As of early 2026, the average FICO Score in the U.S. sits at 714. That’s a one-point dip from 2025.

If your score’s stuck, slipping, or just not where it needs to be, you’re not alone. Missed payments, thin credit history, or old account closures can all get in the way, even with the best credit cards.

That’s usually when Kikoff reviews start popping up in search history – people looking for something that might help them get back on track.

This review looks closely at what using Kikoff actually feels like and whether it lives up to what people in credit recovery or early credit-building situations are hoping for.

What Is Kikoff?

Kikoff is a financial technology company founded in 2019 that focuses on helping people build or rebuild their credit scores.

The company is based in San Francisco and partners with Coastal Community Bank to issue its credit products.

Kikoff Credit Builder Details: Fees, Terms, Requirements, Availability

| Category | Details |

|---|---|

| Credit score | No minimum required |

| Type | $750 revolving line of credit |

| Fee | $5/month, no interest (basic plan) |

| Credit reporting | Reports to Equifax, Experian, TransUnion |

| Availability | Most U.S. states (excludes territories) |

| Credit impact | No hard pull; builds history and mix |

What Products Does Kikoff Offer?

Kikoff offers several tools designed to help users build credit.

Kikoff Credit Account

The credit account is a revolving credit line used only for digital purchases through the Kikoff store.

Kikoff Credit Builder Loan

The credit builder loan is a separate installment plan, usually around $10 per month for 12 months. It adds variety to a person’s credit file and works alongside the main credit account to build both payment history and credit mix.

Secured Credit Card

The Kikoff secured credit card requires a deposit and helps build a credit score through reported revolving usage.

Rent Reporting

Available with Premium and Ultimate plans, rent reporting lets users report rent payments, including up to 24 months of historical data.

Who Qualifies for Kikoff?

To sign up, users must be at least 18 years old, have a valid Social Security number or ITIN, and a U.S. address.

Eligibility also focuses on basic identity verification and the ability to link a bank account or debit card to make payments.

What Fees Does Kikoff Charge?

- Credit Account: Starts at $5/month

- Credit Builder Loan: $10/month for 12 months, 0% interest

- Kikoff secured credit card: Refundable deposit, varies by limit

- No late fees or prepayment penalties

- Money-back guarantee: 45 days, one-time use per person; applies to Kikoff Credit Service and Kikoff store items if canceled within the window

How to Enroll in Kikoff

You can apply directly through the Kikoff app or website. No credit check required. After signing up, you’ll link a checking account or debit card to set up payments.

From there, you’ll choose a plan:

- Basic ($5/month): Reports a $750 Kikoff tradeline, sends updates to Equifax, Experian, and TransUnion, includes weekly credit report access, credit tracking tools, and support.

- Premium ($20/month): Includes everything in Basic, plus a $2,500 tradeline, access to the Kikoff secured credit card, rent payments reporting, and debt negotiation support.

- Ultimate ($35/month): Adds a $3,500 tradeline, identity theft insurance, personal data protection, and all Premium features.

Individual results vary based on usage, account health, and Kikoff’s internal approval process.

Benefits of Kikoff

People new to credit or rebuilding after past issues can expect these features.

No Hard Credit Check or Interest

You can get approved without a credit check. Kikoff also doesn’t charge interest or penalty fees.

Reports to All Major Credit Bureaus

Your Kikoff account reports monthly to Experian, Equifax, and TransUnion, which can support a stronger payment history.

Low Cost and Easy Setup

Plans start at $5/month, and most users get approved right after sign-up. There are no hidden fees.

Accessible to New Borrowers

The setup is accessible for those without a long credit report.

Risks & Limitations of Kikoff

Kikoff offers an easy way to build credit, but it has some limits that may not fit every user’s needs.

Limited Use of Credit Line

The Kikoff account only works inside the Kikoff store. You can’t use it for outside purchases.

Late Payment Reporting

Missed payments are still reported to Equifax, Experian, and TransUnion. Even small missed charges can impact your credit report and delay a credit score increase.

Limited Credit Boost for Some Users

Those with longer credit histories or multiple active accounts might see little change in their credit utilization or overall score.

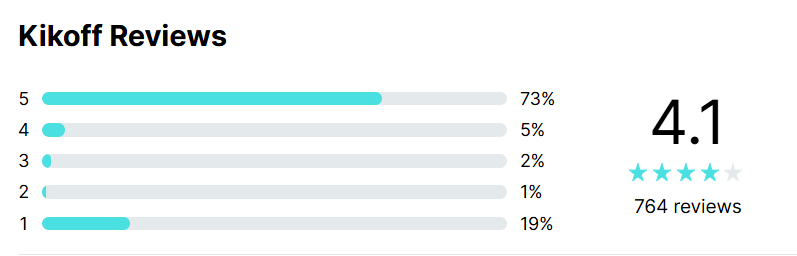

Kikoff Reviews

There’s a mix of strong Kikoff reviews and common complaints.

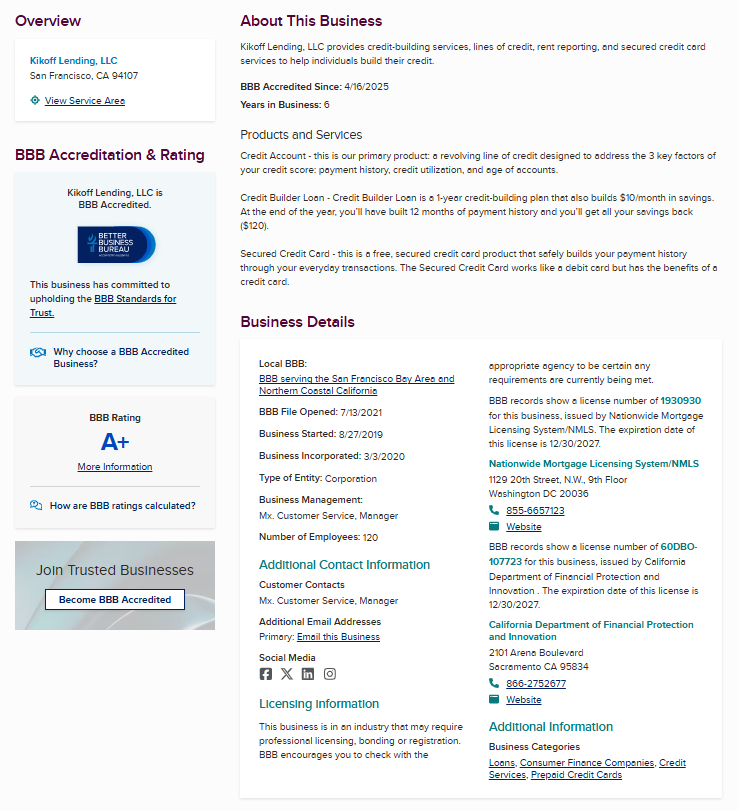

Better Business Bureau (BBB) Reviews

Kikoff has an A+ rating on the BBB and has been accredited since April 2025. The company is based in San Francisco and licensed.

It averages 4.28 stars from 600+ reviews. Positive feedback highlights the simple setup and early score improvements. Common complaints include billing problems, refund delays, and credit reporting issues.

BBB lists 1,363 complaints in the past three years. Most were answered, but not all were fully resolved.

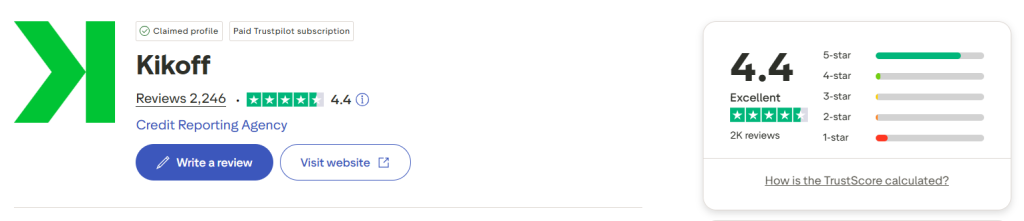

Trustpilot Reviews

Kikoff has over 2,200 reviews on Trustpilot. Most of them are positive. Users like the Kikoff app, credit tracking tools, and low monthly cost. Some report credit score increases of 50 points or more.

People also mention the rent reporting feature and flexible payment plans. On the downside, a few say they had trouble updating their debit card, correcting address details, or getting help from support.

Some are even skeptical about bold score increase claims.

WalletHub Reviews

WalletHub lists over 700 Kikoff reviews. The feedback is mixed, but leans slightly positive.

Many users mention the low monthly cost, consistent credit reporting, and a smooth sign-up process. Some also appreciate the credit tools included in the platform.

On the other side, complaints focus on refund delays, slow customer service, and confusion about canceling a subscription.

Some users also find the Kikoff line too limited.

Reddit Reviews

Reddit threads show a similar mix of feedback. Users say Kikoff is a legit financial technology company and a decent option for people starting with no credit.

Several posts mention the $5 monthly fee as a fair trade-off for a beginner-friendly account with no hard credit check. Still, others raise concerns.

Some say the credit line is too restricted, while others report no real change in their credit score.

When to Use Kikoff

Kikoff can make sense for people in very specific credit situations.

You Have No Credit or Thin Credit File

If you don’t have any history with loans or credit cards, Kikoff offers a way to start reporting on-time payments.

It’s best for users who need to get something active on their credit report without going through a traditional lender or taking on real debt.

You Want a Low-Cost Credit Builder

At $5 per month, the Kikoff subscription can be a cost-effective option.

When to Avoid Kikoff

Because of the limitations, it’s best to avoid Kikoff in the following situations.

You Want a Usable Credit Card

You can’t use the credit line at other retailers or for everyday spending. If you’re looking for a flexible product, a traditional secured card may be a better option.

You Need Strong Customer Support

Many reviews mention delays in customer service, especially with account cancellations or refunds. If fast support is important, this could be frustrating.

You Already Have Established Credit

If you already have open accounts and a decent credit score, Kikoff may not provide much benefit.

Is Kikoff Legit?

Yes. Kikoff is a licensed financial technology company that reports to Experian, Equifax, and TransUnion.

How Kikoff Compares to Other Credit Builders

| App | Key Details |

|---|---|

| Kikoff | • $750 revolving credit line • $5/month, no interest for basic plan • Reports to all three bureaus • No hard pull; builds history and mix |

| Self | • Deposit-backed loan (~$25/month) • Option to upgrade to Self Visa® card • Builds credit in 12–24 months • Cancel anytime and reclaim savings |

| CreditStrong | • Loans from $1,000–$10,000 (up to 5 years) • APRs 6.99%–15.61% • No early cancellation penalty • Ideal for long-term builders |

| Experian Boost | • Free service updates Experian score fast • Adds utility and streaming payments • Reports only to Experian |