J.D. Power found that as of February 2026, 68% of U.S. consumers are financially unhealthy. The number dipped from 72% in January, but most households are still stretched thin.

Personal loans are one of the first places people look when bills or an emergency drain their savings. Some borrowers also explore the best credit cards.

Bad credit, though, closes a lot of doors with traditional lenders.

Borrowers in those situations may turn to options like Transform Credit, which rebranded as Together Loans in December 2025. But is it the right choice for you?

What Is Transform Credit?

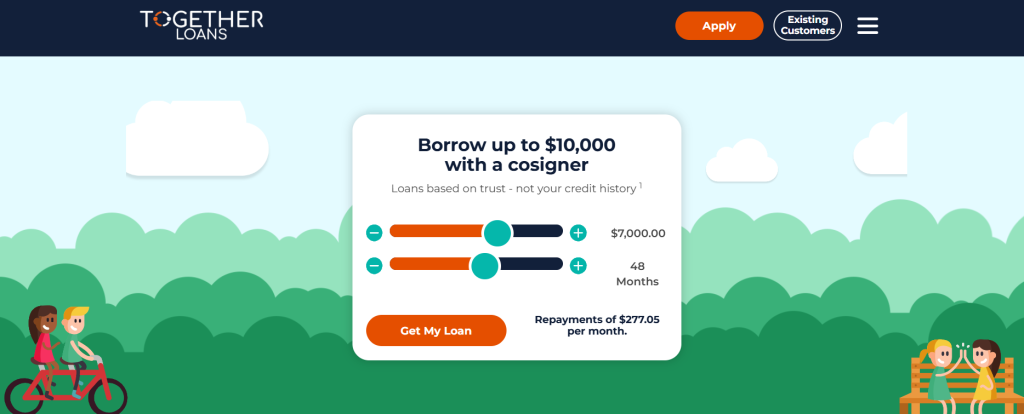

Transform Credit is a Chicago-based personal loan provider that offers financing to people with poor or limited credit. It is a direct lender. It is now called Together Loans.

Transform Credit Loan Details

| Feature | Details |

|---|---|

| Loan Amount | Maximum $10,000 |

| Repayment Term | 24 to 60 months |

| APR | 35.99% (fixed) |

| Funding Time | Within 24 hours of co-signer approval |

| Required Credit Score | None for borrower; 750+ for co-signer |

| Co-signer Required | Yes |

| Early Repayment Penalty | None |

| Fees | No application or origination fees disclosed |

| Credit Builder Program | $5/month optional fee; reported to credit bureaus |

Who Qualifies for a Transform Credit Loan?

You don’t need good credit to apply with Transform Credit, but your co-signer does. They’ll need a credit score of at least 750, and being a homeowner can help your chances.

Both of you must be U.S. residents, at least 18 years old, and have some form of steady income. You’ll also need valid IDs to move forward with the application.

How to Apply for a Transform Credit Loan?

Applying is quick. You fill out a short form, then add your co-signer’s information. They’ll get a link to complete their part.

If you’re both approved, the money is sent to your bank account within one business day.

Why Does Transform Credit Require a Co-Signer?

Transform Credit relies on trust instead of traditional credit checks. That’s why it asks for a co-signer who guarantees the loan. This approach helps protect the company while giving people with bad credit a fair chance to get the money they need.

Benefits of Getting a Transform Credit Loan

Transform Credit is accessible to borrowers with bad credit or no credit history at all in the following ways:

- Bad Credit-Friendly: No credit needed if you have a qualified co-signer. Great option if you’ve been turned down by most lenders.

- Approval Based on Co-Signer: Your co-signer’s good credit helps you qualify. Avoids the risks of a payday loan or shady company.

- Build Credit Over Time: On-time payments are reported to bureaus, helping boost your credit if you’re rebuilding.

- Fast, Online Process: Simple, 100% online application. Many borrowers say they felt secure and liked how straightforward it was.

- No Hidden Fees: No origination fees or prepayment penalties. Just a $5 fee if you join the Credit Builder program.

Drawbacks and Risks of Transform Credit Loans

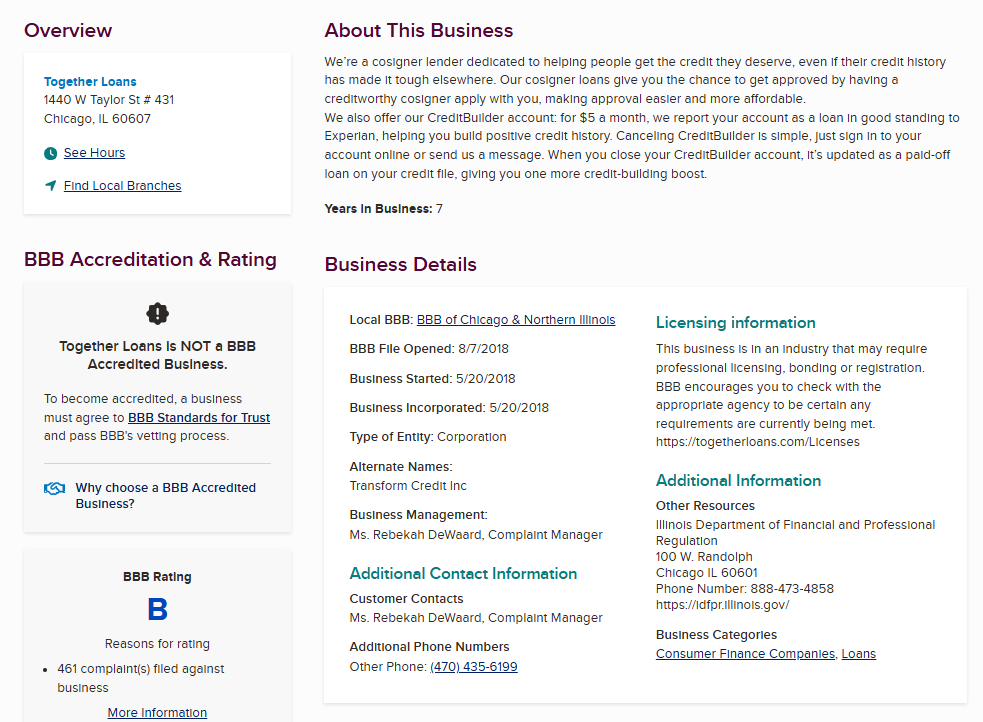

While Transform Credit appeals to borrowers with bad credit, it has a poor Better Business Bureau (BBB) reputation due to complaint patterns and possible fraud triggers.

In line with this, many users flagged the following issues:

- Unwanted Loans: Some co-signer loans were approved without full borrower confirmation, raising red flags during the loan application process.

- Hidden Fees: A few applicants noticed additional fees tied to monthly payments or unclear Credit Builder terms.

- Slow Support: Customer service was described as slow and not very helpful, even when a professional worker was needed to fix issues like an extra payment.

- Co-Signer Risk: Missed due dates can hurt both your credit and your family member’s finances, especially if that person is responsible for repayment.

- Limited Availability: You must live in a state like South Dakota or New Hampshire to borrow. The company may not accept applications from other areas.

- High APR: The interest is fixed at 35.99%, which can make the loan product costly over a long loan term. You may save money by comparing offers from other lenders like Credit Inc.

Transform Credit Reviews

Here’s what real customers and users across platforms say about Transform Credit.

Better Business Bureau (BBB) Reviews

Transform Credit has a B rating with the BBB, but it has an average of 4.5 stars across over 1,400 reviews.

Many people say the loan process went smoothly and they felt supported throughout. However, there are several complaints about billing issues, unexpected charges, credit checks, and confusion around cosigner responsibilities.

It seems to work well for some, but the company could improve how it communicates the details.

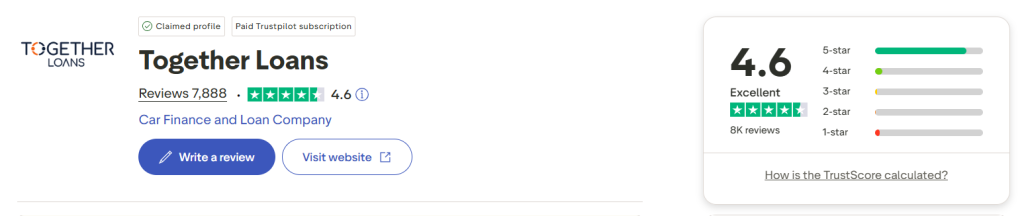

Trustpilot Reviews

As of April 2026, Transform Credit has over 7,000 reviews on Trustpilot with a 4.6 TrustScore.

Most reviewers say they had a great experience, especially when other lenders turned them down. People often mention fast turnaround times and helpful customer service.

On the flip side, some users weren’t thrilled about the co-signer requirement, the way funds are routed through the co-signer, and the detailed verification process.

Reddit Reviews

Is transform credit legit? Looking for real experiences

by

u/jackandbluedog in

moneyadvice

Reddit users generally agree that Transform Credit is legit. People have gotten loans, made payments, and even seen their credit improve.

Still, the cosigner requirement is a major sticking point. It puts real responsibility on the cosigner, and some borrowers felt uneasy about that.

TransformCredit reviews? is it legit?

by

u/TurnOnTheDevon in

financeonloans

A few also pointed out that funds might go to the cosigner’s account instead of the borrower’s, and credit reporting may not cover all three major bureaus.

Most Redditors say it’s only a good option if you’re confident in making every payment and your cosigner fully understands what they’re signing up for.

What Is the $5 Charge in Transform Credit?

The $5 charge is tied to the Credit Builder program.

When you enroll, you agree to a $5 monthly fee that gets reported to credit bureaus. These monthly payments help boost your credit profile and show consistent repayment behavior.

Moreover, notifications are sent before the payment is drafted from your account, so you always know when it’s coming.

For those with bad credit, this can be a low-cost way to rebuild, assuming all payments are made on time.

However, because of unclear terms, some borrowers noted that they were unknowingly charged $5 despite not enrolling in the Credit Builder program.

Who Shouldn’t Use Transform Credit

Here are the types of borrowers who should not consider Transform Credit:

No Co-Signer With Good Credit

Approval depends on your co-signer’s credit file. If their score is below 750 or they have recently made late payments, Transform Credit can reject your application.

Cannot Prequalify Without a Hard Credit Check

Transform Credit performs a hard inquiry on the co-signer’s credit, which may lower their score slightly. There’s no soft pull option to check rates beforehand.

Live in a State Where Transform Credit Is Not Available

The loan is only available in specific states. If you don’t reside in one of those, Transform Credit may deny your application even if your co-signer lives in an eligible location.

Cannot Have Fixed High-Interest Loans

The 35.99% APR increases total repayment costs significantly. If you qualify elsewhere for a lower interest rate, that may be the better option.

Do Not Want to Burden Co-Signers

If you miss payments, your co-signer becomes fully responsible. This obligation can damage relationships and impact their credit as well.

How Transform Credit Compares to Other Lenders

| Lender | APR | Min. Credit Score | Loan Amount |

|---|---|---|---|

| Transform Credit Personal Loans | 35.99% (fixed) | None for borrower; 750+ co-signer required | Up to $10,000 |

| Best Egg Personal Loans | 6.99% – 35.99% | 640 | $2,000 – $100,000 |

| Upgrade Personal Loans | 7.74% – 35.99% | 580 | $1,000 – $50,000 |

| SoFi Personal Loans | 8.74% – 35.49% | 680 | $5,000 – $100,000 |

| LightStream Personal Loans | 6.49% – 24.89% | Good to excellent credit | $5,000 – $100,000 |

| Upstart Personal Loans | 6.20% – 35.99% | 300 | $1,000 – $75,000 |