Latest Equifax data shows that the rate of increase for overall consumer debt grew faster in December 2025 than in the same month in 2023 and 2024, with total U.S. consumer debt reaching $18.20 trillion by the end of 2025.

As more consumers look for ways to manage their debt load, many are turning to debt relief companies and searching for information like Credit Associates reviews.

So, is Credit Associates worth trusting with your debt?

What Is Credit Associates?

Credit Associates is a debt settlement company based in Dallas, Texas. It doesn’t offer debt consolidation.

Unlike lenders, Credit Associates does not handle secured debts like mortgages or auto loans.

This company is not a lender; it works through negotiation and settlement of unsecured debts.

Credit Associates Debt Relief Fees, Terms, Requirements, Availability

| Category | Details |

|---|---|

| Minimum enrolled debt | Not stated on its website; third-party sources say $7,500 or $10,000. |

| Program length | 24–48 months |

| Fees | 25% of enrolled debt |

| Debt types covered | Unsecured debts such as credit cards, medical bills, personal loans, collection accounts, some private student loans |

| Excluded debts | Secured debts (e.g., auto loans, mortgages), government loans, court-judgment debts |

| Impact on credit | Enrollment typically harms your credit score, because you stop making payments while funds accumulate |

| Account setup / funds holding | Clients deposit monthly payments into a dedicated “special purpose” or savings account used for settlement |

| State / availability constraints | Not every state is serviced; some state restrictions apply |

What Products Does Credit Associates Offer?

Credit Associates offers debt settlement. The goal of this service is debt resolution through negotiation.

Instead of having clients continue to make minimum payments, Credit Associates seeks to settle each enrolled debt for less than the full balance.

Who Qualifies for Credit Associates Debt Relief?

To qualify:

- Clients may need at least $7,500 or $10,000 in unsecured debts, including credit card debt, medical bills, or personal loans.

- Applicants must show financial hardship, such as late or missed monthly payments.

- Service is limited to U.S. residents in states where Credit Associates is active.

- Enrollees are required to make monthly deposits into a special-purpose savings account.

What Fees Does Credit Associates Charge?

Credit Associates charges a 25% fee based on the amount of debt you enroll.

There may also be small administrative costs where your payments are held during the program.

These details aren’t always fully explained upfront, so it’s worth asking about them during the free consultation before you sign anything.

How to Enroll in Credit Associates Debt Relief

Credit Associates’ process involves the following steps:

- Schedule a free consultation.

- Review and sign the service agreement.

- Start monthly deposits into the savings account.

- Credit Associates negotiates with creditors.

- Approve or reject each settlement offer.

Benefits of Credit Associates

Some of the most notable benefits of Credit Associates include:

Accredited / Industry Memberships

Credit Associates is accredited by the following organizations:

- International Association of Professional Debt Arbitrators (IAPDA)

- Association for Consumer Debt Relief (ACDR)

- Dun & Bradstreet Credibility Corp

- BSI Financial Services

While these memberships don’t guarantee performance, they indicate the company’s commitment to industry standards on fees, compliance, and disclosure.

No Upfront Fees

Clients don’t pay anything at enrollment. The company only charges after each debt is settled.

Potential Debt Reduction

If settlements are successful and clients complete the program, there’s potential to lower the total amount owed on credit card debt, medical bills, and personal loans.

Risks & Limitations of Credit Associates

Clients considering enrollment should understand these risks before proceeding.

Credit Score Damage

The program requires you to stop paying creditors, which leads to missed payments, delinquencies, and possibly charge-offs.

These are reported to credit bureaus and can lower your credit score, sometimes for years.

Collection Calls, Lawsuits & Legal Risk

Enrollment doesn’t prevent legal action or eliminate communication from collectors.

While enrolled, creditors can continue calling, send letters, or pursue lawsuits. Some Credit Associates reviews mention being sued while still active in the program.

Uncertainty / No Guarantee of Success

Not every account will be settled. Some creditors refuse to negotiate, which can leave balances unresolved.

Clients might not achieve full debt resolution or expected savings, even if the program is completed.

Limited Service Scope & Lack of Transparency

Credit Associates does not offer debt consolidation, credit counseling, or other options. The company only provides settlement.

Some reports also claim the company doesn’t explain its settlement fees or expected outcomes clearly during the free consultation.

State Restrictions & Eligibility

Not all states allow debt relief services. Service is unavailable in some areas due to debt settlement laws. Clients must confirm eligibility based on their location before enrolling.

Credit Associates Reviews

While some Credit Associates reviews report positive outcomes, others share concerns around communication, transparency, and service consistency.

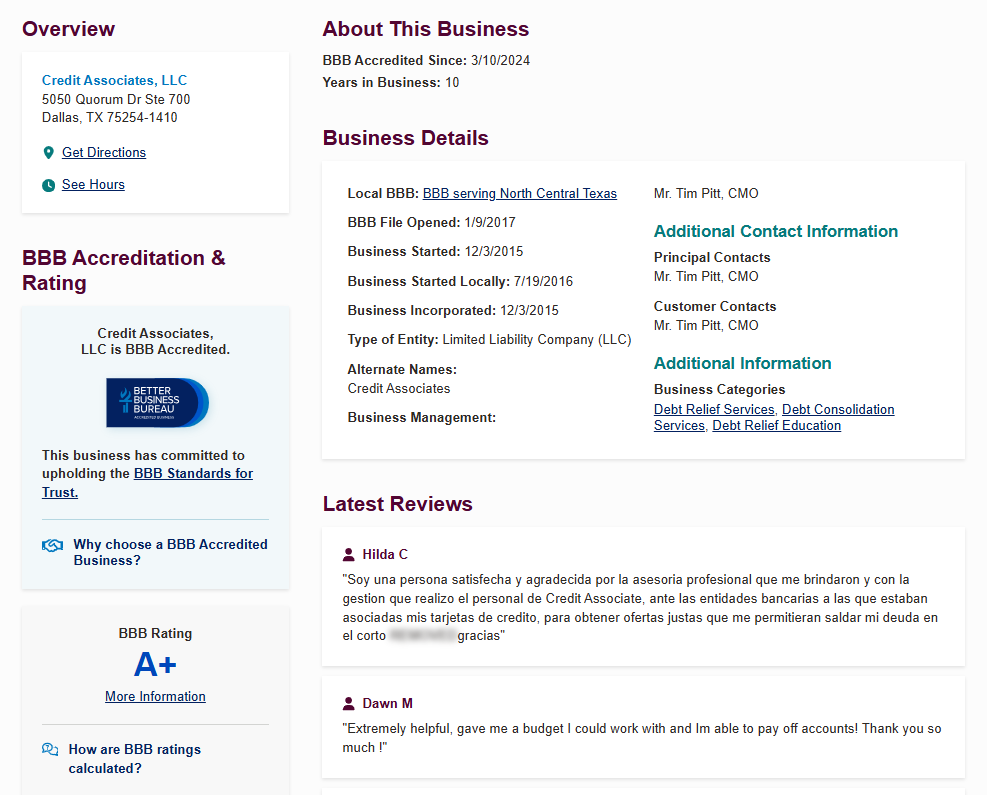

Better Business Bureau (BBB) Reviews

Credit Associates is accredited by the BBB and holds an A+ rating.

The company has a 4.21 rating based on over 300 customer reviews, with positive feedback centered on helpful representatives and successful debt settlements.

However, the company has received 119 complaints over the last three years, with the most common issues involving clients being sued by creditors while still enrolled, fee misrepresentation, and poor communication.

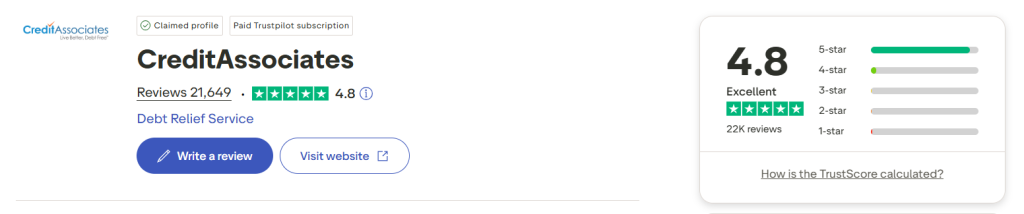

Trustpilot Reviews

Credit Associates has a 4.8 rating on Trustpilot, based on more than 21,000 reviews.

Most reviewers praise the staff for being knowledgeable, patient, and clear in explaining the program.

A small number of reviewers raised concerns about payment issues and fees offsetting their overall savings.

Reddit Reviews

Reddit isn’t enthusiastic about debt settlement. The general tone is skeptical. Users share concerns about credit score damage, poor communication, and the chance of getting sued while still in the program.

Some say they saw results. A few debts were settled. But even in those cases, progress felt slow and updates were inconsistent.

CreditAssociates and other ‘debt relief’ companies – a warning from a dupe.

by

u/ham-ham-iam in

personalfinance

In comparison, users tend to recommend other routes: nonprofit credit counseling, direct negotiations, or bankruptcy. These are viewed as more transparent and easier to control.

One theme comes up repeatedly: aggressive sales tactics. Some felt pushed to enroll quickly after the free consultation. Others were frustrated when creditors refused to negotiate at all.

When to Use Credit Associates

Below are situations where using Credit Associates could make sense.

You Have High Unmanageable Debt

If you owe $10,000 or more in unsecured debts and cannot manage the balances through minimum payments, refinancing, or consolidation, settlement could be a last-option path.

You Accept Temporary Credit Damage

Using a debt settlement program will almost always cause a drop in your credit score, especially in the early stages.

If you’re willing to trade credit impact for the possibility of debt resolution, this approach may be worth considering.

You Prefer Negotiation

If you don’t feel comfortable negotiating directly with creditors or don’t have the time or emotional bandwidth to manage it, then letting a firm like Credit Associates handle that process may appeal to you.

When to Avoid Credit Associates

Credit Associates isn’t the right choice for everyone. Some people may have safer, more predictable options depending on their financial situation and how much risk they’re willing to take on.

You Qualify for Nonprofit DMP or Loan Consolidation

If you can get into a nonprofit debt management plan or qualify for a lower-interest loan, those might be better options.

These programs usually let you stay current on your accounts, avoid credit score damage, and get out of debt with less uncertainty.

You Can’t Tolerate Risk

If you’re not prepared for collection calls, late fees, or the risk of being sued, it may not be something you want to take on.

You’re in an Unsupported State

Some states either ban or limit how debt settlement companies can work. If you live somewhere that restricts these services, you won’t be able to enroll.

You Need Transparency & Certainty

Some Credit Associates reviews say it’s hard to get clear answers at the beginning. If that kind of uncertainty is a dealbreaker, it’s something to keep in mind.

Is Credit Associates Legit?

Yes, Credit Associates operates as a legitimate debt settlement company, with confirmed business records, industry memberships, and third-party verification.

How Credit Associates Compares to Other Debt Settlement Companies

| Company | Requirements / Fees | Eligible / Ineligible Debts |

|---|---|---|

| Credit Associates |

| Eligible: Unsecured (credit cards, medical bills, personal loans, collections, some private student loans) Ineligible: Secured (mortgages, auto), government loans, court-judgment debts |

| JG Wentworth |

| Eligible: Most unsecured (credit cards, medical, personal loans, some private student loans) Ineligible: Secured (mortgages, auto) |

| Pacific Debt Relief |

| Eligible: Unsecured (credit cards, medical) Ineligible: Secured (mortgages, auto) |

| Money Management International (MMI) |

| Eligible: Focused on unsecured via management, not settlement |

| National Debt Relief |

| Eligible: Most unsecured (credit cards, loans, payday, medical, collections, some business & private student loans) Ineligible: Mortgages, auto, child support, taxes, federal student loans |