U.S. consumer debt hit $18.57 trillion as of September 2025, according to Experian. Meanwhile, the Federal Reserve Bank of New York put household debt at $18.8 trillion.

As balances grow, so does the pressure to keep up with payments.

Plenty of people are looking into debt settlement or debt consolidation as one possible way to manage that strain. Searches for terms like Turbo Debt reviews suggest many want to weigh their options before taking the next step.

What Is Turbo Debt?

Turbo Debt is a debt settlement company based in Sunrise, Florida. It operates across several states and U.S. territories.

Turbo Debt Debt Relief Details

| Category | Details |

|---|---|

| Minimum Debt | Around $10,000 in unsecured debt required to enroll |

| Program Duration | 24-48 months |

| Fees | About 25% of enrolled debt, charged after settlement |

| Eligible Debts | Credit cards, medical bills, personal and business loans, veteran or divorce-related debts |

| Availability | Not available in Connecticut, Minnesota, Oregon, Vermont, West Virginia, and Wisconsin |

| Credit Impact | Credit score may drop temporarily as payments are paused during savings buildup |

What Services Does Turbo Debt Offer?

Turbo Debt markets itself as a debt relief company, but its primary service is debt settlement. It focuses on helping clients negotiate unsecured debts through customized settlement plans.

Who Qualifies for Turbo Debt Debt Relief?

To qualify, you need at least $10,000 in unsecured debt and a financial situation that makes it hard to keep up with monthly payments. You also need to live in a state or territory where Turbo Debt operates.

Turbo Debt works with several types of unsecured debt, including credit card debt, personal loans, medical debt, divorce-related debt, retirement debt, student loans, and business debt.

The following types of debt are generally not eligible:

- Auto loans

- Debts from lawsuits or court judgments

- Government-backed loans

- IRS debt

- Mortgages or home equity loans

- Utility bills

- Any debt secured by collateral

What Fees Does Turbo Debt Charge?

Turbo Debt doesn’t charge upfront fees. You only pay after a debt has been successfully settled. The service fee can go as high as 25% of the enrolled debt.

Keep in mind, fees are based on the amount enrolled. Not on how much debt is forgiven or how much you save.

How to Enroll in Turbo Debt Debt Relief

It starts with a quick questionnaire about your financial situation, just a few questions that take a couple of minutes.

After that, a Turbo Debt representative will go over your options and explain how the process works.

If it makes sense for you, you can enroll and begin making payments under the plan you choose.

Benefits of Turbo Debt

Turbo Debt offers features and services that some borrowers may find helpful.

Broad Accessibility & Support

Turbo Debt serves clients in multiple U.S. states and territories. It also provides Spanish support and keeps extended business hours for easier scheduling.

No Upfront Fees

You don’t pay anything unless a settlement is reached.

Potential for Significant Savings

Turbo Debt reports that clients may save around 46% before fees. After fees, savings tend to land closer to 20% to 25%.

Risks & Limitations of Turbo Debt

Turbo Debt may work for some borrowers, but there are real limits to consider before enrolling.

Credit Score Impact

Since you stop paying creditors while saving for settlement, your credit score will drop. Missed payments and delinquent accounts can stay on your credit report for years.

No Guarantees

Turbo Debt doesn’t promise specific results. Some creditors may not agree to negotiate, and outcomes vary. In some cases, you could end up paying more than expected.

Fees Are Significant

Fees can reach up to 25% of enrolled debt. Depending on how much is settled, the final savings after fees may be smaller than expected.

Lawsuit/Collection Risk

During the process, creditors may still send your account to collections, sue, garnish wages, or file liens, especially if balances go unpaid for several months.

Read More: Can Debt Consolidation Affect Your Credit Score? Pros, Cons & Best Practices

Turbo Debt Reviews

On review platforms, Turbo Debt reviews are generally mixed.

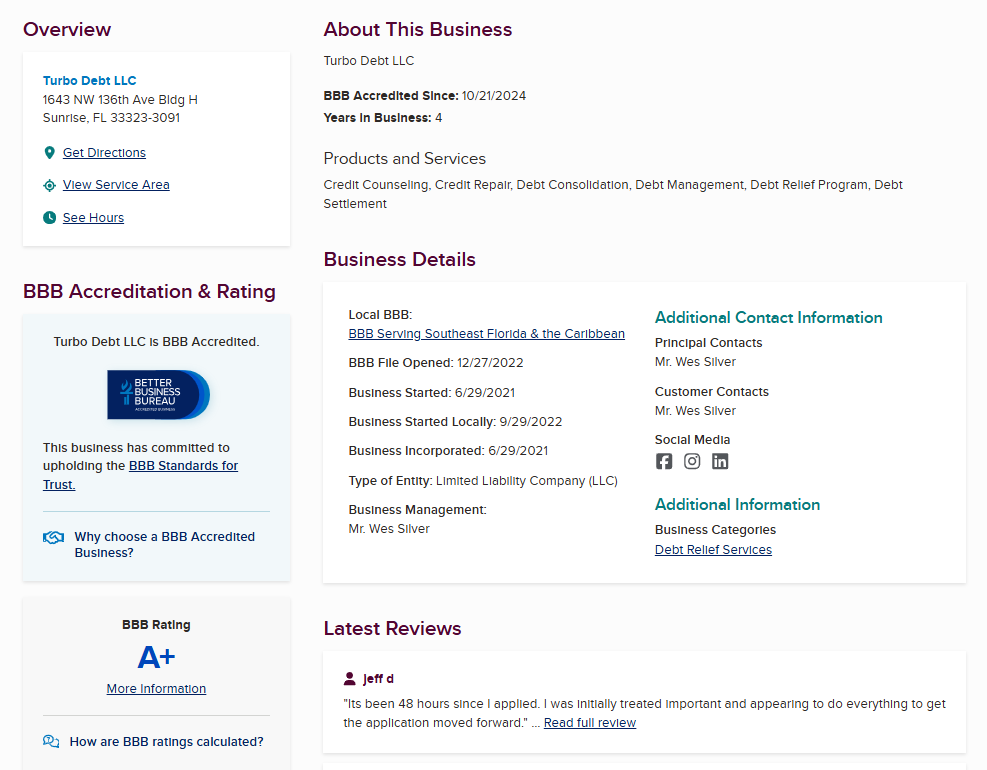

Better Business Bureau (BBB) Reviews

Turbo Debt is BBB accredited and currently has an A+ rating. It has an average of 4.87 stars from over 1,300 reviews.

Several people note that their reps were helpful and made things understandable. Some complaints, however, are centered on pushy phone sales or poor follow-up.

In the past three years, Turbo Debt has received 88 complaints, with 14 closed in the last 12 months. These common reasons revolve around service issues, repeated attempts to get in touch, and mismatched expectations.

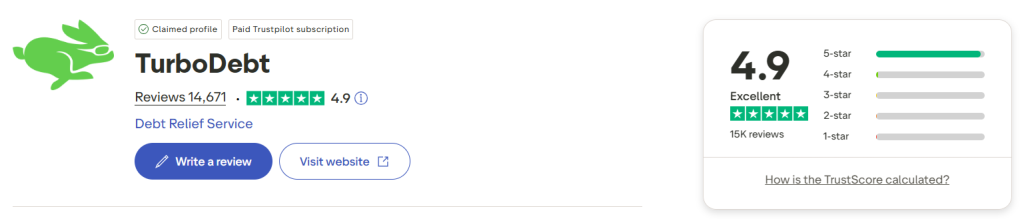

Trustpilot Reviews

On Trustpilot, Turbo Debt has a 4.9 TrustScore, based on over 14,000 reviews.

Reviewers describe their rep as patient, respectful, and easy to work with. Many say the signup process felt simple and organized.

One-star reviewers mainly complain about aggressive sales tactics, unclear terms, and a lack of transparency during the signup process. Some also report poor communication and say the service didn’t meet expectations or felt untrustworthy.

Reddit Reviews

Turbo Debt- Has anyone worked with them to get out to debt?

by

u/Ok-Anxiety-3008 in

DebtAdvice

Reddit feedback is more split. Some users say Turbo Debt helped them take control of their debt and explore realistic options.

Others felt pressured during the consultation or confused about how enrolled debt translates to actual savings.

There are also concerns about credit score drops and collection activity during the program.

Some Redditors recommend comparing it with credit counseling, debt management, or debt consolidation loans before signing up.

When to Use Turbo Debt

Turbo Debt might make sense when unsecured debt has become unmanageable, and other options no longer work.

You Owe $10,000 or More in Unsecured Debt

Turbo Debt only works with clients who owe at least $10,000 in unsecured debt. This amount is usually the minimum where settlement becomes a practical option after fees.

You Accept Credit Score and Legal Risks

If you’re willing to take credit score and legal hits in exchange for the chance to reduce what you owe through settlement, you can go for Turbo Debt.

You’ve Run Out of Lower-Risk Options

Turbo Debt may be relevant for your situation when other paths are no longer realistic.

When to Avoid Turbo Debt

Turbo Debt isn’t designed for every debt situation.

You Can Still Make Minimum Payments

If you can keep up with your monthly payments, you can avoid damaging your credit and stay current. In this case, settlement likely isn’t needed.

You Need Fast Results Without Collection Risk

Settlement takes time, and creditors can still take legal action while you’re in the program. If you need a quick solution and can’t risk that, this approach may not work.

You Have Secured or Government-Backed Debts

If most of your balances are tied to debt secured by property or backed by the government, Turbo Debt won’t apply.

You Prefer to Keep Accounts Current

If you’d rather avoid missed payments, programs like debt management plans or credit counseling may be a better fit.

Is Turbo Debt Legit?

Yes. TurboDebt is a legitimate debt settlement company. However, “legit” doesn’t mean risk-free.

How Turbo Debt Compares to Other Debt Relief Services

| Company | Requirements / Fees | Eligible / Ineligible Debts | Programs / Details |

|---|---|---|---|

| Turbo Debt | Minimum $10k unsecured debt. Fee about 25%, charged after settlement. | Eligible: Credit cards, personal, medical, business, veteran, and divorce debts. Ineligible: Secured debts. | Debt settlement (12–48 months). Credit may drop while payments pause. |

| Credit Associates | Min. $10k. Fee ~25% of enrolled debt. | Eligible: Unsecured (cards, medical, loans, collections, some private student loans). Ineligible: Secured or government debts. | Debt settlement (24–36 months). Uses a savings account. Credit may fall temporarily. |

| JG Wentworth | Min. $10k. Fees 18–25%. No upfront charges. | Eligible: Most unsecured debts. Ineligible: Secured debts. | Debt settlement (24–60 months). Credit score may decline during program. |

| Accredited Debt Relief | $1k–$100k. Success fee near 25%. APR 4.9–35.99%. | Eligible: Unsecured debts (cards, medical, personal, private student loans). Ineligible: Secured or government debts. | Debt consolidation (24–48 months). Credit may be affected; collectors might contact you. |

| Money Management International (MMI) | No minimum. Setup $33–$75. Monthly $25–$59. | Eligible: Unsecured debts through payment plans (not settlement). | Nonprofit counseling and DMPs. Often cuts interest rates by 20%+. |

| Pacific Debt Relief | Min. $10k. Fee around 25%; $10 one-time setup; $10 monthly account fee | Eligible: Unsecured (credit cards, utilities, medical). Ineligible: Secured debts. | Debt settlement (2–4 years). Free consultation. IAPDA accredited. |

| National Debt Relief | Min. $7,500. $9 setup + $9.85 monthly. Fee up to 25%. | Eligible: Unsecured (cards, loans, payday, medical, collections). Ineligible: Mortgages, auto, child support, taxes, federal student loans. | Debt settlement with flexible timelines and clear pricing. |