people who apply are already behind on payments or close to it. You’ll also need to show you can make consistent monthly deposits into a separate account.

What Fees Does Accredited Debt Relief Charge?

Accredited Debt Relief doesn’t bill you at the start. You only pay if they’re able to negotiate a debt. The fee can go up to 25% of the amount enrolled.

There may also be a separate charge from the third-party company that manages your escrow account during the program.

How to Enroll in Accredited Debt Relief

- Start by getting a free quote online or call 800-497-1965.

- Go over your budget and debt with a specialist.

- Get matched with a program based on your financial situation.

- Begin making monthly payments into a separate account.

- Some clients finish the program in 24 to 48 months.

Benefits of Accredited Debt Relief

Accredited Debt Relief gives people room to look at their options without pressure.

Free Consultation

The consultation is free. It lets you ask questions and review your financial situation without committing to anything.

Flexible Debt Relief Solutions

If debt consolidation isn’t a fit, the company can refer you to a lender that offers other debt relief options instead. This gives more room to adjust based on your income or the type of debt you need to manage.

Risks of Accredited Debt Relief

The program can help reduce debt, but there are risks that depend on your creditors, location, and financial situation.

Credit Score Impact

Your credit score may drop during the process, since accounts usually go unpaid while negotiations happen.

Not All Creditors Settle

Some lenders don’t accept debt settlements. This can lead to delays or further collection activity.

Collection Calls & Legal Risk

While you’re saving up funds, you may still get calls from debt collectors. In some cases, lawsuits are also a possibility.

Limited State Availability

Accredited Debt Relief doesn’t operate in every state, so eligibility depends on where you live.

Possible Tax Implications

If any portion of your debt is forgiven, it may count as taxable income, depending on the amount and how the IRS treats it.

Read More: Can Debt Consolidation Affect Your Credit Score?

Accredited Debt Relief Reviews

People have shared varying Accredited Debt Relief reviews across the following platforms:

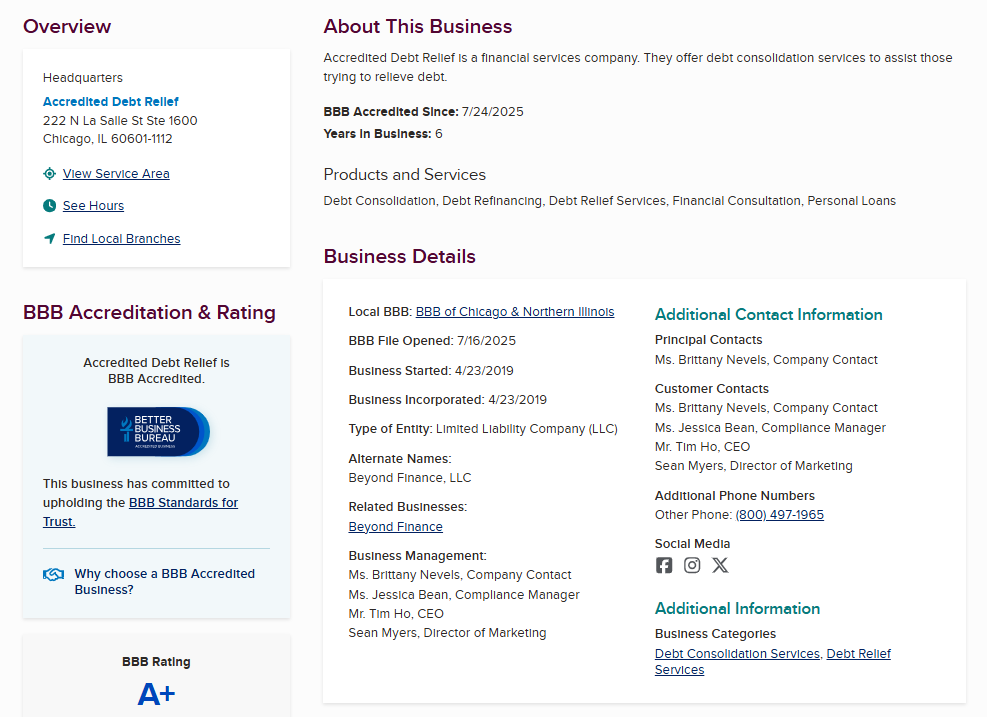

Better Business Bureau (BBB) Reviews

Accredited has a 4.9-star average from more than 3,000 reviews on its BBB profile. It’s also accredited and has an A+ rating.

Customers say the staff is respectful, calm under pressure, and willing to walk them through difficult financial decisions.

On the downside, there are complaints about delays, especially around refunds when accounts were canceled or when creditors refused to negotiate.

A few ran into issues with billing errors tied to third-party escrow accounts or heard from debt collectors even after enrolling.

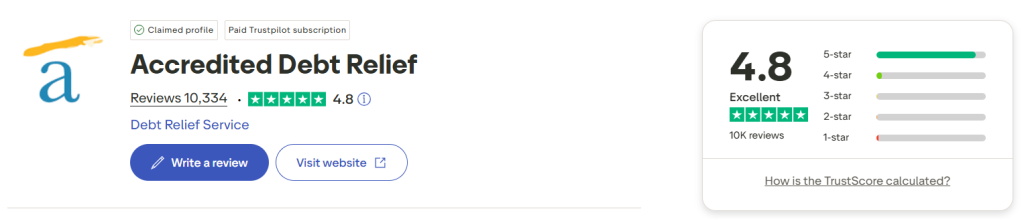

Trustpilot Reviews

More than 10,000 people have left feedback on Trustpilot.

Some reviews mention that they were able to lower their monthly payments, and a few said they finally saw a way out after struggling with debt for years.

There are also complaints about transparency regarding the credit impact and the overall cost of the program compared to self-negotiation.

Reddit Reviews

Anyone here actually used Accredited Debt Relief? Reviews seem too polished

by

u/R3LOGICS in

DebtAdvice

Reddit users tend to be more blunt. Most users confirm that your credit score will drop once you stop making payments, which is part of how this debt relief works.

A few said they received collection calls or legal notices while still building funds, which added more pressure.

Any reviews from people who have used accredited debt relief?

by

u/RogueAndor1 in

CRedit

Several people advised comparing the program to options like credit counseling, debt management plans, or even bankruptcy before signing anything.

When to Use Accredited Debt Relief

For some consumers, it fits a specific type of situation where the balance, timeline, and risk all line up.

You Have $10,000+ in Unsecured Debt

It works best if you owe more than $10,000 in credit card debt, medical bills, or other unsecured accounts.

You Prefer a Hands-Off Negotiation

If you’d rather not negotiate with creditors directly, the company takes care of that.

You Accept Short-Term Credit Impact

Getting debt-free through settlement means your score may drop. This could make sense if your goal is to reduce what you owe and eventually recover over time.

When to Avoid Accredited Debt Relief

Depending on your options and location, other routes may be safer or more effective.

You Qualify for Traditional Consolidation or a Nonprofit DMP

If you can get approved for a lower-interest consolidation loan or qualify for a nonprofit debt management plan, those may reduce your cost with fewer downsides.

You Can’t Handle Collections or Lawsuits

The settlement process can trigger phone calls from creditors or even lawsuits while you build up your account. If that would create more stress or risk, this route may not work for you.

You Live in a Restricted State

Accredited Debt Relief doesn’t operate in every state. If your state isn’t covered, the program won’t be an option.

Is Accredited Debt Relief Legit?

Yes, Accredited Debt Relief is a real service. How well it works comes down to what you owe, how much you can set aside, and whether you’re able to stick with the program through to the end.

Comparing Accredited Debt Relief to Other Debt Relief Providers

| Company | Requirements / Fees | Eligible / Ineligible Debts | Locations | Programs / Details |

|---|---|---|---|---|

| Accredited Debt Relief | Works with about $1k-$100k. Success fee around 25% and can vary by state. Site lists 4.9%-35.99% APR. | Eligible: most unsecured debts like credit cards, medical bills, personal loans, private student loans. Ineligible: secured debts and some government debts. | Not in every state | Debt consolidation. Typical timeline 24-48 months. Credit can dip while payments pause and collectors may call or sue. |

| JG Wentworth | Minimum $10k. Fees run 18%-25%. One-time setup fee of $9.95; monthly escrow fee of $9.95; legal representation at $17.99 monthly. | Eligible: most unsecured debts. Ineligible: secured debts. | Varies by state | Debt settlement. Plans often last 24-60 months. Expect a likely credit hit. |

| Credit Associates | Minimum $7,500. Fee is about 25% of enrolled debt. | Eligible: unsecured debts like cards, medical, personal loans, collections, some private student loans. Ineligible: secured debts, government debts, court judgments. | Not in all states | Debt settlement. About 24-36 months. Money goes into a dedicated account. Credit may drop during the process. |

| National Debt Relief | Minimum $7,500. $9 setup and $9.85 monthly. Settlement fee up to 25%. | Eligible: most unsecured debts including cards, loans, payday, medical, collections, some business and private student loans. Ineligible: mortgages, auto, child support, taxes, federal student loans. | 47 states except OR, VT, WV plus DC, PR, Guam, USVI | Debt settlement program. |

| Pacific Debt Relief | Minimum $10k. Fee around 15-25%. | Eligible: unsecured debts Ineligible: secured debts. | All states except Oregon | Debt settlement with a free consult. Usually 2-4 years. IAPDA accredited. |

| Money Management International (MMI) | No minimum. Setup $33-$75. Monthly $25-$59. | Eligible: helps manage unsecured debts through payment plans, not settlement. | Nationwide | Nonprofit credit counseling and DMPs. Often cuts interest by about 20% or more. |