U.S. household debt reached $18.8 trillion in the fourth quarter of 2025, marking a $191 billion increase from the previous quarter. Amidst these rising balances and tighter household budgets, Beyond Finance presents itself as a structured alternative for consumers unable to keep up with compounding unsecured loans.

Therefore, this review will examine Beyond Finance’s debt consolidation services and assess their costs, process, pros, and cons to help you determine whether they are suitable for your debt relief needs.

What Is Beyond Finance?

Beyond Finance is a debt relief company that works with individuals with unsecured debt, such as credit cards, personal loans, medical bills, private student loans, lines of credit, and accounts already in collections.

Instead of issuing loans, it negotiates directly with creditors to reduce the total amount owed.

How Does Beyond Finance Work?

Beyond Finance’s application process is as follows:

Free Consultation

The process starts with a phone consultation. A team member asks specific questions about your current balances, creditors, and monthly budget. This helps assess if a settlement strategy aligns with your financial limits and creditor mix.

Pick an Option That Matches Your Situation

After reviewing your details, the team outlines possible repayment structures. You choose based on timeline, monthly affordability, and how aggressively you want to reduce your total debt.

Pay Debt Within 24 to 48 Months

Most clients see their debt paid off within the first few months. From there, consistent deposits into a dedicated account allow the team to negotiate remaining balances.

Full resolution typically occurs within 2 to 4 years, depending on the amount and the creditor’s response time.

Beyond Finance Debt Consolidation Details

| Feature | Details |

| Type | Debt Consolidation |

| Minimum Debt | $10,000 in unsecured debt |

| Eligible Debt Types | Credit cards, personal loans, medical bills, private student loans, collections |

| Service Model | Negotiates consolidations with creditors on the client’s behalf |

| Program Length | 24 to 48 months |

| Fees | Origination fees ranging from 1% to 6% Up to 25% of enrolled debt (only after successful settlement) |

| Credit Score Requirement | No minimum |

| Availability | Not available in all states |

| Initial Consultation | Free |

| Risk Factors | Credit impact, legal action, tax on forgiven debt |

What Services Does Beyond Finance Offer?

Beyond Finance promotes debt consolidation as its flagship service through partner lenders. These affiliates extend personal loan offers ranging from $1,000 to $100,000.

Approved borrowers use these funds to combine multiple unsecured debts into a single loan with structured repayment terms. The service functions as a referral channel, not a direct lender, and terms vary based on individual credit profiles.

Who Qualifies for Beyond Finance Loans?

Beyond Finance is best for borrowers with at least $10,000 in unsecured debt. To qualify, applicants must live in a state where the service is available and show they can make consistent monthly payments. Income stability and creditor types also factor into your eligibility.

At the same time, applicants must demonstrate they can serve their obligations and commitments.

How Much Does Beyond Finance Cost?

- APRs range from 4.9% to 35.99%

- Origination fees: 1% to 6%

- Loan terms: 4 to 84 months (based on credit and loan size)

- Example: A $23,760 loan at 18% APR, 4.95% origination fee, 48-month term = $697.95/month

- Borrower nets $22,584 after the $1,176 origination fee

- Total repayment: $33,501.60

- Negotiated settlement clients typically repay ~55% of enrolled debt (before fees)

- Settlement fees are often ~25% of enrolled debt, charged only after successful resolution

Benefits of Beyond Finance

Here’s how Beyond Finance’s service model stands out in the following ways:

Personalized Debt Relief Services

Beyond Finance plans match the client’s total enrolled debt with what they can realistically afford each month.

Advisors assign one-on-one support and outline the negotiation timeline in stages. This gives you an overview of what to expect across the repayment process.

Helps Reduce Your Debt

Clients generally reduce their required monthly payments by about 45%, which can help ease short-term financial pressure.

This model focuses on consolidating balances sooner instead of paying extended interest over decades. For people who qualify, it can significantly shorten repayment timelines.

No Upfront Fees

Beyond Finance does not charge clients until consolidations occur.

The fee is performance-based and calculated as a percentage of the total enrolled amount. No payment is collected until results are confirmed.

Risks of Beyond Finance

Beyond Finance also has the following drawbacks:

Fees May Be Higher

Some clients pay fees as high as 25% of the debt they enroll, which places Beyond Finance at the upper end compared to other firms that charge between 15% and 25%, depending on the complexity and amount of debt involved.

These costs can affect your budget and continue to accrue under certain circumstances.

You May Not Qualify

Eligibility requires a minimum amount of unsecured debt, usually $10,000 or more. Some creditors or types of unsecured loans may also fall outside the program.

In addition, state availability can limit who can apply.

Not Transparent About the Process

Upfront information is limited before the consultation. Specifics around fee breakdowns, negotiation timelines, and creditor engagement vary case by case, which can leave clients uncertain until after enrollment.

No Guarantee of How Much You’ll Save

Debt reduction depends on several variables. Creditors must agree to consolidate, and the amount saved will depend on each negotiation. No fixed discount or outcome is promised.

Your Creditor May Sue You

While consolidation is the goal, some creditors may pursue legal action instead. This risk remains throughout the process until an agreement is reached.

May Impact Your Credit Score

Enrollees typically stop paying creditors once the program begins. This leads to delinquencies on record and a drop in credit scores during the early stages.

Tax Implications

Forgiven debt may count as taxable income. Depending on the IRS threshold, clients may receive a 1099-C from creditors if the savings exceed $600.

Therefore, be sure to read IRS guidelines and file appropriate forms.

Beyond Finance May Increase Your Debt

If negotiations take time, interest and penalties may continue accruing. This can increase balances temporarily before a settlement is reached.

Not Available in All States

Regulatory restrictions prevent Beyond Finance from offering its services in certain areas. Prospective clients should check availability before starting the process or consider alternatives if their state is excluded.

San Diego, for example, is one of the states where Beyond Finance is active, but availability can change. Always check current coverage before applying.

Read More: Can Debt Consolidation Affect Your Credit Score? Pros, Cons & Best Practices

Beyond Finance Reviews

Public feedback on Beyond Finance varies across the following platforms:

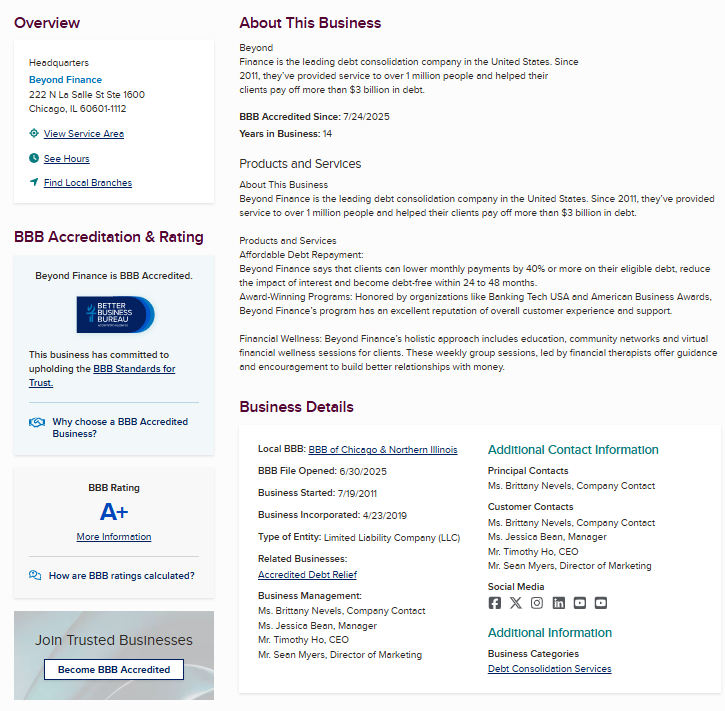

Better Business Bureau (BBB) Reviews

In BBB, Beyond Finance is accredited, has an A+ rating, and has a 4.76-star average from 10,000 reviews.

The company has received 662 complaints over the past three years, 275 of which were resolved in the last twelve months.

Most complaints are billing, service, and product issues.

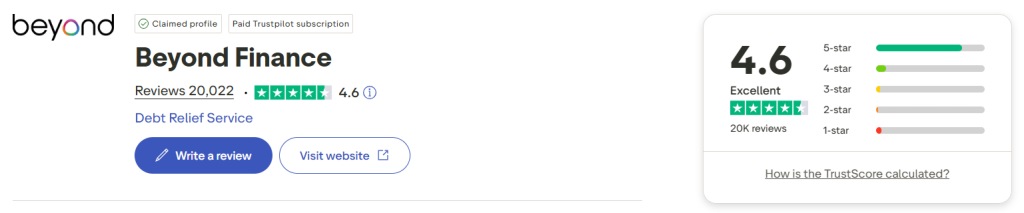

Trustpilot Reviews

Beyond Finance holds a 4.6-star rating on Trustpilot, based on over 20,000 reviews.

Many people report positive experiences with their advisors and appreciate the lowered payments. However, some noted early confusion about timelines, unclear charges, and slow processing.

Reddit Reviews

User posts about Beyond Finance on Reddit are mixed.

Some people say the program helped them settle debt faster than expected, while others caution against potential credit score drops and legal risks.

Therefore, remember to check Reddit threads like these to account for real experiences.

Alternatives to Beyond Finance

If Beyond Finance doesn’t fit your needs or eligibility, the following alternatives can help you manage unsecured debt.

Debt Avalanche

Debt avalanche is a method that targets the highest-interest debts first.

By putting extra funds toward those balances while making minimum payments on others, you reduce total interest paid.

This option is ideal for borrowers focused on long-term cost savings.

Debt Snowball

In the debt snowball approach, you pay off the smallest balances first, regardless of interest rate.

The goal is to eliminate accounts quickly and build momentum. It can help build confidence and motivation for those who want to monitor progress.

DIY Debt Strategy

Some people use a DIY debt strategy by negotiating directly with creditors. This may involve asking for lower interest, setting up reduced payment plans, or exploring hardship programs.

Since this is an independent debt management technique, success depends on timing, negotiation skills, and willingness to collaborate or respond to creditor demands.

Personal Loan for Debt Consolidation

Borrowers with good credit may qualify for a personal loan that combines multiple debts into one payment. The loan usually carries a fixed interest rate and term.

This option works best for those with predictable income and strong repayment habits.

Credit Counseling

Credit counseling agencies offer structured guidance through certified counselors. These sessions may lead to enrollment in a debt management plan, which consolidates payments and lowers interest.

Debt Consolidation via Banks and Creditors

Some banks extend consolidation offers directly to account holders. These opportunities typically include lower rates and bundled payment plans but depend on creditworthiness and customer history.

Debt Settlement via Banks and Creditors

Banks and creditors may agree to settle debts in a single lump-sum payment. This often bypasses third-party services and resolves balances quickly.

However, it usually requires available cash and may still reflect negatively on your credit file.

The process involves debt settlement proposals, which outline the lump sum and your repayment amount.

These letters formalize agreements and protect the client from future collection attempts, provided that the bank or creditor accepts the settlement.

Unlike debt settlement companies, which negotiate with creditors on your behalf, you’ll sign settlement letters and file them personally with your bank or creditor.

As a result, you have more control over the negotiations.

Beyond Finance vs. Other Debt Relief Companies

| Company | Costs | Requirements |

|---|---|---|

| Beyond Finance | Origination fees ranging from 1% to 6%; up to 25% of enrolled debt (only after successful settlement) | Minimum $10,000 in unsecured debt; no minimum credit score; not available in all states |

| Accredited Debt Relief | Charges and fees vary by the company you’re ultimately connected with | Must be at least 18 years old and a legal US resident; additional terms may apply based on services and products used |

| National Debt Relief | 15–25% of total enrolled debt | Must have a legitimate financial hardship and a minimum of $7,500 in debt |

| Freedom Debt Relief | Monthly payment based on enrolled debt, no upfront fees | Must have at least $7,500 in unsecured debt, demonstrate financial hardship, and live in a serviced state |