Lenders offering fast-access credit are no longer rare, but consistent delivery is harder to find. CreditFresh operates in this space with increasing visibility, especially among users who prioritize speed without sacrificing predictability.

Some borrowers view CrediFresh as a practical alternative to rigid bank processes, while others see it as another option in a crowded field of short-term lenders.

So, how do you qualify, and is this line of credit really worth it?

What Is CreditFresh?

CreditFresh is a financial service developed by Propel Holdings Inc., launched in 2019.

It operates as a credit platform that provides access to personal lines of credit issued by a bank partner.

This lender also distinguishes itself by focusing on short-term credit solutions with flexible repayment.

Read More: Overdraft vs. Lines of Credit – Understanding the Key Differences

How Does a CreditFresh Line of Credit Work?

A CreditFresh line of credit functions as a reusable credit limit.

Credit limits typically range from $500 to $5,000. Applicants can prequalify before submitting a full application. This initial step estimates the credit limit without affecting your credit score.

Approved users access funds through their online account. You can draw the funds in flexible amounts, as long as the total does not exceed the available credit. Requests made before 3:30 p.m. Eastern on business days usually process the same day.

Additionally, payments are scheduled to match the borrower’s income frequency. Most accounts follow a biweekly or monthly schedule.

CreditFresh Loan Details: Terms, Limits, Fees, Availability

| Detail | Information |

| Loan Type | Personal Line of Credit |

| Credit Limit | $500 to $5,000 |

| Application Method | Online only |

| Approval Time | Same day possible (if verified early) |

| Funding Speed | Same business day if requested by 3:30 p.m. ET |

| Repayment Schedule | Biweekly or monthly (based on income) |

| Minimum Payment Includes | Billing cycle charge + required principal |

| Fees | No origination or prepayment fees |

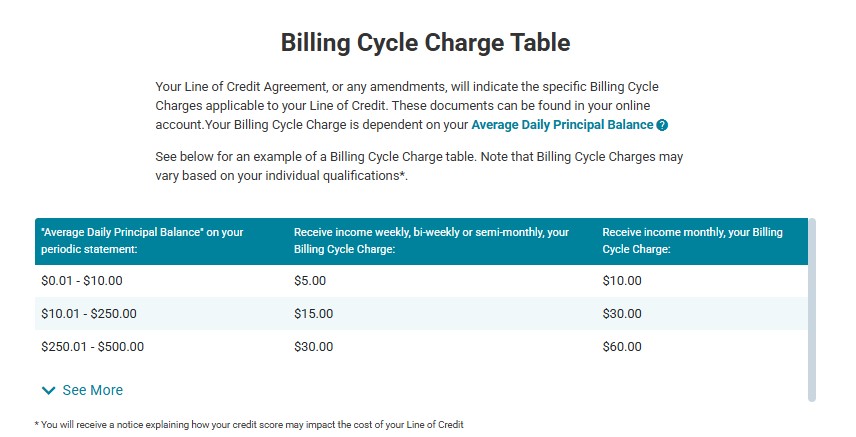

| Billing Cycle Charge | Based on average daily principal balance |

| Reports to Bureaus | Yes |

| Credit Check | Soft pull for prequalification |

| Availability | Select U.S. states |

| Customer Support | Phone and email |

You May Also Like: Charge vs Credit Card: Pros, Cons, and Key Comparisons

Where to Use a CreditFresh Line of Credit

CreditFresh is most suitable for the following expenses:

Emergency Expenses

A line of credit can help cover urgent costs that require immediate attention. These costs include car repairs or essential home repairs like broken plumbing or heating issues. You can also use it for medical bills that emergency funds and insurance can’t cover.

Additional Student Loans

When federal aid or institutional student loans don’t fully cover school-related expenses, a line of credit can cover the gap.

You can use it for tuition balances, housing deposits, textbooks, or lab fees that fall outside standard student loan disbursements.

Ongoing Projects

Some expenses are unpredictable until the work is underway. Weddings, home remodeling, or long-term caregiving needs usually come with unclear or shifting budgets.

A line of credit provides controlled access to fund these costs without overborrowing upfront.

Consolidating Debt

Using a line of credit to pay off higher-interest balances may simplify repayment. This option allows you to combine multiple credit card debts or payday loans into one account with a single payment schedule.

Big Purchases

A line of credit can break the cost of items that exceed what’s available in a single paycheck, such as appliances, furniture, or tech upgrades, into manageable draws.

This can make large purchases more feasible without using traditional installment loans.

Paying Bills

A line of credit can cover bills that you cannot delay during short-term income gaps. These include rent, utilities, phone plans, and insurance premiums.

Read More: The Best Money Management Apps of 2025

Who’s Eligible for a CreditFresh Line of Credit?

To qualify for a CreditFresh line of credit, you must meet the following requirements:

- Legal age based on your state’s laws

- U.S. citizen or permanent resident

- An active bank account

- Regular and consistent income source

- Valid phone number and active email address

Currently, CreditFresh products are unavailable to active-duty military members or their dependents, as none of the available credit options meet federal lending criteria under the Military Lending Act.

Applications are reviewed individually, and it does not disclose whether it supports co-applicants.

What Are CreditFresh’s Costs and Fees? (With Computation Example)

CreditFresh does not use a fixed APR like traditional personal loans.

Instead, the total cost is based on two components applied each billing cycle: a required principal contribution and a billing cycle fee.

The principal contribution is calculated from your average daily principal balance. The billing cycle charge is also in this average, divided by the number of days in the cycle. Together, these determine your minimum payment.

Example 1: Monthly Income Frequency

In this setup, payments occur about once every 30 days. If you borrow $1,500, here’s how the first three months would look:

| Billing cycle | 1 | 2 | 3 |

| Balance | $1,500 | $1,470 | $1,440.60 |

| Principal payment | $30 | $29.40 | $28.81 |

| Billing cycle charge | $184 | $184 | $184 |

| Min. payment | $214 | $213.40 | $212.81 |

| New balance | $1,470 | $1,440.60 | $1,411.79 |

After three months, you would have paid $552 but still owe over $1,400. This is due to the billing cycle cost, which stays high even as the balance decreases.

Example 2: Non-Monthly Income Frequency

With payments scheduled about every 14 days, the cycle charge is lower but applies more frequently. Here’s a breakdown using a $1,500 draw:

| Billing cycle | Balance | Min. payment | New balance |

| 1 | $1,500 | $100 | $1,485 |

| 2 | $1,485 | $99.85 | $1,470.15 |

| 3 | $1,470 | $99.70 | $1,455.45 |

| 4 | $1,455.45 | $99.55 | $1,440.90 |

| 5 | $1,440.90 | $99.41 | $1,426.49 |

| 6 | $1,426.49 | $99.26 | $1,412.23 |

Each payment includes a mandatory principal portion and an $85 billing cycle charge.

Although there are no additional fees, such as origination or late charges, the cumulative cost can still exceed the effective APR of traditional loans.

For context, a $1,500 personal loan at 12% APR would lead to monthly payments of around $70.61.

After 90 days, the balance would drop to about $1,288, with total payments of $211.83. Borrowers typically pay this loan in 24 months, making the long-term cost lower.

You May Also Like: Good Debt vs Bad Debt: Differences Explained

How to Repay Your CreditFresh Line of Credit

CreditFresh sends a periodic statement before each due date. This statement includes your minimum payment and the exact date you must pay the due.

It is sent at least 14 days in advance, giving you time to review the charges and prepare the payment.

You can set up automatic payments through ACH by submitting an authorization form.

If approved, payments will be withdrawn directly from your bank based on the schedule provided in your statement.

This option helps avoid missed deadlines without requiring manual input for each cycle.

On the other hand, if you prefer to make payments manually, it also accepts debit card and prepaid card payments through its secure online portal.

You can log in and process payments without needing to contact support.

Remember that for every billing cycle with an outstanding balance, you must make at least the minimum payment.

Benefits of Using a CreditFresh Line of Credit

According to user reviews on platforms like Reddit, here are the advantages of using CreditFresh:

Fast Funding

If approved and a draw request is submitted by 3:30 p.m. Eastern on a business day, funds may be deposited into your account the same day. This speed can help cover urgent expenses without waiting for a traditional loan disbursement.

No Hidden Fees

Borrowers only pay the billing cycle, which is clearly defined in the agreement. CreditFresh does not add extra fees such as application or prepayment penalties, reducing the chance of unexpected costs.

Only Pay for What You Use

You only incur charges on the amount you draw from your credit line. If you don’t borrow, no billing cycle cost applies.

On-Time Payment Incentives

Borrowers who make payments on time may qualify for lower billing cycle charges and increased credit limits. These adjustments are not guaranteed but are based on repayment behavior.

Helps Build a Positive Credit Score

CreditFresh reports payment activity to credit bureaus. Therefore, making consistent, on-time payments can improve or rebuild your credit history.

No Hard Inquiry

Prequalification does not involve a hard credit pull. This lets you check eligibility without reducing your credit score during the initial step.

Read More: Credit Builder Credit Cards 101 Guide

Risks of CreditFresh Lines of Credit

Depending on your situation, below are the limitations, according to users, that could affect the platform and the loan’s usefulness:

Unclear Interest Rates

CreditFresh does not use a traditional APR model, which can make it challenging to compare interest rates and borrowing costs with other financial products.

Also, the billing cycle fee varies and is tied to your balance, not a fixed rate.

High Monthly Billing Cycle Charge

The billing cycle fee can be substantial relative to the amount borrowed. Since it applies to each cycle, even small draws may result in high overall repayment costs compared to fixed-rate loans.

Limited Eligibility Information

CreditFresh provides minimal detail about specific qualification criteria. Without clear benchmarks on income or credit requirements, applicants may feel uncertain about their approval.

Not Available in All States

As of June 2025, CreditFresh lines of credit are only available in select states. Residents in other states cannot currently apply.

The states are as follows:

- Alabama

- Alaska

- Arizona

- Arkansas

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Indiana

- Kentucky

- Kansas

- Louisiana

- Michigan

- Mississippi

- Missouri

- Montana

- Nebraska

- New Jersey

- North Carolina

- Ohio

- Oklahoma

- Pennsylvania

- South Carolina

- Tennessee

- Texas

- Utah

- West Virginia

- Wisconsin

- Wyoming

Lower Credit Limits

Unlike other lenders, which may offer up to $50,000 in credit, CreditFresh caps its lines at $5,000. For borrowers seeking larger amounts, this limit may not meet their needs.

You May Also Like: Collateral: What You Can Use for a Secured Loan

How to Apply for a CreditFresh Line of Credit

CreditFresh uses an online-only process to review applications, verify eligibility, and issue credit decisions.

At the same time, the process may require additional document uploads depending on the information you submit.

Step 1: Apply Online

The online application begins with a short online form. You’ll be asked to provide basic personal, financial, and contact details. Most users complete this step in a few minutes.

Step 2: Get Approved

After submitting your application, you’ll be prompted to request a credit limit and verify your identity and banking information. A checking account is required to qualify.

To verify your bank, you can use one of the following:

- Online Instant Account Verification

Many applicants can complete verification through DecisionLogic. This method links directly to your bank and typically takes only a few minutes to process. - Phone Verification

If online verification isn’t possible, customer service may help confirm your bank account over the phone. This method can take longer due to possible hold times with your bank.

If CreditFresh cannot verify certain information electronically or over the phone, you will be asked to submit documents.

You can upload these by logging into your account, navigating to your profile, selecting “Upload Document,” and submitting files up to 5MB each.

Accepted formats include image and PDF files. You must upload each document separately.

If needed, documents can also be emailed to [email protected].

Additional documents may include:

- A voided check or other proof of bank account

- A valid, unexpired government-issued ID

- Recent proof of income, such as a bank statement or pay stub, dated within 30 days

- Proof of residence, like a utility bill

Once your application is approved, you will receive a confirmation email with the next steps.

Step 3: Request a Draw Online

After approval, you can access your account to request funds. If the request is submitted on a business day before 3:30 p.m. Eastern, the deposit may arrive in your bank account the same day.

Read More: What Type of Loan Fits You Best?

Is CreditFresh Right for You?

CreditFresh may be a suitable option in certain situations, but not all borrowers will benefit from its structure.

When It May Make Sense

If You’re Denied Elsewhere

If banks or mainstream lenders have turned down your application, CreditFresh could provide access where other sources have declined. It focuses on consumers with less-than-perfect credit who still meet basic financial requirements.

Time-Sensitive Expenses

When time-sensitive expenses come up and cash isn’t available, the speed of the loan application process may help. Access to same-day funds can make a difference when dealing with urgent bills or repairs.

Short-Term Financial Gaps

If your budget has a temporary gap due to delayed income or irregular pay cycles, a line of credit with flexible draws may help cover immediate needs without locking you into a traditional installment.

When to Avoid

You Qualify For Traditional Credit

If you’re eligible for a personal loan or credit card with a low interest rate, those options will likely cost less. Moreover, traditional lenders typically offer clearer terms and longer repayment schedules.

Long-Term Repayment Needed

CreditFresh is designed for short-term borrowing. If you expect to carry a balance for many months, the billing cycle costs can add up quickly and outweigh the benefits.

You’re Fee-Sensitive

Even though CreditFresh avoids typical loan fees, the billing cycle cost can be high. If you prefer predictable interest or need to minimize cost, this credit structure may not align with your priorities.

You May Also Like: What Happens if You’re Not Approved for a Loan?

CreditFresh vs. Other Lenders

| Lender | Type | Loan Amount | APR / Fees | Credit Check | Funding Time | Reports to Bureaus | Best For |

|---|---|---|---|---|---|---|---|

| CreditFresh | Line of credit | $500–$5,000 | Billing cycle charge | Soft pull (prequalify) | Same-day (if early draw) | Yes | Short-term emergencies |

| Varo | Bank + personal loans | Up to $500 | No monthly fee, $1.60–$40 transfer fee | Yes | 1–2 business days | Yes | Traditional lending needs |

| Earnin | Pay advance app | Up to $150/day, $750 max | Voluntary tip + fee | No | 1–2 business days free, faster for a fee | Yes | Early paycheck access |

| Current | Neobank + overdraft | $50 to $750 | No mandatory fees | No | Up to 3 days, or within an hour (paid) | Yes | Small cash gaps |

| OppLoans | Installment | $500 to $5,000 | 160% to 195% | Soft or hard pull | Same business day | Yes | Short-term expenses |

| Cleo | Budget + cash advance | Up to $250 | $5.99 monthly membership | No | 3–4 days, or instant (paid) | Yes | Budget help + small cash |

| CreditNinja | Installment loan | $300 to $5,000 | Triple-digit APR possible | May check | Same day | Yes | Higher-risk borrowers |

Read More: What Types of Loans are Available for You?

Conclusion

CreditFresh is a legitimate lender, but the cost structure makes it one of the more expensive options available.

It may serve a purpose for borrowers with limited access to credit and urgent needs. Otherwise, you should consider lower-cost alternatives when necessary.

For more in-depth reviews on financial services, subscribe to Financial Daily Update today.

CreditFresh FAQs

Is CreditFresh Legit?

Yes. CreditFresh is a licensed online lender that partners with FDIC-insured banks CBW Bank and First Electronic Bank to issue personal lines of credit.

Its website uses standard security protocols to protect user information.

However, customer feedback is mixed. On Trustpilot, this lender holds a 4.5 out of 5 rating, with many users citing fast access to funds.

On the other hand, the Better Business Bureau (BBB) shows 108 complaints closed in the last 12 months but does not display an overall customer rating.

Do I Have to Pay Off My CreditFresh Balance in Full?

No. CreditFresh offers an open-end line of credit, so you’re required to make minimum payments based on your billing cycle.

Each payment includes a principal portion and a billing cycle fee based on your average daily balance.

Paying more than the minimum can reduce your cost, but full payoff is not required unless you choose to close the account.

Can I Cancel My CreditFresh Line of Credit?

Yes. You can cancel your agreement without penalty within one business day of your effective date.

To cancel, call 1-800-766-2007 or email [email protected].

If you received funds, you must return the principal in full to complete the cancellation.